|

Taxation of Companies: Exercises |

| << Taxation of Resident Company |

| Computation of Capital Gain >> |

Taxation

Management FIN 623

VU

MODULE

8

LESSON

8.37

INCOME

FROM BUSINESS & ITS

COMPUTATION

Taxation

of Companies

Exercise-5

M/S XYZ is a

limited company, running a

chain of hospitals. The

company filed tax return along

with

relevant accounts/

documents for tax year 2006.

This return has been

selected for total audit. As a

taxation

officer,

work out taxable income

and tax liability of the said

company for tax year

2006.

Medicines

purchased Rs.

1,000,000

Ambulances-

running expenses.

Rs.

300,000

Depreciation on

ambulances

Rs.

40,000

Depreciation on

other assets

Rs.

60,000

Salaries

paid through bank accounts of

employees

Rs.

300,000

Unsupported

payment for purchase of

stationery

Rs.

12,000

Depreciation on

account of car owned by director

and in his personal use

Rs. 40,000

Payment

of legal fee by cash

Rs.

60,000

Received

payments from corporations on the panel

of the hospitals

Rs.

6,000,000

Other

receipts

Rs.

2,000,000

Gain

on sale of a vehicle

Rs.

200,000

Purchase

of X-Ray machine for shown

as expense in revenue

account

Rs.

1,000,000

Withholding

tax deductions

Rs.

525,000

Loss

carried forward from tax

year 2005

Rs.

1,200,000

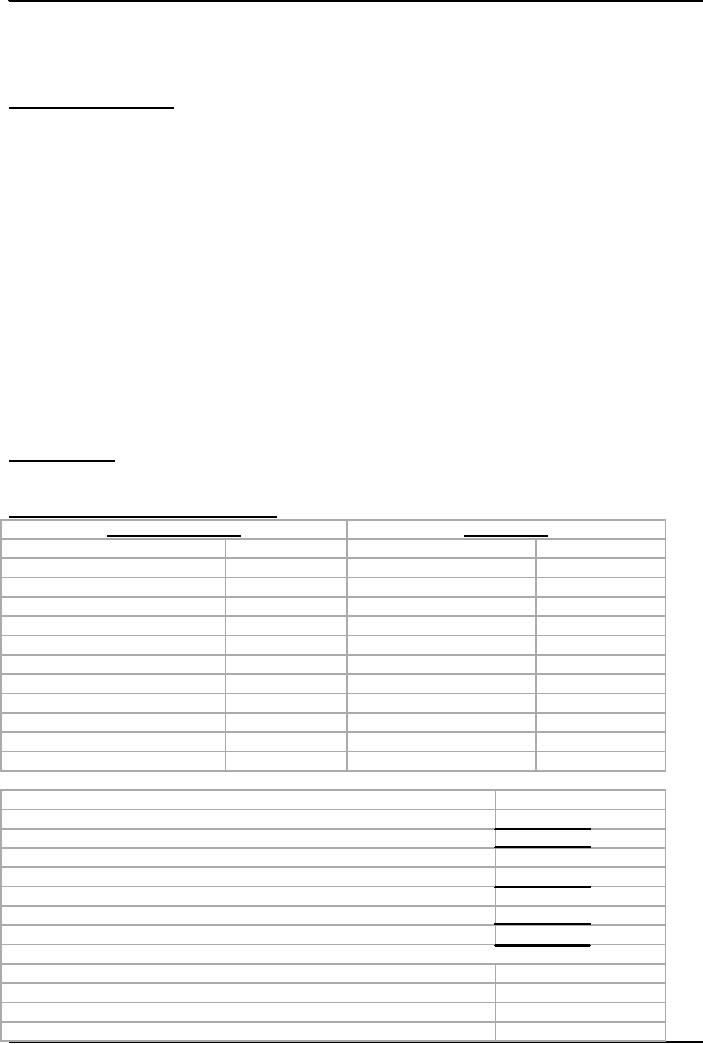

Solution

of E-5

Tax

Payer: M/S XYZ Ltd.

Tax

Year: 2006

Resident

Company

NTN:

000111

Revenue

Account as Submitted by Co.

RECEIPTS

EXPENDITURES

Particulars

Amount

in Rs. Particulars

Amount

in Rs.

Medicines

1,000,000

From

Corporations

6,000,000

Ambulances

300,000

Other

Receipts

2,000,000

Depreciation

(Ambulances)

40,000

Gain

on Sale of Vehicles

200,000

Depreciation

Others

60,000

Salaries

thru bank

300,000

Unsupported

PAMT

12,000

Depreciation on

personal car

40,000

Legal

Fee by cash

60,000

X-Ray

machine

1,000,000

Net

Profit

5,388,000

8,200,000

8,200,000

Computation

of Tax Payable:

Net

Profit as computed by Co.

