|

REAL VERSUS NOMINAL PRICES:SUPPLY AND DEMAND, The Demand Curve |

| << Economics: Another Perspective, Factors of Production |

| Changes in Market Equilibrium:Market for College Education >> |

Microeconomics

ECO402

VU

Lesson

3

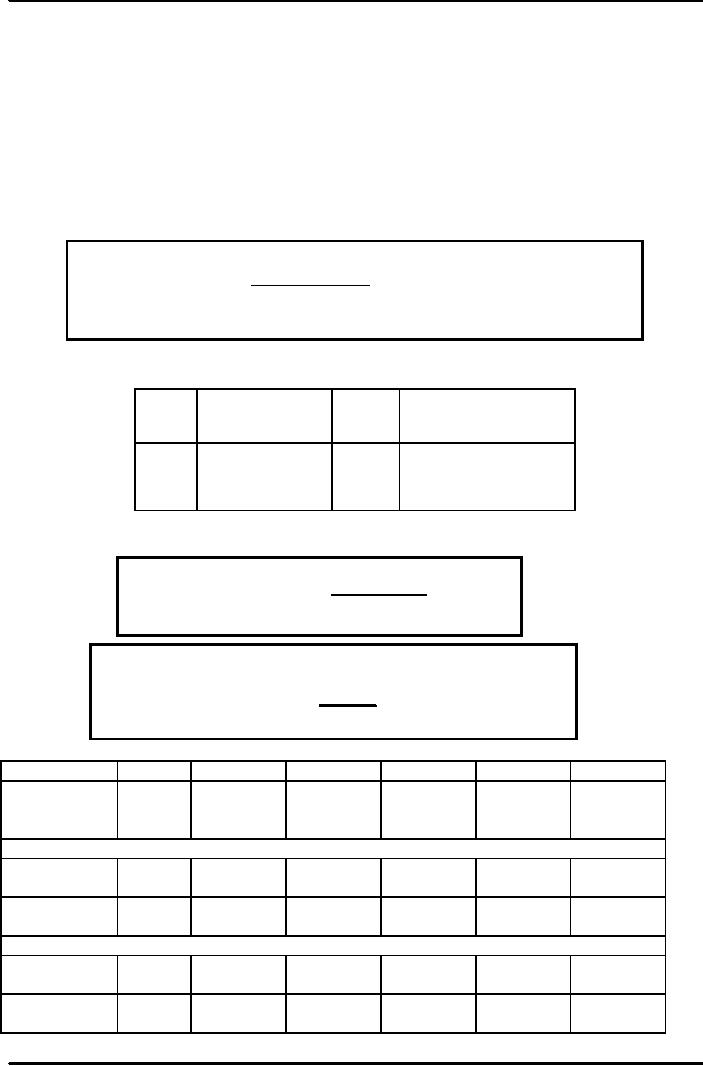

REAL

VERSUS NOMINAL

PRICES

Nominal

price is the absolute or

current dollar price of a

good or service when it is

sold.

Real

price is the price relative

to an aggregate measure of prices or

constant dollar

price.

The

Consumer Price Index (CPI)

is an aggregate measure. Real

prices are

emphasized

to permit the analysis of

relative prices.

Calculating

Real Prices

CPI

base

year

Real

Price =

x

Nominal Price current

year

CPI

current

year

Calculating

the Real Price of

Milk

Nominal

Price

Real

Price of Milk

Year

of

Milk

CPI

in

1970 dollars

1970

.40

38.8

.40=38.8/38.8x

.40

1980

.65

82.4

.31=38.8/82.4x

.65

1999

1.05

167.0

.24=38.8/167.0x

1.05

Calculating

Real Prices: An Example -

Eggs & College

38.8

1970

=

Real

Price of Eggs

x

1.04

163

1998

(1970 = 100)

Real

Price of

38.8

College

Education =

x

$19,213 =

$4,573

163.0

1998

(1970 = 100)

1970

1975

1980

1985

1990

1998

Consumer

Price

Index

38.3

53.8

82.4

107.6

130.7

163.0

(1983

= 100)

Nominal

Prices ($)

