|

INTRODUCTION TO ECONOMICS (CONTINUED ):Opportunity Cost |

| << INTRODUCTION TO ECONOMICS:Economic Systems |

| DEMAND, SUPPLY AND EQUILIBRIUM:Goods Market and Factors Market >> |

Introduction

to Economics ECO401

VU

Lesson

1.2

INTRODUCTION

TO ECONOMICS

(CONTINUED.........)

Optimum

means

producing the best possible

results (also

optimal).

Equity

in economics means a

situation in which every

thing is treated fairly or

equally, i.e.

according

to its due share. So if the

lives of all individuals are

deemed to have equal

value,

equity

would demand that all of

them have equal financial

net worth.

Nepotism

means

doing unfair favors for

near ones when in

power.

Microeconomics

and Macroeconomics:

Microeconomics

deals with the behavior of

individual elements in the

economy.

Macroeconomics

deals with the behavior of

the economy as whole or on

aggregate level.

Rational

choice is the

choice based on pure reason

and without succumbing to

one's

emotions

or whims.

Barter

trade is a

non-monetary system of trade in

which "goods" not money is

exchanged.

This

was the system used in

the world before the

advent of coins and

currency.

Opportunity

Cost:

The

opportunity cost of a particular

choice is the satisfaction

that would have been

derived

from

the next best alternative

foregone; in other words, it is

what must be given up

or

sacrificed

in making a certain choice or

decision.

Marginal

Cost and Marginal

Benefit:

Marginal

cost is the increment to

total costs of producing an

additional unit of some good

or

service.

There are other broader

definitions as well.

Marginal

benefit is the increment to

total benefit derived from

consuming an additional unit

of

good

or service. There are other

broader definitions as

well.

Production

Possibility Frontier

(PPF):

Production

possibility frontier (PPF) is

the curve which joins

all the points showing

the

maximum

amount of goods and services

which the country can

produce in a given time

with

limited

resources, given a specific

state of technology.

Economic

growth is an increase

in the total output of a

country over time.

2

Introduction

to Economics ECO401

VU

END

OF UNIT 1 - EXERCISES

Could

production and consumption

take place without money? If

you think they

could,

give

examples.

Yes.

People could produce things

for their own consumption.

For example, people could

grow

vegetables

in their garden or allotment;

they could do their own

painting and

decorating.

Alternatively

people could engage in

barter: they could produce

things and then swap

them for

goods

that other people had

produced.

Must

goods be at least temporarily

unattainable to be scarce?

Goods

need not be unattainable to be

scarce. Because people's

incomes are limited, they

can

not

have everything they want

from shops, even though

the shops are stocked

full. If all items in

shops

were free, the shelves

would soon be

emptied!

If

we would all like more

money, why does the

government not print a lot

more? Could it

not

thereby solve the problem of

scarcity `at a

stroke'?

The

problem of scarcity is one of a

lack of production. Simply

printing more money

without

producing

more goods and services

will merely lead to

inflation. To the extent

that firms cannot

meet

the extra demand (i.e.

the extra consumer

expenditure) by extra production,

they will

respond

by putting up their prices.

Without extra production,

consumers will be unable to

buy

any

more than previously.

Which

of the following are

macroeconomic issues, which

are microeconomic ones

and

which

could be either depending on

the context?

a)

Inflation.

b)

Low wages in certain service

industries.

c)

The rate of exchange between

the dollar and the

rupee.

d)

Why the price of cabbages

fluctuates more than that of

cars.

e)

The rate of economic growth

this year compared with

last year.

f)The

decline of traditional manufacturing

industries.

a)

Macro. It refers to a general

rise in prices across the

whole economy.

b)

Micro. It refers to specific

industries

c)

Either. In a world context, it is a

micro issue, since it refers

to the price of one

currency

in terms of one other. In a

national context it is more of a

macro issue,

since

it refers to the exchange

rate at which all Pakistanis

goods are traded

internationally.

(This is certainly a less

clearcut division that in

(a) and (b)

above.)

d)

Micro. It refers to specific

products.

e)

Macro. It refers to the

general growth in output of

the economy as a

whole.

f)Micro

(macro in certain contexts). It is

micro because it refers to

specific industries. It

could,

however, also help to

explain the macroeconomic

phenomena of high

unemployment

or balance of payments

problems.