5,388,000

Less

set off of c/f losses

(1,200,000)

Taxable

Income

4,188,000

Tax

Payable 4,188,000x35%

1,465,800

Less

withholding Tax

deductions

525,000

Balance

Tax Payable

940,800

Tax

Paid with Return

940,800

Tax

Payable/Refundable

NIL

Additions

by Taxation Officer on account of inadmissible

expenses:

Unsupported

payments

12,000

Depreciation

claimed on personal car of

Director

40,000

Payment

of legal fee by cash

60,000

Purchase

of X-Ray machine ( to be capitalized,

balance sheet item as such

1,000,000

69

Taxation

Management FIN 623

VU

not to

be shown in Revenue

a/c)

Total

additions

1,112,000

Tax

payable on account of add

backs (1,112,000 x 35%=

389,200)

389,200

The

company shall have to pay

tax amounting Rs 389,200.

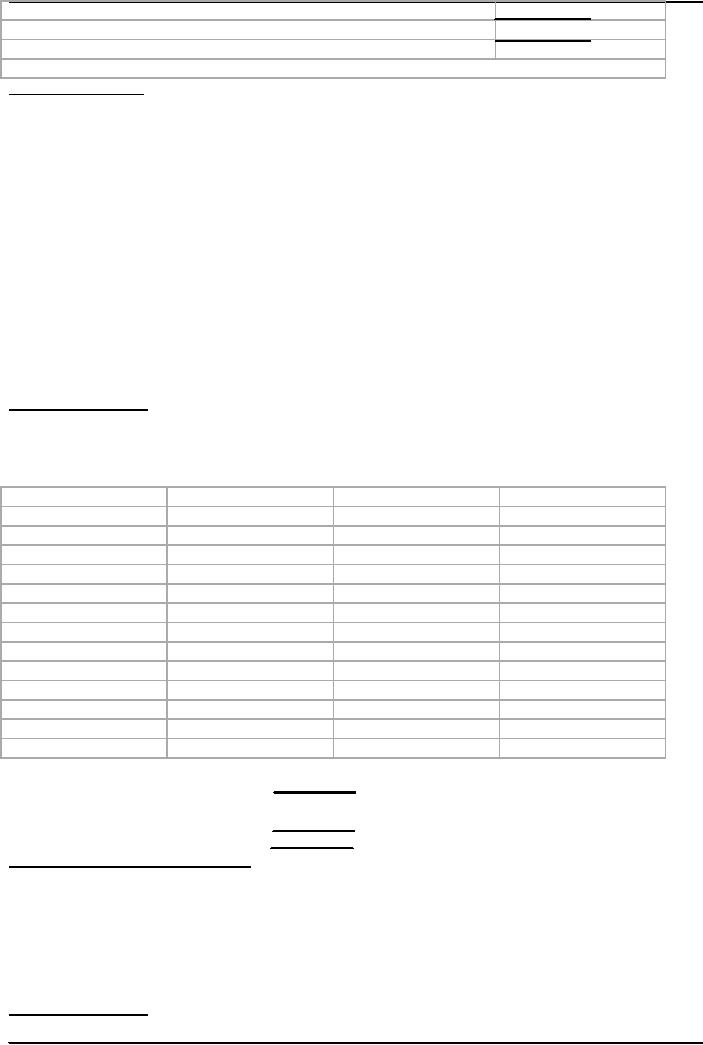

Sole

Proprietorship

Exercise-6

Mr. A

is running business as sole

proprietor. From the following

information/data relevant to tax

year

2007,

compute taxable income and

tax thereon.

Opening

Stock

Rs.800,000

Purchases

Rs.1,000,000

Sales

Rs.2,000,000

Carriage

inwards

Rs.30,000

Closing

stock

Rs.800,000

Electric

bill of office paid

Rs

18,000

Telephone

bill paid

Rs

20,000

Rent

of office

Rs

120,000

Stationary

for office

Rs

4000

Postages

Rs

3000

Salaries

to staff

Rs

200,000

Advertisement

expenses

Rs

10,000

Advance tax

paid

Rs

60,000

Solution

Exercise 6:

Tax

Payer: Mr. A

.

