|

SHIFTS IN POTENTIAL OUTPUT AND REAL BUSINESS CYCLE THEORY |

| << EQUILIBRIUM AND THE DETERMINATION OF OUTPUT AND INFLATION |

Money

& Banking MGT411

VU

Lesson

45

SHIFTS

IN POTENTIAL OUTPUT AND REAL BUSINESS

CYCLE THEORY

Changes

in potential output shift the

long-run aggregate supply

curve

At

first the shift has no

impact on the short-run aggregate

supply curve, so inflation and

output

remain

stable

But

with time, the increase in

potential output will mean

that current output is now

below

potential

output, creating a recessionary

output gap, which puts

downward pressure on

inflation,

shifting

the short-run aggregate supply

curve downward

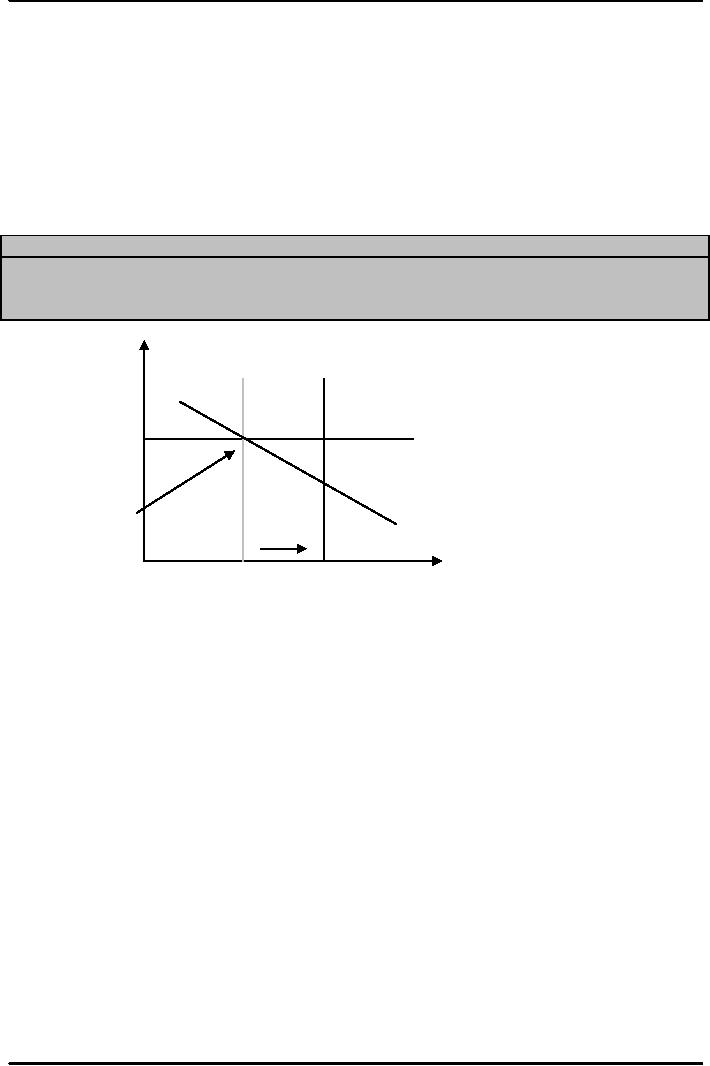

Figure:

The Effects of an increase in potential

Output on Inflation and

Output

An

increase in potential output

shifts the LRAS curve to

the right. In the short

run, current

output

remains unchanged. But since

current output is now below

potential output, the

resulting

recessionary

gap places downward pressure

on inflation and output eventually

begin to rise.

Inflation

(�)

Old

LRAS

New

LRAS

Target

SRAS

Inflation

(�T)

Short

run

equilibrium

is

AD

unchanged

Old

New

Output

(Y)

Potential

Potential

Output

Output

What

happens next depends on what

policymakers do; they

can:

Take

advantage of the downward pressure on

inflation to reduce their

inflation target

Initiate

actions that ensure that

inflation does not

fall.

In

either case, notice that the

higher level of potential

output means a lower

long-term real

interest

rate.

Business

cycle fluctuations can

therefore be explained in terms of

shifts in aggregate

demand

that

change its point of

intersection with a flat

short-run aggregate supply

curve

An

alternative explanation for

business cycle fluctuations

focuses on shifts in potential

output, a

view

called real business cycle

theory.

Real

business cycle

theory

Real

business cycle theory starts

with the assumption that prices

and wages are flexible, so

that

inflation

adjusts rapidly (the

short-run aggregate supply

curve shifts quickly in

response to

deviations

of current output from

potential output).

This

assumption implies that the short-run

aggregate supply curve is

irrelevant: equilibrium

output

and inflation are determined by the

point on the aggregate demand

curve where current

output

equals potential

output

Any

shift in the aggregate demand

curve, regardless of its

source, will change

inflation but not

output

143

Money

& Banking MGT411

VU

Real

business cycle theorists explain

recessions and booms by looking at

fluctuations in

potential

output, focusing on changes in

productivity and their

impact on GDP

The

Impact of a Shift in Aggregate Demand

and Aggregate Supply on Output

and Inflation

Increase

in Aggregate

Positive

Inflation

Increase

in Potential

Demand

Shock

Output

Consumer

Confidence up Labor Costs

up

Capital

in Production up

Source

Business

Optimism up Raw Material Prices up

Labor in Production up

Expected

Inflation up Productivity up

Govt.

Purchases up

Taxes

Down

Exchange

Rate

Depreciates

Short-Run

Y

Increases

Y

falls

Y

unchanged

�

Is

unchanged

�

rises

�

Unchanged

Effects

1.

Recessionary output gap

1.

Recessionary output

1.

Expansionary

Path

of

puts

downward pressure

gap

puts downward

output

gap puts

Adjustment

on

inflation

pressure

on inflation

upward

pressure on

2.

As

Inflation begins to

2.

As

Inflation begins

inflation

fall,

output begins to

to

fall, output begins

2.

As

Inflation begins

rise

to

rise

to

rise, output

begins

to fall

Y

= original potential

Y

= original potential Y = new

potential output

Long-Run

�

=

target (may change)

output

output

Effects

�

=

target (may change)

�

=

target (may

change)

Inflation

will rise

Inflation

will rise

Inflation

will fall

Effects

of

temporarily

unless the

temporarily

unless the temporarily unless

the

Monetary

central

bank changes its central

bank changes its central

bank changes its

Policy

inflation

target.

inflation

target.

inflation

target.

Stabilization

Policy

Monetary

Policy

Policymakers

can shift the aggregate

demand curve by shifting

their monetary policy

reaction

curve,

but they cannot shift the

short-run aggregate supply

curve

They

can neutralize movements in

aggregate demand, but they

cannot eliminate the effects of

an

inflation shock

Shifts

in Aggregate Demand

If

households and businesses become more

pessimistic, driving down aggregate

demand, the

economy

moves into a recession as the

new short-run equilibrium

point is at a current

output

less

than potential

output.

Policymakers

will conclude that the long-run

real interest rate has gone down and

will shift their

monetary

policy reaction curve to the

right, reducing the level of the

real interest rate at every

level

of inflation

This

shifts the aggregate demand

curve back to its initial

position

144

Money

& Banking MGT411

VU

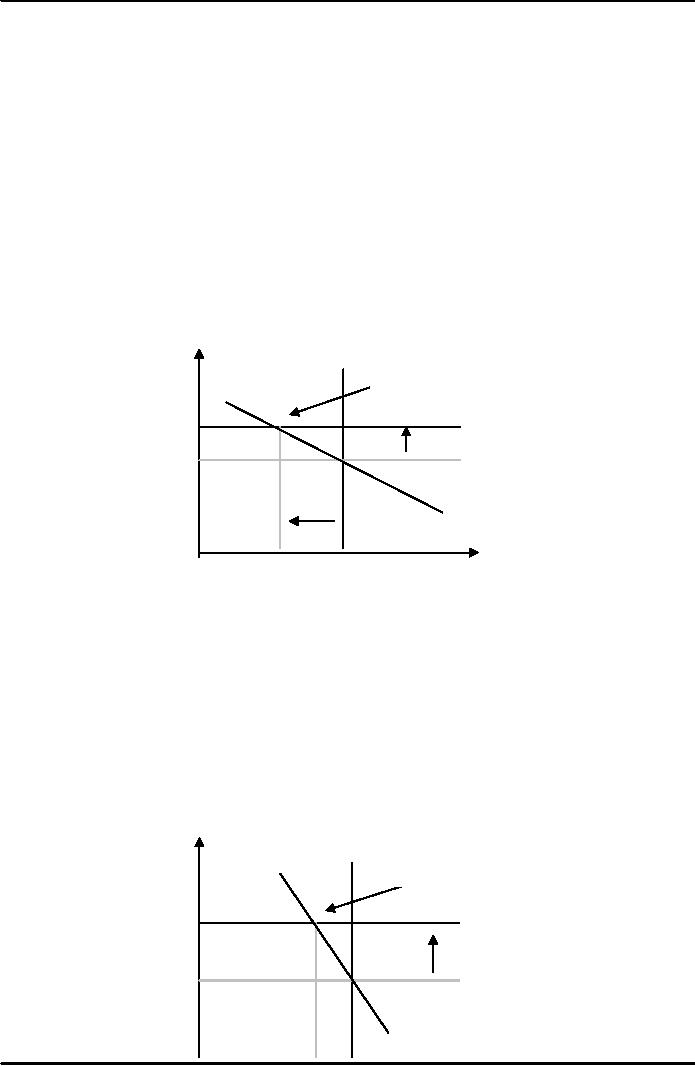

Figure:

Stabilizing a shift in Aggregate

Demand

Following

a drop in consumer or business

confidence, ADC shifts to the

left. to stabilize the

economy,

the

central bank can ease

the policy, shifting the

monetary policy reaction

curve to the right.

This

reduces

the real interest rate at every level of

inflation and shifts the aggregate

demand curve back to

where

it started. Their action

leaves current output and

inflation unchanged.

In

the absence of a policy response,

output would fall; instead,

output remains steady along

with

inflation.

Policymakers

have neutralized the shift in aggregate

demand, keeping current

output equal to

potential

output and current inflation

equal to target

inflation.

Inflation

Shocks and the Policy

Tradeoff

For

policymakers, an inflation shock is an

entirely different

story.

A

positive inflation shock

drives down output and

drives up inflation.

Policymakers

can shift the monetary

policy reaction curve and so

shift the aggregate

demand

curve,

relying on the economy's natural

response to an output gap to bring

inflation back to

target

New

short run

Inflation

(�)

Equilibrium

New

SRAS

Target

Old

SRAS

Inflation

(�T)

Flat

ADC

Current

Potential

Output

(Y)

Output

Output

The

central bank can respond

aggressively to keep Current Inflation

near Target

But

this tool cannot be used to

bring the economy back to its original

long-run equilibrium

point,

because monetary policy can

shift the aggregate demand

curve but not the

short-run

aggregate

supply curve

However,

monetary policymakers can

choose the slope of their monetary

policy reaction curve

and

so affect the slope of the aggregate

demand curve, and in this

way monetary

policymakers

can

choose the extent to which

inflation shocks translate into

changes in output or changes

in

inflation

By

reacting aggressively to inflation

shocks, policymakers force

current inflation back to

target

quickly,

but at a cost of substantial decreases in

output

LRAS

Inflation

(�)

New

short run

equilibrium

New

SRAS

Target

Inflation

Old

SRAS

(�T)

Steep

AD

145

Money

& Banking MGT411

VU

Output

(Y)

Current

Potential

Output

Output

The

central bank can respond

cautiously to Minimize Deviations of

Current Output from

Potential

Output

When

choosing how aggressively to respond to

inflation shocks, central

bankers decide how to

conduct

stabilization policy; they

can stabilize output or

inflation, but not

both

Opportunities

Created by Increased

Productivity

When

productivity rises, potential

output increases. This

shifts the long-run aggregate

supply

curve

to the right, eventually creating a

recessionary gap, which exerts

downward pressure on

inflation.

This

gives policymakers the

opportunity to guide the economy to a

new, lower inflation

target

without

inducing a recession

Since

the increase in potential output

lowers the long-run real interest rate,

rather than reducing

their

inflation target, policymakers

can shift their monetary

policy reaction curve to the

right,

shifting

aggregate demand to the

right.

This

will increase current output

quickly, leaving inflation unchanged at

the target level

Fiscal

Policy

The

people who control the

government's tax and expenditure

policies can stabilize

output and

inflation

too.

Fiscal

policy can be used just

like monetary policy to

neutralize shocks to aggregate

demand

and

stabilize output and

inflation.

Fiscal

policy has two defects: it

works slowly and it is almost impossible

to implement

effectively

Most

recessions are short, data is

available only with a lag,

and it takes time for

Congress to

pass

legislation.

Economics

collides with politics where

fiscal stimulus is concerned as

politicians design

stimulus

packages based more on political

calculation than economic

logic.

Under

most circumstances, then,

stabilization policy should be

left to the central bankers;

fiscal

policy

does have a role but only

after monetary policy has

run its course

♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣♣

146

Table of Contents:

- TEXT AND REFERENCE MATERIAL & FIVE PARTS OF THE FINANCIAL SYSTEM

- FIVE CORE PRINCIPLES OF MONEY AND BANKING:Time has Value

- MONEY & THE PAYMENT SYSTEM:Distinctions among Money, Wealth, and Income

- OTHER FORMS OF PAYMENTS:Electronic Funds Transfer, E-money

- FINANCIAL INTERMEDIARIES:Indirect Finance, Financial and Economic Development

- FINANCIAL INSTRUMENTS & FINANCIAL MARKETS:Primarily Stores of Value

- FINANCIAL INSTITUTIONS:The structure of the financial industry

- TIME VALUE OF MONEY:Future Value, Present Value

- APPLICATION OF PRESENT VALUE CONCEPTS:Compound Annual Rates

- BOND PRICING & RISK:Valuing the Principal Payment, Risk

- MEASURING RISK:Variance, Standard Deviation, Value at Risk, Risk Aversion

- EVALUATING RISK:Deciding if a risk is worth taking, Sources of Risk

- BONDS & BONDS PRICING:Zero-Coupon Bonds, Fixed Payment Loans

- YIELD TO MATURIRY:Current Yield, Holding Period Returns

- SHIFTS IN EQUILIBRIUM IN THE BOND MARKET & RISK

- BONDS & SOURCES OF BOND RISK:Inflation Risk, Bond Ratings

- TAX EFFECT & TERM STRUCTURE OF INTEREST RATE:Expectations Hypothesis

- THE LIQUIDITY PREMIUM THEORY:Essential Characteristics of Common Stock

- VALUING STOCKS:Fundamental Value and the Dividend-Discount Model

- RISK AND VALUE OF STOCKS:The Theory of Efficient Markets

- ROLE OF FINANCIAL INTERMEDIARIES:Pooling Savings

- ROLE OF FINANCIAL INTERMEDIARIES (CONTINUED):Providing Liquidity

- BANKING:The Balance Sheet of Commercial Banks, Assets: Uses of Funds

- BALANCE SHEET OF COMMERCIAL BANKS:Bank Capital and Profitability

- BANK RISK:Liquidity Risk, Credit Risk, Interest-Rate Risk

- INTEREST RATE RISK:Trading Risk, Other Risks, The Globalization of Banking

- NON- DEPOSITORY INSTITUTIONS:Insurance Companies, Securities Firms

- SECURITIES FIRMS (Continued):Finance Companies, Banking Crisis

- THE GOVERNMENT SAFETY NET:Supervision and Examination

- THE GOVERNMENT'S BANK:The Bankers' Bank, Low, Stable Inflation

- LOW, STABLE INFLATION:High, Stable Real Growth

- MEETING THE CHALLENGE: CREATING A SUCCESSFUL CENTRAL BANK

- THE MONETARY BASE:Changing the Size and Composition of the Balance Sheet

- DEPOSIT CREATION IN A SINGLE BANK:Types of Reserves

- MONEY MULTIPLIER:The Quantity of Money (M) Depends on

- TARGET FEDERAL FUNDS RATE AND OPEN MARKET OPERATION

- WHY DO WE CARE ABOUT MONETARY AGGREGATES?The Facts about Velocity

- THE FACTS ABOUT VELOCITY:Money Growth + Velocity Growth = Inflation + Real Growth

- THE PORTFOLIO DEMAND FOR MONEY:Output and Inflation in the Long Run

- MONEY GROWTH, INFLATION, AND AGGREGATE DEMAND

- DERIVING THE MONETARY POLICY REACTION CURVE

- THE AGGREGATE DEMAND CURVE:Shifting the Aggregate Demand Curve

- THE AGGREGATE SUPPLY CURVE:Inflation Shocks

- EQUILIBRIUM AND THE DETERMINATION OF OUTPUT AND INFLATION

- SHIFTS IN POTENTIAL OUTPUT AND REAL BUSINESS CYCLE THEORY