Assume

that you are looking

for a job and are

offered two. One is more

unpleasant to do,

but

pays more. How would

you make a rational choice

between the two

jobs?

You

should weigh up whether the

extra pay (benefit) from

the better paid job is

worth the extra

hardship

(cost) involved in doing

it.

How

would the principle of

weighing up marginal costs

and benefits apply to a

worker

deciding

how much overtime to work in

a given week?

The

worker would consider

whether the extra pay

(the marginal benefit) is

worth the extra

effort

and

loss of leisure (the

marginal cost).

3

Introduction

to Economics ECO401

VU

Would

it ever be desirable to have

total equality in an

economy?

The

objective of total equality

may be regarded as desirable in

itself by many people. There

are

two

problems with this

objective, however. The

first is in defining equality. If

there were total

equality

of incomes then households

with dependants would have a

lower income per head

than

households

where everyone was working.

In other words, equality of

incomes would not

mean

equality

in terms of standards of

living.

If

on the other hand, equality

were to be defined in terms of

standards of living, then

should the

different

needs of different people be

taken into account? Should

people with special health

or

other

needs have a higher income?

Also, if equality were to be

defined in terms of standards

of

living,

many people would regard it

as unfair that people should

receive different

incomes

(according

to the nature of their

household) for doing the

same amount of work.

The

second major problem

concerns incentives. If all

jobs were to be paid the

same (or people

were

to be paid according to the

composition of their household),

irrespective of people's

efforts

or

skills, then what would be

the incentive to train or to

work harder?

If

there are several other

things you could have

done, is the opportunity

cost the sum of

all

of them?

No.

It is the sacrifice involved in

the next best

alternative.

What

is the opportunity cost of

spending an evening revising

for an economics

exam?

What

would you need to know in

order to make a sensible

decision about what to do

that

evening?

The

next best alternative might

be revising for another

exam, or it might be taking

time off to

relax

or to go out. To make a sensible

decision, you need to

consider these alternatives

and

whether

they are better or worse

for you than studying

for the economics exam.

One major

problem

here is the lack of

information. You do not know

just how much the

extra study will

improve

your performance in the

exam, because you do not

know in advance just how

much you

will

learn and you do not

know what is going to be on

the exam paper. Similarly

you do not

know

this information for

studying for other

exams.

Make

a list of the benefits of

higher education.

The

benefits to the individual

include: increased future

earnings; the direct

benefits of being

more

educated; the pleasure of

the social contacts at

university or college.

Is

the opportunity cost to the

individual of attending higher

education different from

the

opportunity

costs to society as a

whole?

Yes.

The opportunity cost to

society as a whole would

include the costs of

providing tuition

(staffing

costs, materials, capital

costs, etc.), which could be

greater than any fees

the student

may

have to pay. On the other

hand, the benefits to

society would include

benefits beyond those

received

by the individual. For

example, they would include

the extra profits employers

would

make

by employing the individual

with those

qualifications.

There

is a saying in economics, `There is no

such thing as a free lunch'

(hence the sub-

title

for this box). What

does this mean?

That

there is always (or

virtually always) an opportunity

cost of anything we consume.

Even if

we

do not incur the cost

ourselves (the `lunch' is

free to us), someone will

incur the cost (e.g.

the

institution

providing the lunch).

Are

any other (desirable) goods or

services truly

abundant?

Very

few! Possibly various social

interactions between people,

but even here, the

time to enjoy

them

is not abundant.

4

Introduction

to Economics ECO401

VU

Under

what circumstances would the

production possibility curve be

(a) a straight

line;

(b)

bowed in toward the origin?

Are these circumstances ever

likely?

a)

When there are constant

opportunity costs. This will

occur when resources are

equally

suited

to producing either good.

This might possibly occur in

our highly simplified

world

of

just two goods. In the

real world it is

unlikely.

b)

When there are decreasing

opportunity costs. This

will occur when

increased

specialization

in one good allows the

country to become more

efficient in its

production.

It

gains `economies of scale'

sufficient to offset having to

use less suitable

resources.

Will

economic growth necessarily

involve a parallel outward

shift of the

production

possibility

curve?

No.