Grade

A

0.61

0.77

0.84

0.80

0.98

1.04

Large

Eggs

College

2530

3403

4912

8156

12800

19213

Education

Real

Prices ($1970)

Grade

A

0.61

0.56

0.40

0.29

0.30

0.25

Large

Eggs

College

2530

2454

2313

2941

3800

4573

Education

5

Microeconomics

ECO402

VU

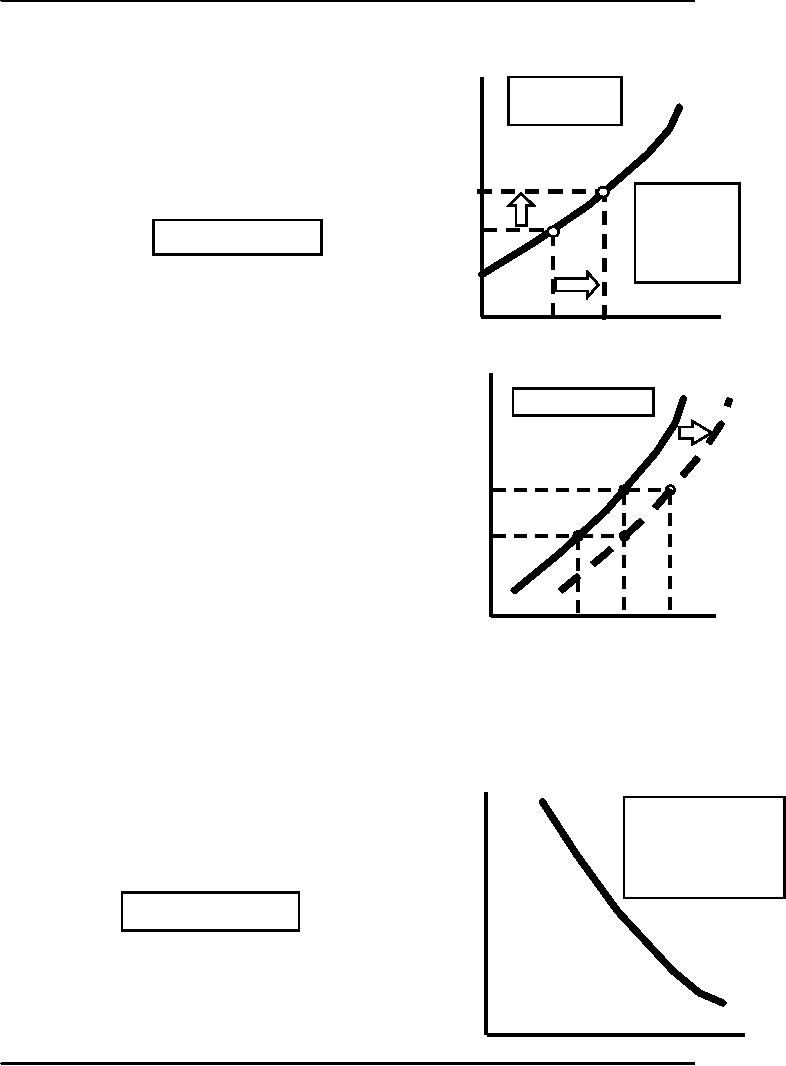

SUPPLY

AND DEMAND

The

Supply Curve

Price

($

The

Supply

S

per

unit)

The

supply curve shows how

much of a

Curve

Graphically

good

producers are willing to

sell at a

given

price, holding constant

other

factors

that might affect quantity

supplied

This

price-quantity relationship can

be

P2

shown

by the equation:

The

supply curve

slopes

upward

demonstrating

P1

=

Q

S(P

)

Q

that

at higher

s

irms

will increase

output.

