|

COMPANY ACCOUNTS 2 |

| << COMPANY ACCOUNTS 1 |

| Problems Solving >> |

Advance

Financial Accounting

(FIN-611)

VU

LESSON

# 21

COMPANY

ACCOUNTS

Components

of financial statements

As

per International Accounting

Standards there are five

components of financial

statements:

1.

Balance

Sheet

2.

Income

Statement

3.

Statement

of Changes in Equity

4.

Cash

Flow Statement

5.

Notes

Here

we will discuss all but cash flow

statement in detail as the

cash flow statement

will be

discussed in separate

chapter.

1)

Balance Sheet

It

has already been discussed

in the preceding section

that balance sheet of an

entity

shows

financial position, which comprises of

resources and source. A very

simple

equation

of balance sheet is:

Assets

= Owners' Equity +

Liabilities.

Where

Assets are the resources and

Owners' Equity and Liabilities

are the sources.

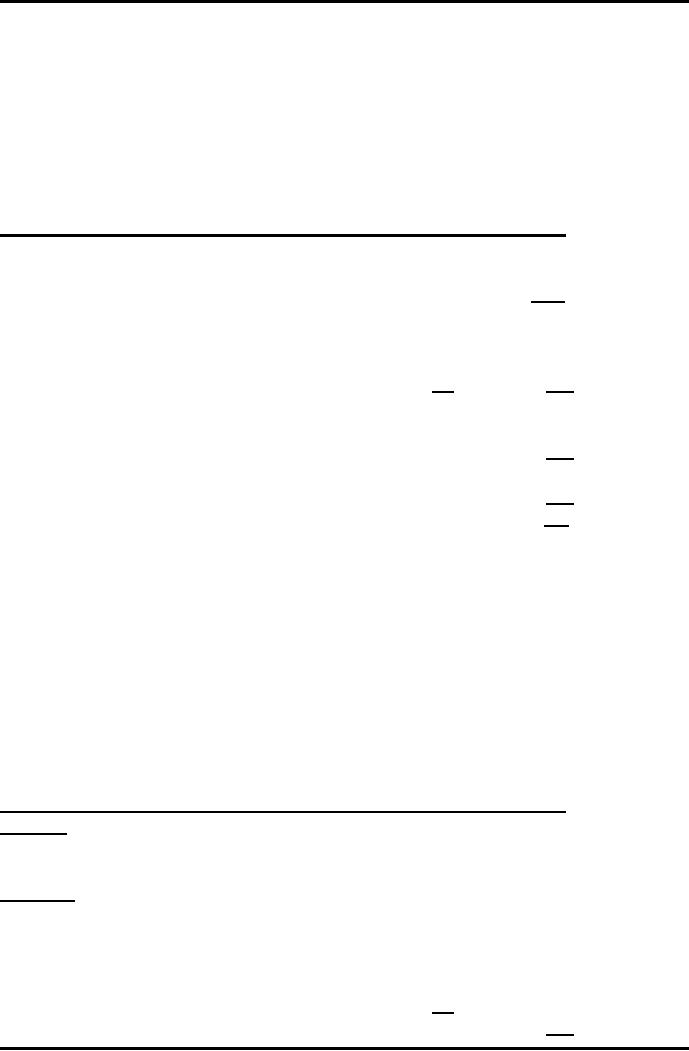

Limited

Liability Company

Balance

Sheet

As on

December 31, 2009

Rs.

Rs.

Assets

(Resources)

Non

Current Assets

Fixed

Assets

Tangible

Assets

***

***

Intangible

Assets

***

Long Term

Investments

***

Long Term

Loans

***

Long Term

Advances, Deposits &

Prepayments

***

***

Current

Assets

***

Current

Liabilities

(***)

***

Capital

Employed

***

97

Advance

Financial Accounting

(FIN-611)

VU

Financed

By (Sources)

Owners'

Equity

Ordinary

Share Capital

***

Reserves

Capital

Reserves

***

Revenue

Reserves

***

***

***

Non

Current Liabilities

Loan

Stocks/Term Finance

Certificates

***

Loan

from financial institutions

***

Finance

lease liability

***

***

Capital

Employed

***

Approved

by Chief Executive and a

Director

Classification

of assets in the balance sheet is on

the base of permanency

order. This is

known as

marshaling. In a company balance

sheet grouping and marshaling is

strictly

followed.

It is clearly presented in the

balances sheet that assets

are broadly

classified

into

Non-Current Assets and Current

Assets. Non-Current Assets

are then grouped

into

fixed and other non-current

assets. Fixed assets are further

classified into fixed

tangible

and fixed intangible

assets.

a)

Fixed Tangible

Assets

These

are the property, plant and

equipment that are held by

the entity a) for

production

or selling of goods or services, b) for

administrative purposes, or c) for

rental

to others. These are

expected to be useful for the

entity for more than

one

accounting

year.