Technical progress, the

discovery of raw materials,

improved education and

training, etc.,

may

favour one good rather

than the other. In such

cases the gap between

the old and

new

curves

would be widest where they

meet the axis of the

good whose potential output

had grown

more.

Do

you agree with the

positions that the eight

countries (including Pakistan)

have been

given

in the economics systems

spectrum diagram? Explain why or why

not.

Given

that there is no clearly

defined scale by which

government intervention or

free-marketness

is

measured, the precise

position of the countries

along the spectrum is open

to question.

Can

you think of any examples

where prices and wages do

not adjust very rapidly to

a

shortage

or surplus? For what reasons

might they not do

so?

Many

prices set by companies are

adjusted relatively infrequently: it

would be

administratively

too costly to change them

every time there was a

change in demand.

For

example a mail order

company, where all the

items in its catalogue have

a printed

price,

would find it costly to

adjust prices very

frequently, since that would

involve printing

a

new catalogue, or at least a

new price list.

Many

wages are set annually by a

process of collective bargaining.

They are not

adjusted

in

the interim.

Why

do the prices of fresh

vegetables fall when they

are in season? Could an

individual

farmer

prevent the price

falling?

Because

supply is at a high level.

The increased supply creates

a surplus which pushes

down

the

price. Individual farmers

could not prevent the

price falling. If they

continued to charge

the

higher

price, consumers would

simply buy from those

farmers charging the lower

price.

If

you were the owner of a

clothes shop, how would

you set about deciding

what prices to

charge

for each garment at the

end of season

sale?

You

would try to reduce the

price of each item as little

as was necessary to get rid

of the

remaining

stock. The problem for

shop owners is that they do

not have enough

information

about

consumer demand to make

precise calculations here.

Many shops try a fairly

cautious

approach

first, and then, if that is

not enough to sell all

the stock, they make

further `end of sale'

reductions

later.

The

number of owners of CD players

has grown rapidly and

hence the demand for

CDs

has

also grown rapidly. Yet

the prices of CDs have

fallen. How could this

come about?

·

The

costs of manufacturing CDs

may have fallen with

improvements in technology

and

mass-production

economies.

·

Competition

from increased numbers of

manufacturers may have

increased supply of

CDs

and

driven prices down.

5

Introduction

to Economics ECO401

VU

·

The advent of

copying tracks from the

internet reduces the demand

for CDs. This

change

in

demand has further

compounded the fall in

price.

Which

of the following are

positive statements, which

are normative statements

and

which

could be either depending on

the context?

a)

Cutting the higher rates of

income tax will redistribute

incomes from the

poor

to the rich.

b)

It is wrong that inflation

should be reduced if this

means that there will

be

higher

unemployment.

c)

It is wrong to state that

putting up interest rates

will reduce

inflation.

d)

The government should raise

interest rates in order to

prevent the

exchange

rate falling.

e)

Current government policies

should reduce

unemployment.

a)

Positive. This is merely a

statement about what would

happen.

b)

Normative. The statement is

making the value judgment

that reducing inflation is a

less

desirable

goal than the avoidance of

higher unemployment.

c)

Positive. Here the word

`wrong' means `incorrect'

not `morally wrong'. The

statement is

making

a claim that can be tested

by looking at the facts. Do

higher interest rates

reduce

inflation,

or don't they?

d)

Both. The positive element

is the claim that higher

interest rates prevent the

exchange

rate

falling. This can be tested

by an appeal to the facts.

The normative element is

the

value

judgment that the government

ought to prevent the

exchange rate

falling.

e)

Either. It depends what is

meant. If the statement

means that current

government

policies

are likely to reduce

unemployment, the statement is

positive. If, however,

it

means

that the government ought to

direct its policies towards

reducing unemployment,

the

statement is normative.