Q2

Quantit

Q1

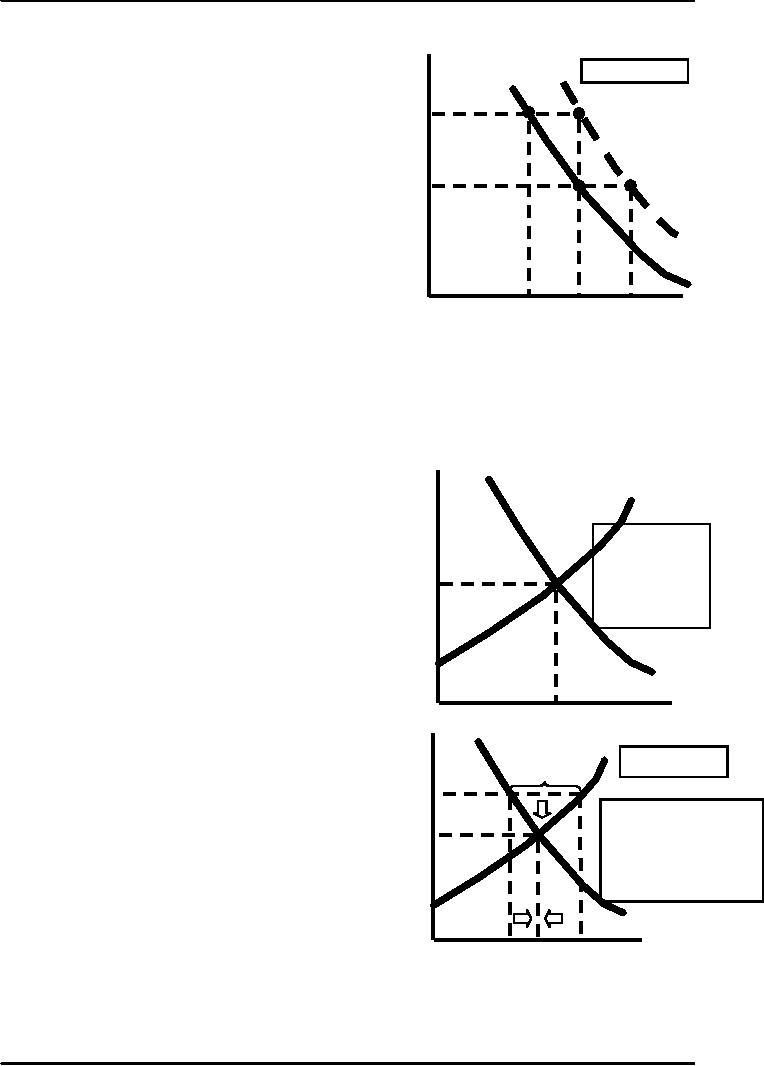

P

S'

S

Change

in Supply

Non-price

Determining Variables of

Supply

Costs of

Production

·

Labor

·

Capital

·

Raw

Materials

P1

The

cost of raw materials

falls

P2

At

P1, produce Q2

At

P2, produce Q1

Supply

curve shifts right to

S'

More

produced at any price on S'

than on S

Q0

Q1

Q

Supply

- A Review

Q2

Supply is

determined by non-price

supply-determining variables as such as

the cost of

labor,

capital, and raw

materials.

Changes in

supply are shown by shifting

the entire supply

curve.

Changes in

quantity supplied are shown

by movements along the

supply curve and

are

caused

by a change in the price of

the product.

The

Demand Curve

Price

($

The

demand curve shows how

much of a good

The

demand curve slopes

per

consumers

are willing to buy as the

price per unit

downward

demonstrating that

unit)

consumers

are willing to buy

changes

holding non-price factors

constant.

more

at a lower price as

product

becomes relatively

This

price-quantity relationship can be

shown by the

cheaper

and the consumer's

equation:

real

income increases

Q

D =

Q

D (P)

D

Quantity

6

Microeconomics

ECO402

VU

P

Non-price

Determining Variables of

Change

in Demand

D'

Demand

D

Income

P2

Consumer

Tastes

Price of

Related Goods

·

Substitutes

·

Complements

P1

Income

Increases

At

P1,

produce Q2

At

P2,

produce Q1

Demand

Curve shifts right

More

purchased at any price on

D'

than

on D

Q0

Q1

Q2

Q

Demand

- A Review

Demand is

determined by non-price

demand-determining variables, such

as,

income,

price of related goods, and

tastes.

Changes in

demand are shown by shifting

the entire demand

curve.

Changes in

quantity demanded are shown

by movements along the

demand

curve.

Price

The

Market Mechanism

($

per

S

Characteristics

of the equilibrium or

market

unit)

clearing

price:

QD =

QS

The

curves intersect

at

equilibrium, or

No

shortage

market

clearing,

No

excess supply

price.

At P0 the

P0

quantity

supplied is

No

pressure on the price to

change

equal

to the quantity

demanded

at Q0 .

D

Q0

Quantity

Price

The

market price is above

equilibrium

($

per

S

A

Surplus

There is

excess supply

unit)

Surplus

Producers

lower prices

P1

Quantity

demanded increases

and

Assume

the price is P1,then:

quantity

supplied decreases

1)

Qs : Q1 > Qd : Q2

P2

2)

Excess supply is

Q1:Q2.

The

market continues to adjust

until

3)

Producers lower

price.

the

equilibrium price is

reached.

4)

Quantity supplied

decreases

and

quantity demanded

increases.

5)

Equilibrium at P2Q3

D

Q2

Q1

Q3

Quantity

7

Microeconomics

ECO402

VU

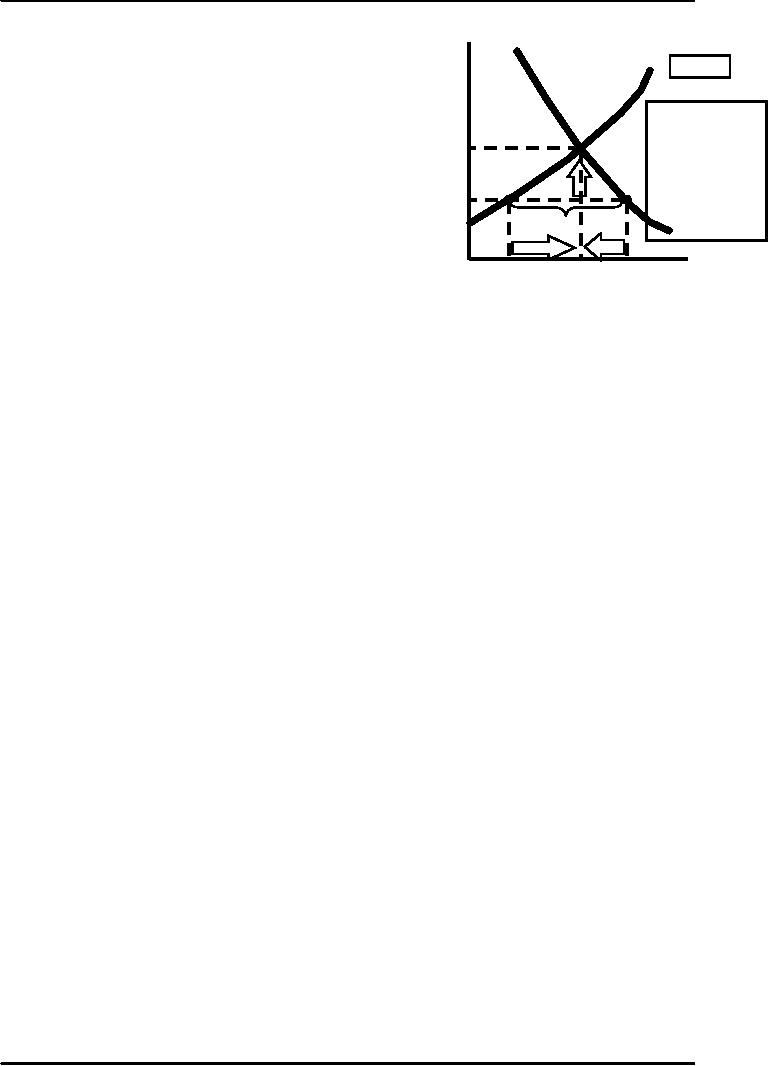

The

market price is below

equilibrium:

Price

S

There is a

shortage

($

per

Shortage

unit)

Producers

raise prices

Quantity

demanded decreases

and

Assume

the price is

quantity

supplied increases

P2,:

The

market continues to adjust

until the

1)

Qd :

Q2 > Qs

: Q1

P3

2)

Shortage is Q1:Q2.

new

equilibrium price is

reached.

3)

Producers raise

price.

4)

Quantity supplied

increases

and quantity

P2

demanded

decreases.

5)

Equilibrium at P3,

Q3

Shortage

D

Q1

Q3

Q2

Quantity

Market

Mechanism Summary

1)

Supply and demand interacts

to determine the market-clearing

price.

2)

When not in equilibrium, the

market will adjust to

alleviate a shortage or

surplus

and return the market to

equilibrium.

3)

Markets must be competitive

for the mechanism to be

efficient.

8

Table of Contents:

- ECONOMICS:Themes of Microeconomics, Theories and Models

- Economics: Another Perspective, Factors of Production

- REAL VERSUS NOMINAL PRICES:SUPPLY AND DEMAND, The Demand Curve

- Changes in Market Equilibrium:Market for College Education

- Elasticities of supply and demand:The Demand for Gasoline

- Consumer Behavior:Consumer Preferences, Indifference curves

- CONSUMER PREFERENCES:Budget Constraints, Consumer Choice

- Note it is repeated:Consumer Preferences, Revealed Preferences

- MARGINAL UTILITY AND CONSUMER CHOICE:COST-OF-LIVING INDEXES

- Review of Consumer Equilibrium:INDIVIDUAL DEMAND, An Inferior Good

- Income & Substitution Effects:Determining the Market Demand Curve

- The Aggregate Demand For Wheat:NETWORK EXTERNALITIES

- Describing Risk:Unequal Probability Outcomes

- PREFERENCES TOWARD RISK:Risk Premium, Indifference Curve

- PREFERENCES TOWARD RISK:Reducing Risk, The Demand for Risky Assets

- The Technology of Production:Production Function for Food

- Production with Two Variable Inputs:Returns to Scale

- Measuring Cost: Which Costs Matter?:Cost in the Short Run

- A Firms Short-Run Costs ($):The Effect of Effluent Fees on Firms Input Choices

- Cost in the Long Run:Long-Run Cost with Economies & Diseconomies of Scale

- Production with Two Outputs--Economies of Scope:Cubic Cost Function

- Perfectly Competitive Markets:Choosing Output in Short Run

- A Competitive Firm Incurring Losses:Industry Supply in Short Run

- Elasticity of Market Supply:Producer Surplus for a Market

- Elasticity of Market Supply:Long-Run Competitive Equilibrium

- Elasticity of Market Supply:The Industrys Long-Run Supply Curve

- Elasticity of Market Supply:Welfare loss if price is held below market-clearing level

- Price Supports:Supply Restrictions, Import Quotas and Tariffs

- The Sugar Quota:The Impact of a Tax or Subsidy, Subsidy

- Perfect Competition:Total, Marginal, and Average Revenue

- Perfect Competition:Effect of Excise Tax on Monopolist

- Monopoly:Elasticity of Demand and Price Markup, Sources of Monopoly Power

- The Social Costs of Monopoly Power:Price Regulation, Monopsony

- Monopsony Power:Pricing With Market Power, Capturing Consumer Surplus

- Monopsony Power:THE ECONOMICS OF COUPONS AND REBATES

- Airline Fares:Elasticities of Demand for Air Travel, The Two-Part Tariff

- Bundling:Consumption Decisions When Products are Bundled

- Bundling:Mixed Versus Pure Bundling, Effects of Advertising

- MONOPOLISTIC COMPETITION:Monopolistic Competition in the Market for Colas and Coffee

- OLIGOPOLY:Duopoly Example, Price Competition

- Competition Versus Collusion:The Prisoners Dilemma, Implications of the Prisoners

- COMPETITIVE FACTOR MARKETS:Marginal Revenue Product

- Competitive Factor Markets:The Demand for Jet Fuel

- Equilibrium in a Competitive Factor Market:Labor Market Equilibrium

- Factor Markets with Monopoly Power:Monopoly Power of Sellers of Labor