Examples

include:

land & Building, Plant &

Machinery, Furniture & fixtures,

Motor

Vehicles,

Office equipments

etc.

b)

Fixed Intangible

Assets

These

are the identifiable, non

monetary asset in control of

the entity that have

no

physical

existence and are expected to be

useful for the entity for

more than one

accounting

year.

Examples

include:

Trademark, Copy right, Patents,

Designs etc.

c)

Long term

Investment

These

are the investments made by

the company in other

entities for more than

one

accounting

year.

98

Advance

Financial Accounting

(FIN-611)

VU

Examples

include:

Investments in equity instruments or

debt instruments of

other

entities.

d)

Long term

loans

These

are the loans given to

the third parties on long term basis,

receivable after the

expiry

of more than one accounting

year.

e)

Long term advances,

deposits, and

prepayments

These

are the security deposits,

fixed deposits, advances

given to the suppliers

of

assets,

and prepayments on long term

basis.

f)

Current Assets

These

are the assets recoverable and

tradable within the normal operating

cycle of an

entity

that is 12 months after the

balance sheet date in normal

circumstances. Cash and

cash

equivalents are also current

assets.

g)

Current Liabilities

These

are the obligations that

are payable within the normal

operating cycle of an

entity

that is 12 months after the

balance sheet date in normal

circumstances. This

also

include

bank overdraft.

2)

Income Statement

Income

Statement is prepared to know the

financial performance of an entity. In

an

Income

Statement; expenses for the

year are subtracted from the

incomes earned

during

the year. Both incomes and

expenses are measured

according to the

accrual

concept,

whereas, profit are measured

according to the matching

concept.

According

to the IAS 1 Income Statement

can be prepared using

ether:

1.

Function of expenses method,

or

2.

Nature of expenses

method

a)

Function of expenses

method

According

to the functions of expenses

method the expenses are

divided into five

groups

according to their

functions:

· Cost

of sales

· Administrative

· Selling

and marketing

· Financial

· Income

Tax

99

Advance

Financial Accounting

(FIN-611)

VU

Incomes

are also divided into two

groups:

·

Sales

revenue (operating

income)

·

Other

incomes (non-operating

incomes)

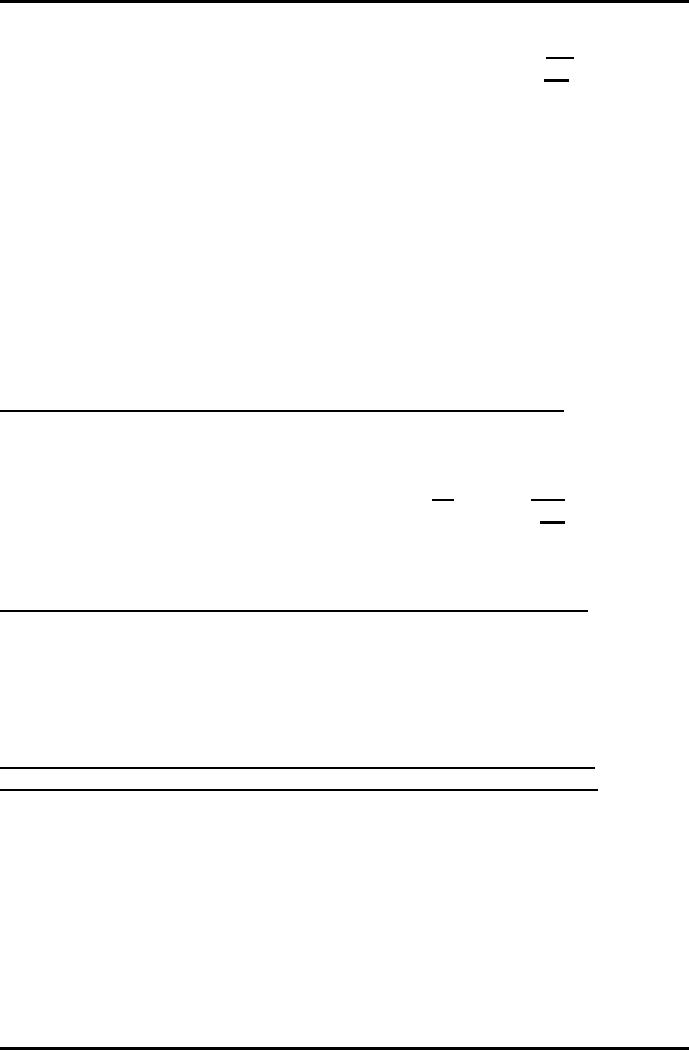

Limited

Liability Company

Income

Statement

For

the Year ended December

31, 2006

(Function

of expenses method)

Rs.

Rs.