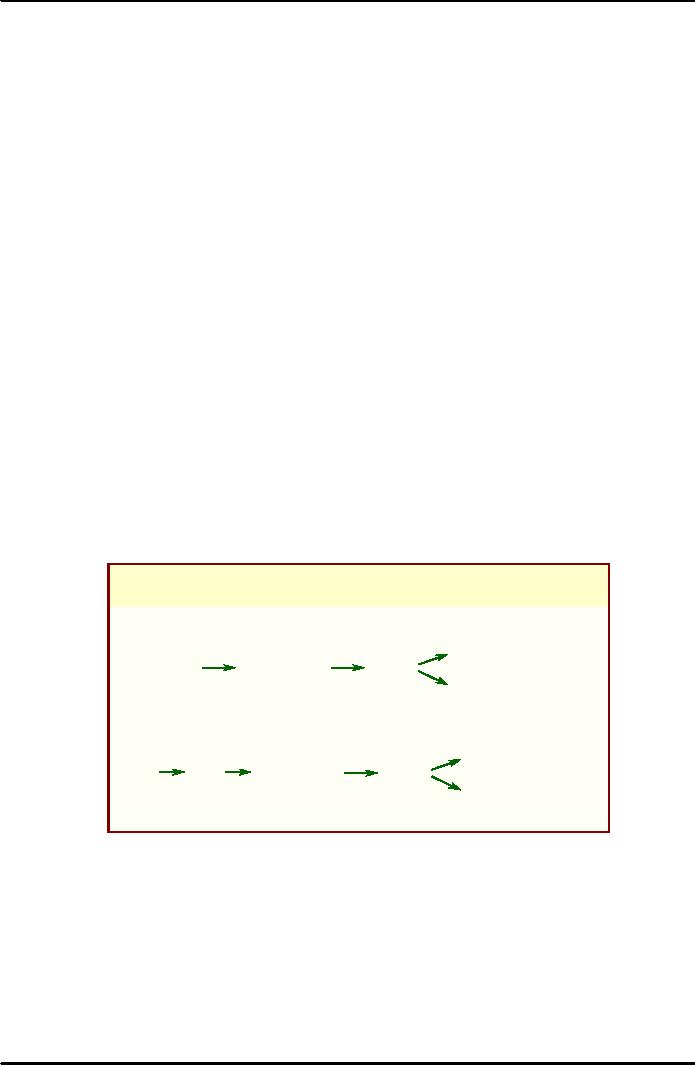

Explain

in words what is happening in

the following

diagram.

T

h e p r ic e m e c h a n is m : th e e f fe c t o f th e d is c o v e r y o f r

a w m a te r ia ls

F

a c to r M a rk e t

Si ↓

Si ↑

Pi ↓

s

u rp lu s

u

n t il D

i =

S i

(

S

i > D i)

Di ↑

G

o o d s M a rk e t

Sg ↓

Pi ↓

Sg ↑

Pg ↓

s

u rp lu s

u

n t il D

g =

S g

(S

g > D g)

Dg ↑

The

new discovery of raw

material i means an increase in

the supply i. This causes a

surplus

(excess

supply) in the market for i,

causing the price of i to

fall until the same is

removed (lower

Pi

causes demand to increase

and supply to fall). The

reduction in Pi also reduces

the cost of

producing

good g (we can assume

good g uses the factor i

intensively), causing the

supply of

good

g to increase beyond demand.

The surplus in the market

for good g drives the

price of g

down

until the excess is cleared.

The diagram illustrates

interdependence between goods

and

factor

markets.

Can

different factor markets be

interdependent also? Give

examples.

Yes.

A rise in the price of one

factor (e.g. oil) will

encourage producers to switch to

alternatives

(e.g.

coal). This will create a

shortage of coal and drive

up its price. This will

encourage

6

Introduction

to Economics ECO401

VU

increased

production of coal. Similarly an

increase in the population

(and consequently size

of

the

labour force) of a country

will depress the price of

labour (wages). This will

cause producers

to

shift to more labour

intensive production and

reduce production methods

which are capital

(or

machine)

intensive. As a result the

demand for capital will

fall reducing its rental

price.

7

Table of Contents:

- INTRODUCTION TO ECONOMICS:Economic Systems

- INTRODUCTION TO ECONOMICS (CONTINUED ):Opportunity Cost

- DEMAND, SUPPLY AND EQUILIBRIUM:Goods Market and Factors Market

- DEMAND, SUPPLY AND EQUILIBRIUM (CONTINUED ..)

