|

Financial

Management MGT201

VU

Lesson

32

FINANCIAL

LEVERAGE AND CAPITAL STRUCTURE

Learning

Objectives:

After

going through this lecture,

you would be able to have an

understanding of the following

topics:

�

Financial

Leverage

�

Capital

Structure

First

we recap some concepts of

previous lectures.

�

WACC

% = rD XD +

rE XE + rP XP.

(Debt, Common Equity, Preferred

Equity)

o

Where "r" is

ACTUAL COST which can be calculated

from REQUIRED ROR

after

accounting

for Taxes & Transaction

Costs.

o

Equity

Capital: If Not Enough Retained Earnings

then Equity Capital must be

financed

by

New Stock Issuance which is

more costly.

�

Total

Risk Faced by FIRM

=

Business Risk + Financial

Risk

�

Higher

Operating Leverage (OL =

Fixed Costs / Total

Costs)

o

Higher

Mean ROE WHEN FIRM'S SALES

> BREAKEVEN POINT

o

Higher

Fixed Costs means Higher

Breakeven Point and More

Chances of Operating

Loss.

Risk of Large Drop in Return

on Equity (ROE) so Higher

Risk.

Financial

Risk:

From

the discussion of the previous lecture we

can infer that

Financial

Risk = Total Standalone Risk

Business Risk

For

example, if

Total

risk as measured by standard

deviation of ROE of levered firm =

30%

and

Business risk as measured by

standard deviation of ROE of un-levered

firm = 20%

then

Financial

Risk = 30% - 20% =

10%

Financial

Risk is created when firms

take loan or debt. As

companies take more debt

they are exposed

to

more financial risk.

Financial

Leverage (FL):

Financial

Leverage shows the effect

that small increase in EBIT

can create much larger

increase in ROE

of

the firm.

Financial

Leverage (%) =Debt /Total

Assets = Debt / Debt +

Equity

If

firm has Rs.1000 of total

assets and Rs.500 debt then

it has 50% (=500/1000)

financial leverage. So

this

firm has 50% leverage

means 50% equity and

50% debt. Practically, firms

increase financial

leverage

by

Issuing New Debt (i.e.

Taking New Loans and

Increase Debt)

OR

Replacing Equity with

New Debt ( Increasing debt

and increasing equity

too)

Financial

Leverage Impact on Risk &

Return of Firm:

Financial

Leverage (or Debt Financing)

generally increases overall

risk & return of a firm.

Let

us

have a look now on a table

that shows how when a

firm becomes levered it

increases the variability

of

ROE and how it increases the

mean ROE.

Effect

of Leverage on ROE Volatility &

Risk

EBIT

Interest

EBT

Tax

Net

Income ROE

(Rs.50)

(30%)

(=NI/Equity)

Un-Levered

600

0

600

180

420

42%

Firm

with

300

0

300

90

210

21%

no

debt or 100%

50

0

50

15

35

3.5%

equity

Levered

firm

600

50

550

165

385

77%

with

debt

300

50

250

75

175

35%

50

50

0

0

0

0%

139

Financial

Management MGT201

VU

This

table shows the effect on ROE as earnings

change from Rs.50 to Rs.600.

This variation in

earnings

can be due to market forces or random

events. This variation in

sales revenue can lead

to

change

in EBIT and this is source of

risk. This will lead to

change in possible values of ROE. Results

of

the

table for levered and

un-levered firm indicate

that leverage (or Debt)

increases the spread or range

of

possible

ROE thereby increasing uncertainty and

risk. Financial Leverage (or

Debt Financing)

generally

increases

overall risk & return of a

firm due to the following

reasons:

�

Increases Return (Mean

ROE):

When EBIT /Total

Assets > Interest Cost

then Financial Leverage is

Good. Small Increase

in

EBIT can create much

larger Increase in ROE. If

EBIT

/Total Assets > Interest

Cost it means firm is

generating profit by the use of

its debt

resulting

in increased ROE as firm has

positive cash flows.

