|

Elasticity of Market Supply:Long-Run Competitive Equilibrium |

| << Elasticity of Market Supply:Producer Surplus for a Market |

| Elasticity of Market Supply:The Industrys Long-Run Supply Curve >> |

Microeconomics

ECO402

VU

·

The

long-run response to short-run

profits is to increase output

and profits.

·

Profits

will attract other

producers.

·

More

producers increase industry

supply which lowers the

market price.

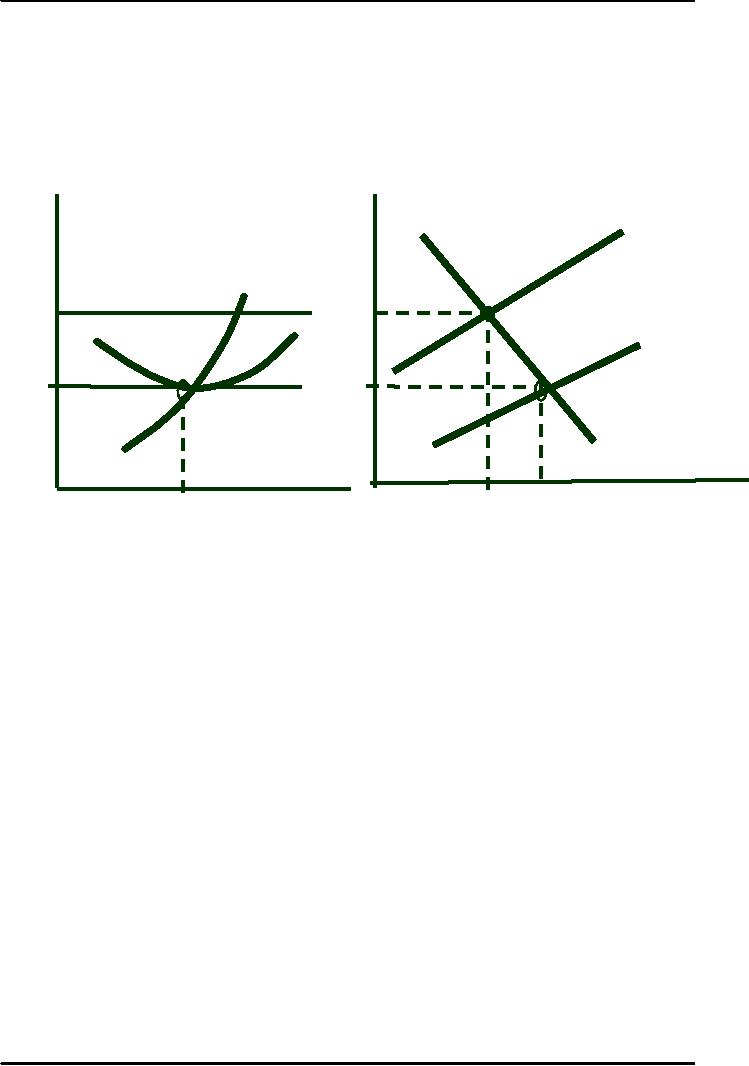

Long-Run

Competitive Equilibrium

·Profit

attracts firms

·Supply

increases until profit =

0

$

per

Firm

Industry

$

per

unit

of

S

unit

of

output

output

LMC

P

$40

S

LAC

$3

P

0

2

D

Q2

Q

Output

q2

Output

Long-Run

Competitive Equilibrium

1)

MC

= MR

2)

P

= LAC

·

No incentive to

leave or enter

·

Profit =

0

3)

Equilibrium

Market Price

Questions

1)

Explain the market

adjustment when P < LAC

and firms have identical

costs.

2)

Explain the market

adjustment when firms have

different costs.

3)

What is the opportunity cost

of land?

Economic

Rent

Economic rent

is the difference between

what firms are willing to

pay for an input

less

the

minimum amount necessary to

obtain it.