Tax

Year: 2007

Sole

proprietorship

NTN:

000111

Trading

and Profit & Loss Account

In

Rs

Opening

balance

800,000

Sale

2,000,000

Purchases

1,000,000

Closing Stock

800,000

Carriage

inward

30,000

Gross

profit

970,000

Total

2,800,000

2,800,000

Electricity

18,000

Telephone

20,000

Office

rent

120,000

Stationary

4,000

Postages

3,000

Salaries

200,000

Advertising

10,000

Net

profit

595,000

Total

970,000

970,000

Tax

payable 595,000 x

12.50%=

Rs.

74,375

Advance tax

paid

Rs

60,000

Tax

payable

Rs

14,375

Tax

paid with return

Rs

14,375

Tax

payable / refundable

Nil

Taxation

of Association of persons

Exercise

7:

From

the following information/ data

for tax year 2007 regarding

M/S XYZ brothers, a partnership firm,

compute

taxable income and tax

liability of the firm as well as

individual members.

This

firm comprises of three

partners Mr. X, Mr. Y and

Mr. Z, each partner has

equal share in

profits.

Net

profit of M/S XYZ brothers for tax year

2007 is worked out as Rs

900,000.

Mr. Z

has also earned income

amounting Rs 200,000 from other

sources.

Solution

Exercise 7:

Tax

Payer: M/S. XYZ

Tax

Year: 2007

70

Taxation

Management FIN 623

VU

Partnership

Firm

NTN:

000111

Net

profit (Taxable Income)

=

Rs

900,000

Tax

liability of firm

(900,000

x 17.50 %*) =

Rs

157,500

*Tax

rate at serial # 12 for

income range Rs 800,000 to

1,000,000 is applied.

Note: Tax

liability is the obligation of firm

and not of the partners.

However, if partner has income

from

any

other source, his share of

income from partnership is added to

taxable income only for

rate purposes.

Share

of profit of each member Mr. X,

Mr. Y, Mr. Z

Rs

300,000 each

Computation

of tax liability of Mr.

Z:

o Income

from other sources

Rs200,000

o Share

of profit of Mr. Z from firm

M/S XYZ brothers

(Add

for rate purposes

only)

Rs

300,000

o Taxable

income

Rs

500,000

o Tax

payable (500,000 x 10%)

Rs

50,000

o Subtract

tax liability due to addition of Rs

300,000 for rate

purposes

(50,000/

500,000 x 300,000=30,000)

Rs

30,000

Tax

payable by Mr. Z

Rs

20,000

If Rs

300,000 would have not

been added for rate

purposes, Mr. Z would have

paid tax at the rate of 4 %

that

is 200,000 x 4% = 8,000 instead of Rs

20,000.

71

Table of Contents:

- AN OVERVIEW OF TAXATION

- What is Fiscal Policy, Canons of Taxation

- Type of Taxes, Taxation Management

- BASIC FEATURES OF INCOME TAX

- STATUTORY DEFINITIONS

- IMPORTANT DEFINITIONS

- DETERMINATION OF LEGAL STATUS OF A PERSON

- HEADS OF INCOME

- Rules to Prevent Double Derivation of Income and Double Deductions

- Agricultural Income

- Computation of Income, partly Agricultural,

- Foreign Government Officials

- Exemptions and Tax Concessions

- RESIDENTIAL STATUS & TAXATION 1

- RESIDENTIAL STATUS & TAXATION 2

- Important Points Regarding Income

- Geographical Source of Income

- Taxation of Foreign-Source Income of Residents

- Exercises on Determination of Income 1

- Exercises on Determination of Income 2

- SALARY AND ITS COMPUTATION

- Definition of Salary

- Significant points regarding Salary

- Tax credits on Charitable Donations

- Investment in Shares

- SALARY AND ITS COMPUTATION EXERCISES 1

- SALARY AND ITS COMPUTATION EXERCISES 2

- SALARY AND ITS COMPUTATION EXERCISES 3

- Tax treatment of Gratuity

- Gratuity Exercise

- PROVIDENT FUND

- Exemptions on Business income, Treatment of Speculation Business

- Deductions Allowed & Not Allowed

- Deductions: Special Provisions, Depreciation

- Methods of Accounting

- Taxation of Resident Company

- Taxation of Companies: Exercises

- Computation of Capital Gain

- Disposals Not Chargeable To Tax

- TAX RETURNS & ASSESSMENT OF INCOME UNIVERSAL SELF ASSESSMENT SCHEME

- Normal Assessment, USAS, Provisional Assessment, Best Judgment Assessment

- ADVANCE TAX COLLECTION & RECOVERY OF TAX PENALTIES & PROSECUTION

- What is Value Added Tax (VAT)?

- SALES TAX

- SALES TAX RETURNS