Sales

revenue

***

Cost

of goods sold

(***)

Gross

profit

***

Operating

expenses

Administrative

expense

***

Selling

& Marketing expenses

***

(***)

Profit

from operations

***

Other

income

***

Financial

expenses

(***)

Profit

before tax

***

Income

tax expense

(***)

Profit

after tax

***

b)

Nature of expense

method

According

to the nature of expense

method all expenses are

aggregated in the

incomes

statement

and are matched with the

total incomes for the year.

Since both incomes

and

expenses

are of different nature

therefore this method of

preparing Income

Statement

is known as

nature of expense

method.

Limited

Liability Company

Income

Statement

For

the Year ended December

31, 2006

(Nature

of expense method)

Rs.

Rs.

Incomes

Sales

revenue

***

Other

incomes

***

***

Expenses

Increase/decrease

in inventory

***

Raw

materials and consumables

***

Employees'

salaries and wages

***

Utility

bills

***

Other

business operation

expenses

***

(***)

Financial

expenses

(***)

100

Advance

Financial Accounting

(FIN-611)

VU

Profit

before tax

***

Income

tax expense

(***)

Profit

after tax

***

3)

Statement of Changes in

Equity

Statement

of changes in equity is prepared to know

the movement in the items

of

owners'

equity. There might be two types of

the statement:

1.

Statement that shows the

movement in the retained

profits only

2.

Statement that shows the

movement in all the items of

owners' equity

Limited

Liability Company

Statement

of changes in equity

For

the year ended December

31, 2006

(Showing

movement in the retained

profits only)

Rs.

Rs.

Retained

profits b/f

***

Profit

after tax

***

Dividend

paid

***

Transfer

to reserves

***

(***)

Retained

profits c/f

***

(Showing

movement in all items of

owners' equity)

Share

Share

Revaluation Named Retained

Total

Capital

Premium Reserve Reserve

Profits

.

Opening

Balance ***

***

***

***

***

***

Fresh

issue of shares

***

***

***

Revaluation

of Assets

***

***

Profit

after tax

***

***

Dividend

paid

(***)

(***)

Transfer

to named reserves

***

(***)

_

Bonus

Share

***

(***)

(***)

(***)

-_

Totals

***

***

***

***

***

***

.

101

Table of Contents:

- ACCOUNTING FOR INCOMPLETE RECORDS

- PRACTICING ACCOUNTING FOR INCOMPLETE RECORDS

- CONVERSION OF SINGLE ENTRY IN DOUBLE ENTRY ACCOUNTING SYSTEM

- SINGLE ENTRY CALCULATION OF MISSING INFORMATION

- SINGLE ENTRY CALCULATION OF MARKUP AND MARGIN

- ACCOUNTING SYSTEM IN NON-PROFIT ORGANIZATIONS

- NON-PROFIT ORGANIZATIONS

- PREPARATION OF FINANCIAL STATEMENTS OF NON-PROFIT ORGANIZATIONS FROM INCOMPLETE RECORDS

- DEPARTMENTAL ACCOUNTS 1

- DEPARTMENTAL ACCOUNTS 2

- BRANCH ACCOUNTING SYSTEMS

- BRANCH ACCOUNTING

- BRANCH ACCOUNTING - STOCK AND DEBTOR SYSTEM

- STOCK AND DEBTORS SYSTEM

- INDEPENDENT BRANCH

- BRANCH ACCOUNTING 1

- BRANCH ACCOUNTING 2

- ESSENTIALS OF PARTNERSHIP

- Partnership Accounts Changes in partnership firm

- COMPANY ACCOUNTS 1

- COMPANY ACCOUNTS 2

- Problems Solving

- COMPANY ACCOUNTS

- RETURNS ON FINANCIAL SOURCES

- IASBS FRAMEWORK

- ELEMENTS OF FINANCIAL STATEMENTS

- EVENTS AFTER THE BALANCE SHEET DATE

- PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 1

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 2

- BORROWING COST

- EXCESS OF THE CARRYING AMOUNT OF THE QUALIFYING ASSET OVER RECOVERABLE AMOUNT

- EARNINGS PER SHARE

- Earnings per Share

- DILUTED EARNINGS PER SHARE

- GROUP ACCOUNTS

- Pre-acquisition Reserves

- GROUP ACCOUNTS: Minority Interest

- GROUP ACCOUNTS: Inter Company Trading (P to S)

- GROUP ACCOUNTS: Fair Value Adjustments

- GROUP ACCOUNTS: Pre-acquistion Profits, Dividends

- GROUP ACCOUNTS: Profit & Loss

- GROUP ACCOUNTS: Minority Interest, Inter Co.

- GROUP ACCOUNTS: Inter Co. Trading (when there is unrealized profit)

- Comprehensive Workings in Group Accounts Consolidated Balance Sheet