An

Example

Two firms

A

&

B

Both own

their land

A

is

located on a river which

lowers A's

shipping

cost by $10,000 compared to

B

124

Microeconomics

ECO402

VU

The demand

for A's

river

location will increase the

price of A's

land

to $10,000

Economic rent =

$10,000

·

$10,000 -

zero cost for the

land

Economic rent

increases

Economic profit

of A

=

0

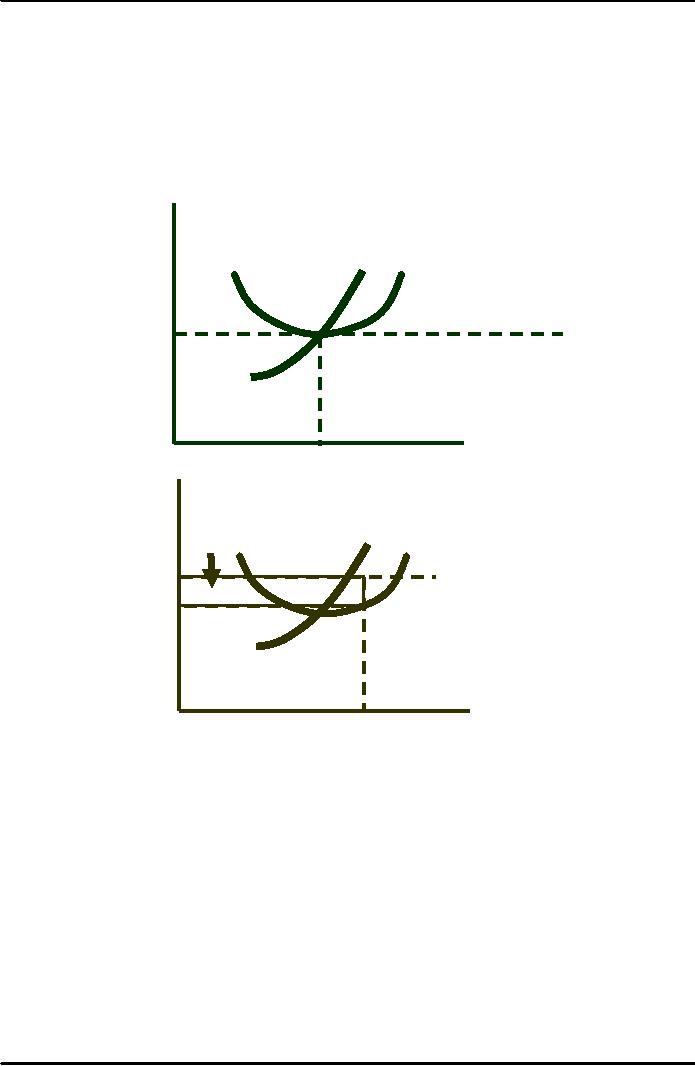

Firms

Earn Zero Profit in Long-Run

Equilibrium

A

baseball team

Ticket

in

a moderate-sized

Price

city

sells enough

tickets

so that price

is

equal to marginal

LMC

LAC

and

average cost

(profit

= 0).

$7

Season

Tickets

Sales

(millions)

1.0

Ticket

Price

LMC

LAC

Economic

Rent

$10

A

team with the

same

$7

cost

in a larger city

sells

tickets for $10.

Season

Tickets

Sales

1.3

(millions)

With

a fixed input such as a

unique location, the

difference between the cost

of production

(LAC

= 7) and price ($10) is the

value or opportunity cost of

the input (location)

and

represents

the economic rent from

the input.

If

the opportunity cost of the

input (rent) is not taken

into consideration it may

appear that

economic

profits exist in the

long-run.

125

Table of Contents:

- ECONOMICS:Themes of Microeconomics, Theories and Models

- Economics: Another Perspective, Factors of Production

- REAL VERSUS NOMINAL PRICES:SUPPLY AND DEMAND, The Demand Curve

- Changes in Market Equilibrium:Market for College Education

- Elasticities of supply and demand:The Demand for Gasoline

- Consumer Behavior:Consumer Preferences, Indifference curves

- CONSUMER PREFERENCES:Budget Constraints, Consumer Choice

- Note it is repeated:Consumer Preferences, Revealed Preferences

- MARGINAL UTILITY AND CONSUMER CHOICE:COST-OF-LIVING INDEXES

- Review of Consumer Equilibrium:INDIVIDUAL DEMAND, An Inferior Good

- Income & Substitution Effects:Determining the Market Demand Curve

- The Aggregate Demand For Wheat:NETWORK EXTERNALITIES

- Describing Risk:Unequal Probability Outcomes

- PREFERENCES TOWARD RISK:Risk Premium, Indifference Curve

- PREFERENCES TOWARD RISK:Reducing Risk, The Demand for Risky Assets

- The Technology of Production:Production Function for Food

- Production with Two Variable Inputs:Returns to Scale

- Measuring Cost: Which Costs Matter?:Cost in the Short Run

- A Firms Short-Run Costs ($):The Effect of Effluent Fees on Firms Input Choices

- Cost in the Long Run:Long-Run Cost with Economies & Diseconomies of Scale

- Production with Two Outputs--Economies of Scope:Cubic Cost Function

- Perfectly Competitive Markets:Choosing Output in Short Run

- A Competitive Firm Incurring Losses:Industry Supply in Short Run

- Elasticity of Market Supply:Producer Surplus for a Market

- Elasticity of Market Supply:Long-Run Competitive Equilibrium

- Elasticity of Market Supply:The Industrys Long-Run Supply Curve

- Elasticity of Market Supply:Welfare loss if price is held below market-clearing level

- Price Supports:Supply Restrictions, Import Quotas and Tariffs

- The Sugar Quota:The Impact of a Tax or Subsidy, Subsidy

- Perfect Competition:Total, Marginal, and Average Revenue

- Perfect Competition:Effect of Excise Tax on Monopolist

- Monopoly:Elasticity of Demand and Price Markup, Sources of Monopoly Power

- The Social Costs of Monopoly Power:Price Regulation, Monopsony

- Monopsony Power:Pricing With Market Power, Capturing Consumer Surplus

- Monopsony Power:THE ECONOMICS OF COUPONS AND REBATES

- Airline Fares:Elasticities of Demand for Air Travel, The Two-Part Tariff

- Bundling:Consumption Decisions When Products are Bundled

- Bundling:Mixed Versus Pure Bundling, Effects of Advertising

- MONOPOLISTIC COMPETITION:Monopolistic Competition in the Market for Colas and Coffee

- OLIGOPOLY:Duopoly Example, Price Competition

- Competition Versus Collusion:The Prisoners Dilemma, Implications of the Prisoners

- COMPETITIVE FACTOR MARKETS:Marginal Revenue Product

- Competitive Factor Markets:The Demand for Jet Fuel

- Equilibrium in a Competitive Factor Market:Labor Market Equilibrium

- Factor Markets with Monopoly Power:Monopoly Power of Sellers of Labor