If Equity (and number of shares)

reduced then Return (NI) per

Share Increases. By

reducing

its

equity the firm will

increase its percentage of

debt in capital structure. As the

earnings

are

the same to be distributed among lesser

number of shares due to reduced equity

the

return

will increase per share

resulting in increased ROE.

These

two effects can be visualized in the

following graph:

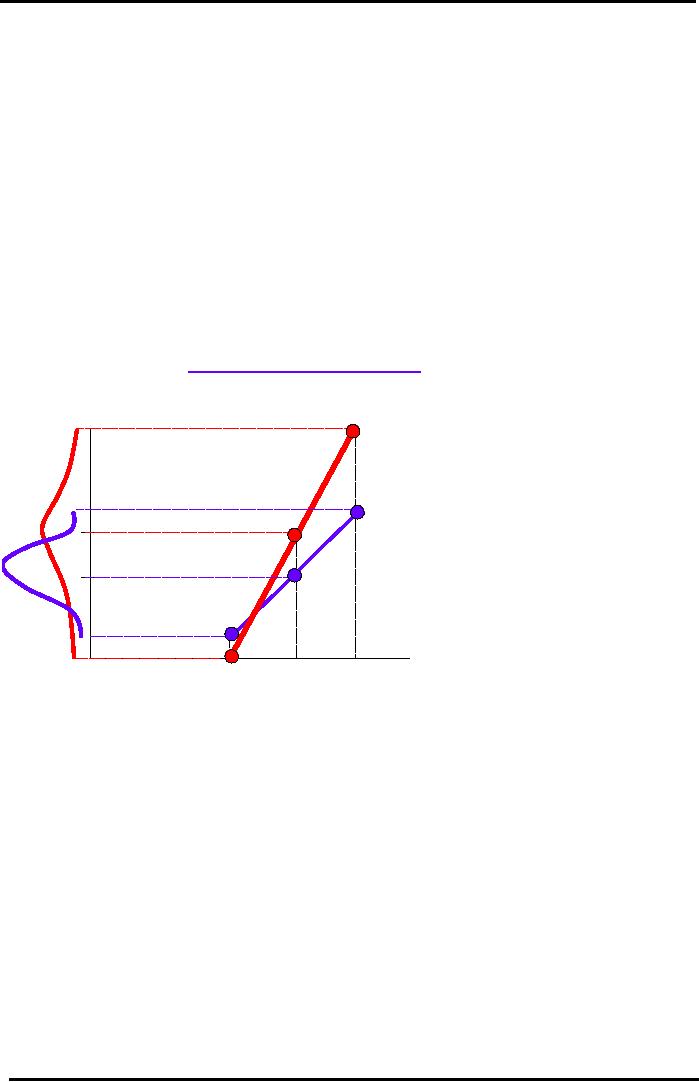

Visualizing

Financial Leverage

(FL)

Impact

on ROE & Capital Structure

LEVERED

(Debt

ROE

(%)

&

Equity) Firm:

77%

Higher

Slope.

ROE

more

sensitive

to

changes

in EBIT

42%

35%

= <ROE>L

UN-LEVERED

(100%

Equity)

21%

= <ROE>UL

Firm.

Safer

Capital

Structure

3.5%

at

Low EBIT's

0%

EBIT

(Rs)

50

300

600

This

is the graphic representation of the above table of

Effect of Leverage on ROE Volatility

& Risk

for

a levered and un levered firm. It

indicates that leverage (or

Debt) increases the spread or range

of

possible

ROE thereby increasing uncertainty and

risk. Range of possible values of ROE have

been

indicated

by straight lines while

level of risk by the probability

distributions.

�

Increases Risk (Standard Deviation

in ROE):

Fixed Interest Dues so

Higher Chances of Losses, No

Dividends for Shareholders.

Possibility

of Large Drop in ROE. Possibly

Default. More Risk

Transferred to

Stockholders.

If Equity (and number of shares)

reduced then Risk per Share

Increases.

This

can also be visualized in the

following graph:

140

Financial

Management MGT201

VU

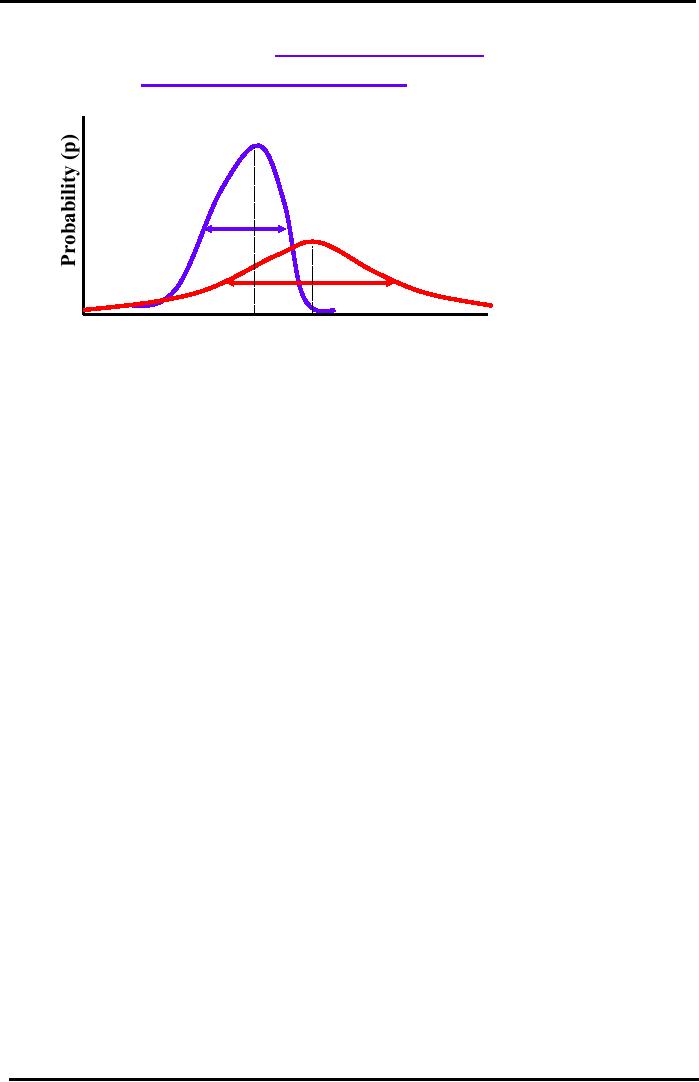

Visualizing

Impact of Financial

Leverage

on

ROE & Capital

Structure

Un-Levered

(100% Equity):

Lower

ROE and Lower Risk.

Levered

(Debt & Equity):

Risk

Higher

ROE but Higher

Risk

Risk

Mean

ROE

Mean

ROE

<ROE>Levered =

<ROE>Un-Levered

=

21%

35%

Return

on Equity ( ROE)%

Capital

Structure Theory:

From

the discussion of Financial leverage we

know Financial Leverage (FL

= Debt / (Debt +

Equity))

Increases

Overall Return (Mean ROE)

when EBIT/Total Assets >

Interest (or Cost of

Debt)

then

Leverage is Good because

small Increase in EBIT

causes much LARGER Increase

in ROE.

Increases

Overall RISK (Standard Deviation of

ROE) of FIRM. Leverage will

always

MAGNIFY

or AMPLIFY a small change in EBIT

into a LARGER change in

ROE.

�

Fundamental Principle in Risk-Return:

Rational Investors in Efficient

Markets will only take

Extra

Risk

if they are compensated by

Sufficient Extra

Return.

�

Should the Management of a Firm

undertake Financial Leverage? If so,

then how much

Debt

should

a Firm have?

Answer provided by Capital

Structure Theory.

Modigliani

- Miller:

�

Fathers of Corporate Finance

�

"Cost of Capital, Corporate Finance

and the Theory of Investment"

Revolutionary Article

Published

by Professors Modigliani & Miller in

American Economic Review in

June 1958.

Won

Nobel Prize.

�

"Pure

M-M" (or Modigliani-Miller) Model - IDEAL

CASE:

There

is no fixed ratio for debt

in capital structure. Generally it varies

with each company's

needs

and

requirements. Capital structure theory tries to

determine the most suitable

ratio for a firm.

Major Assumptions: No Taxes,

No Bankruptcy Costs, Efficient

Markets, Equal

Information

Available to All Investors

Major Conclusions:

�

Capital Structure has no affect on

value of a FIRM! Capital Structure

is

Irrelevant!

�

It does NOT matter how a

firm finances its operations, how

much debt it has

because

it has no bearing on a Firm's

Overall Value as calculated

using NPV!

�

Corporate Financing & Capital

Structure Decisions have no bearing on

Investment

(or Capital Budgeting)

Decisions.

�

Capital Budgeting can be

carried out without knowing

the exact Capital

Structure

of a Firm - you can assume

100% Equity (Un-levered)

Firm.

Keep

in view these conclusions of the theory

are correct only under the

ideal conditions as assumed

by

Modigliani-Miller.

141

Financial

Management MGT201

VU

Modified

MM -

With

Taxes:

In

order to apply it in the real

world for its use,

some other economists made

some modifications. In

order

to make this theory

applicable in the real world and to

account for the effects of corporate

and

personal

taxes on investment decision

and on firm, the effect of

taxes was included in

it.

�

Modigliani-Miller

(With Corporate

Tax)

In most countries, a Firm's

Interest Payments to Bond

Holders are NOT Taxed.

But

Dividend

Payments to Equity Holders

are taxed.

Based on CORPORATE TAXES,

FIRMS should prefer to raise

Capital using DEBT

Financing

rather than equity as there is saving

associated with capital

raised through

this

source.

From

firms point of view interest

payments are source of tax

savings.

�

Merton-Miller

(With Personal

Tax)

In most countries, INVESTORS

(bondholders and shareholders) pay a

higher Personal

Income

Tax on Interest Income from

Bonds than on Dividend Income

from Equity (or

Stocks).

Based on PERSONAL TAXES,

INVESTORS should prefer to

invest in STOCKS (or

Equity).

Uncertain

Conclusion:

Difficult to determine Net

Effect of taxes on optimal

capital structure. But,

practically

speaking, Corporate Tax Effect is

generally stronger so Based on Taxes

alone, Firms should

prefer

Debt.

We

shall discuss other

modifications in Modigliani Miller

capital structure theory along

with the one

discussed

above in the next lecture.

142

Table of Contents:

- INTRODUCTION TO FINANCIAL MANAGEMENT:Corporate Financing & Capital Structure,

- OBJECTIVES OF FINANCIAL MANAGEMENT, FINANCIAL ASSETS AND FINANCIAL MARKETS:Real Assets, Bond

- ANALYSIS OF FINANCIAL STATEMENTS:Basic Financial Statements, Profit & Loss account or Income Statement

- TIME VALUE OF MONEY:Discounting & Net Present Value (NPV), Interest Theory

- FINANCIAL FORECASTING AND FINANCIAL PLANNING:Planning Documents, Drawback of Percent of Sales Method

- PRESENT VALUE AND DISCOUNTING:Interest Rates for Discounting Calculations

- DISCOUNTING CASH FLOW ANALYSIS, ANNUITIES AND PERPETUITIES:Multiple Compounding

- CAPITAL BUDGETING AND CAPITAL BUDGETING TECHNIQUES:Techniques of capital budgeting, Pay back period

- NET PRESENT VALUE (NPV) AND INTERNAL RATE OF RETURN (IRR):RANKING TWO DIFFERENT INVESTMENTS

- PROJECT CASH FLOWS, PROJECT TIMING, COMPARING PROJECTS, AND MODIFIED INTERNAL RATE OF RETURN (MIRR)

- SOME SPECIAL AREAS OF CAPITAL BUDGETING:SOME SPECIAL AREAS OF CAPITAL BUDGETING, SOME SPECIAL AREAS OF CAPITAL BUDGETING

- CAPITAL RATIONING AND INTERPRETATION OF IRR AND NPV WITH LIMITED CAPITAL.:Types of Problems in Capital Rationing

- BONDS AND CLASSIFICATION OF BONDS:Textile Weaving Factory Case Study, Characteristics of bonds, Convertible Bonds

- BONDS’ VALUATION:Long Bond - Risk Theory, Bond Portfolio Theory, Interest Rate Tradeoff

- BONDS VALUATION AND YIELD ON BONDS:Present Value formula for the bond

- INTRODUCTION TO STOCKS AND STOCK VALUATION:Share Concept, Finite Investment

- COMMON STOCK PRICING AND DIVIDEND GROWTH MODELS:Preferred Stock, Perpetual Investment

- COMMON STOCKS – RATE OF RETURN AND EPS PRICING MODEL:Earnings per Share (EPS) Pricing Model

- INTRODUCTION TO RISK, RISK AND RETURN FOR A SINGLE STOCK INVESTMENT:Diversifiable Risk, Diversification

- RISK FOR A SINGLE STOCK INVESTMENT, PROBABILITY GRAPHS AND COEFFICIENT OF VARIATION

- 2- STOCK PORTFOLIO THEORY, RISK AND EXPECTED RETURN:Diversification, Definition of Terms

- PORTFOLIO RISK ANALYSIS AND EFFICIENT PORTFOLIO MAPS

- EFFICIENT PORTFOLIOS, MARKET RISK AND CAPITAL MARKET LINE (CML):Market Risk & Portfolio Theory

- STOCK BETA, PORTFOLIO BETA AND INTRODUCTION TO SECURITY MARKET LINE:MARKET, Calculating Portfolio Beta

- STOCK BETAS &RISK, SML& RETURN AND STOCK PRICES IN EFFICIENT MARKS:Interpretation of Result

- SML GRAPH AND CAPITAL ASSET PRICING MODEL:NPV Calculations & Capital Budgeting

- RISK AND PORTFOLIO THEORY, CAPM, CRITICISM OF CAPM AND APPLICATION OF RISK THEORY:Think Out of the Box

- INTRODUCTION TO DEBT, EFFICIENT MARKETS AND COST OF CAPITAL:Real Assets Markets, Debt vs. Equity

- WEIGHTED AVERAGE COST OF CAPITAL (WACC):Summary of Formulas

- BUSINESS RISK FACED BY FIRM, OPERATING LEVERAGE, BREAK EVEN POINT& RETURN ON EQUITY

- OPERATING LEVERAGE, FINANCIAL LEVERAGE, ROE, BREAK EVEN POINT AND BUSINESS RISK

- FINANCIAL LEVERAGE AND CAPITAL STRUCTURE:Capital Structure Theory

- MODIFICATIONS IN MILLAR MODIGLIANI CAPITAL STRUCTURE THEORY:Modified MM - With Bankruptcy Cost

- APPLICATION OF MILLER MODIGLIANI AND OTHER CAPITAL STRUCTURE THEORIES:Problem of the theory

- NET INCOME AND TAX SHIELD APPROACHES TO WACC:Traditionalists -Real Markets Example

- MANAGEMENT OF CAPITAL STRUCTURE:Practical Capital Structure Management

- DIVIDEND PAYOUT:Other Factors Affecting Dividend Policy, Residual Dividend Model

- APPLICATION OF RESIDUAL DIVIDEND MODEL:Dividend Payout Procedure, Dividend Schemes for Optimizing Share Price

- WORKING CAPITAL MANAGEMENT:Impact of working capital on Firm Value, Monthly Cash Budget

- CASH MANAGEMENT AND WORKING CAPITAL FINANCING:Inventory Management, Accounts Receivables Management:

- SHORT TERM FINANCING, LONG TERM FINANCING AND LEASE FINANCING:

- LEASE FINANCING AND TYPES OF LEASE FINANCING:Sale & Lease-Back, Lease Analyses & Calculations

- MERGERS AND ACQUISITIONS:Leveraged Buy-Outs (LBO’s), Mergers - Good or Bad?

- INTERNATIONAL FINANCE (MULTINATIONAL FINANCE):Major Issues Faced by Multinationals

- FINAL REVIEW OF ENTIRE COURSE ON FINANCIAL MANAGEMENT:Financial Statements and Ratios