- DEMAND, SUPPLY AND EQUILIBRIUM (CONTINUED ..):Equilibrium

- ELASTICITIES:Price Elasticity of Demand, Point Elasticity, Arc Elasticity

- ELASTICITIES (CONTINUED .):Total revenue and Elasticity

- ELASTICITIES (CONTINUED .):Short Run and Long Run, Incidence of Taxation

- BACKGROUND TO DEMAND/CONSUMPTION:CONSUMER BEHAVIOR

- BACKGROUND TO DEMAND/CONSUMPTION (CONTINUED .)

- BACKGROUND TO DEMAND/CONSUMPTION (CONTINUED .)The Indifference Curve Approach

- BACKGROUND TO DEMAND/CONSUMPTION (CONTINUED .):Normal Goods and Giffen Good

- BACKGROUND TO SUPPLY/COSTS:PRODUCTIVE THEORY

- BACKGROUND TO SUPPLY/COSTS (CONTINUED ..):The Scale of Production

- BACKGROUND TO SUPPLY/COSTS (CONTINUED ..):Isoquant

- BACKGROUND TO SUPPLY/COSTS (CONTINUED ..):COSTS

- BACKGROUND TO SUPPLY/COSTS (CONTINUED ..):REVENUES

- BACKGROUND TO SUPPLY/COSTS (CONTINUED ..):PROFIT MAXIMISATION

- MARKET STRUCTURES:PERFECT COMPETITION, Allocative efficiency

- MARKET STRUCTURES (CONTINUED ..):MONOPOLY

- MARKET STRUCTURES (CONTINUED ..):PRICE DISCRIMINATION

- MARKET STRUCTURES (CONTINUED ..):OLIGOPOLY

- SELECTED ISSUES IN MICROECONOMICS:WELFARE ECONOMICS

- SELECTED ISSUES IN MICROECONOMICS (CONTINUED )

- INTRODUCTION TO MACROECONOMICS:Price Level and its Effects:

- INTRODUCTION TO MACROECONOMICS (CONTINUED ..)

- INTRODUCTION TO MACROECONOMICS (CONTINUED ..):The Monetarist School

- THE USE OF MACROECONOMIC DATA, AND THE DEFINITION AND ACCOUNTING OF NATIONAL INCOME

- THE USE OF MACROECONOMIC DATA, AND THE DEFINITION AND ACCOUNTING OF NATIONAL INCOME (CONTINUED ..)

- MACROECONOMIC EQUILIBRIUM & VARIABLES; THE DETERMINATION OF EQUILIBRIUM INCOME

- MACROECONOMIC EQUILIBRIUM & VARIABLES; THE DETERMINATION OF EQUILIBRIUM INCOME (CONTINUED ..)

- MACROECONOMIC EQUILIBRIUM & VARIABLES; THE DETERMINATION OF EQUILIBRIUM INCOME (CONTINUED ..):The Accelerator

- THE FOUR BIG MACROECONOMIC ISSUES AND THEIR INTER-RELATIONSHIPS

- THE FOUR BIG MACROECONOMIC ISSUES AND THEIR INTER-RELATIONSHIPS (CONTINUED .)

- THE FOUR BIG MACROECONOMIC ISSUES AND THEIR INTER-RELATIONSHIPS (CONTINUED .):Causes of Inflation

- THE FOUR BIG MACROECONOMIC ISSUES AND THEIR INTER-RELATIONSHIPS (CONTINUED .):BALANCE OF PAYMENTS

- THE FOUR BIG MACROECONOMIC ISSUES AND THEIR INTER-RELATIONSHIPS (CONTINUED .):GROWTH

- THE FOUR BIG MACROECONOMIC ISSUES AND THEIR INTER-RELATIONSHIPS (CONTINUED .):Land

- THE FOUR BIG MACROECONOMIC ISSUES AND THEIR INTER-RELATIONSHIPS (CONTINUED .):Growth-inflation

- FISCAL POLICY AND TAXATION:Budget Deficit, Budget Surplus and Balanced Budget

- MONEY, CENTRAL BANKING AND MONETARY POLICY

- MONEY, CENTRAL BANKING AND MONETARY POLICY (CONTINUED .)

- JOINT EQUILIBRIUM IN THE MONEY AND GOODS MARKETS: THE IS-LM FRAMEWORK

- AN INTRODUCTION TO INTERNATIONAL TRADE AND FINANCE

- PROBLEMS OF LOWER INCOME COUNTRIES:Poverty trap theories: