|

Financial

Management MGT201

VU

Lesson

25

STOCK

BETAS &RISK, SML& RETURN AND

STOCK PRICES IN EFFICIENT

MARKS

Learning

Objectives:

After

going through this lecture,

you would be able to have an

understanding of the following

topics.

�

Stock

Betas and Risk

�

SML

& Required Returns (CAPM)

�

Stock

Prices in Efficient

Markets

In

the previous lecture, we have mentioned

that the risk that is

relevant in efficient markets

where

the

investors are sensible and

rational is the market risk.

This is because rational investors

maintain

many

stocks and they maintain

diversified portfolio which

contain stocks from

different sectors and

they

manage

to eliminate their diversifiable

risk and the only risk

they faced is the market component of

the

risk.

However, this market component

can not be eliminated and it

will remain because markets

do

fluctuate.

Fluctuation in the Market Index

(KSE 100 index) is a measure

of Market Risk. This

fluctuation

is caused by macro economic and socio

political factors. Rational Investors in

Efficient

Markets

eliminate the Random Company-Specific

Risk through Portfolio

Diversification. So, in

Efficient

Market the only Risk that

remains is Market Risk. And

so, the Price of Efficient Stocks

is

based

on Market Risk only. But the

CAPM based on the fundamental

principal that the rate of return

for

the

stock is directly proportional to the

risk premium and the risk

premium dependent on market

risk

alone

and not the total risk.

Before going into details of

SML we first go through the remaining

topics

related

to beta and its theoretical

calculation based on standard

deviation and covariance. We have

mentioned

that beta of the stocks have tendency of

stock to move with the market. It is

experimentally

possible

to calculate beta of the stock by monitoring the

price or rate of return of the stock and at

the

same

time monitoring the market

index in the same period of

time & comparing that

how the changes in

the

stock market price relate to the

changes in the stock market

index. If you plot them on the

graph

where

you have expected return for stock on Y-

axis and expected return from the stock

market index

slope

of the line from these

points represent the

beta

Stock

Beta measures the Risk of a Stock

Relative to the market.

Beta

Stock A

=

%

Δ

rA* / %

Δ

rM* =

Slope of Regression Line.

Regression Line uses

Experimental

Data.

The

formula that relates beta of

the stock to the standard deviation is as

follows

Beta

Stock A = Covariance of Stock A

with Market / Variance of

Market

=

σ

A

σ

M

ρ

AM

/ σ 2

M

(Covariance

Formula based on Probability &

Statistical Portfolio Theory)

Links Stock Beta

(Market

Portion of Risk) to Stock Standard

Deviation (Total Single

Stock Risk).

Simplified

formula:

=

σ

A

ρ

AM

/ σ M

= market

risk

Theoretical

Beta Example:

Suppose

you have Analyzed the Historical

Time Data for (1) Movements

of the Price (or Return) of

a

Stock A and (2) Movements in the

Value of the Stock

Index.

You

then Apply Simple

Probability Formulas to compute the following Standard

Deviations:

σ

A

= 30%

(Stock A's Total Risk or

Standard Deviation)

σ

M

= 20%

(Stock Market Index Standard

Deviation or Risk)

ρ

AM

= + 0.8

(Correlation between Stock A and the

Market Index)

Compute

the Theoretical Beta of Stock A:

Stock

A Beta = 30% (0.8) / 20% =

24% / 20% = 1.2

108

Financial

Management MGT201

VU

Calculating

Stock Beta

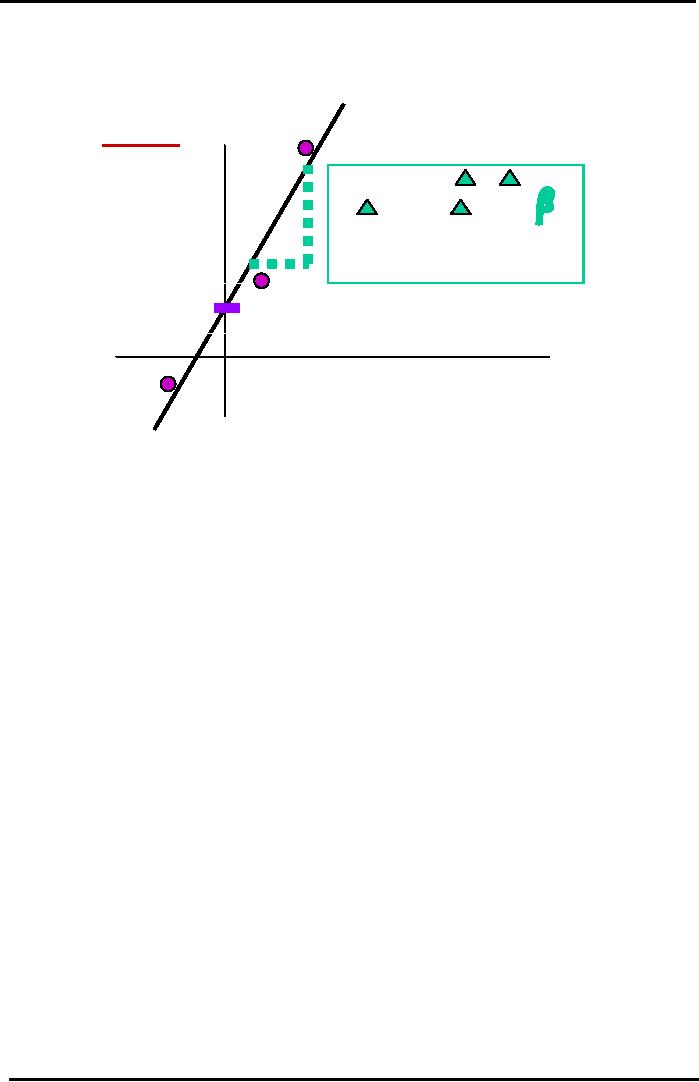

Graphically

Linear

Regression through Annual

Data Points for 3

Years.

CALCULATION

OF BETA

Year

2

BASED

ON EXPERIMENTAL

Expected

DATA

OR OBSERVATION

Return

on

Slope

= Beta =

Y / X

Stock

A

=

% rA* /

% rM*

=

(Historical)

%

A

=Risk

Relative to Market =

rA* - rRF

(rA* - rRF)

/ (rM* - rRF)

Y-Intercept

=

Year

1

Alpha

=

Company

Specific Risk

rM* - rRF

Expected

Return on KSE

100 Market Index

Year

3

(Historical)

%

The

beta of 1.2 shows that stock

is relatively more risky then the

market and if the market

moves

up by 10% this stock will

move up by 12%.

If

all the points of the stock lie on the

straight line then stock

does not have any

diversifiable risk.

The

difference

between the actual data point and the

point which vertically lies

above or below the point is

representative

of the error which is representative of the

company's risk attached to

any stock.

Now

we can put together the two

concepts which we studied up

till now that is

company's

specific

risk and the second concept of

regression line and the distance between

data line and actual

point

of the company's risk. Now, we

can come up with the total

definition of total risk

variances.

Total

variance risk formula:

Total

Risk of Stock A in terms of

Variance (= Std Dev 2)

Total

Risk = Market

Risk + Random

Specific Unique Risk

σ2A

β2A

σ2

M

+

σ

2

A-Error

=

Visualizing

the Variance Risk Formula on

the Regression

Line

If

a Stock is Part of a Totally

Diversified Portfolio then

its Company Risk = 0.

Therefore Total Risk

=

Market Risk. And the Stock

points will lie exactly on

the Regression line.

If

a Stock is a Single Investment

then it carries Company

Specific or Diversifiable or Random

Risk.

This

means that its points

will not lie on the

Regression line. The extent

to which the points

are

scattered

away is a measure of the Variance

Error Term (last term in the

formula)

109

Financial

Management MGT201

VU

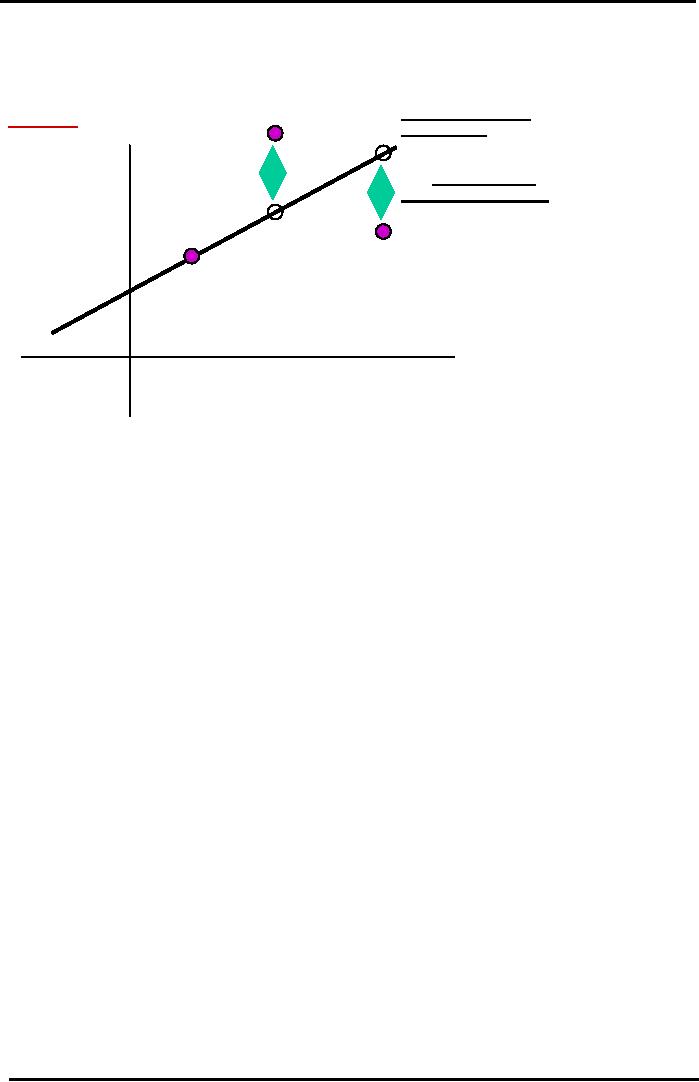

How

Efficiently Priced is Stock A?

A

Regression

(Beta) Line for

Stock

IF

STOCK A WERE

Expected

Return

EFFICIENT,

ALL

on

Stock

A

Error

=

POINTS

WOULD LIE

(Historical)

%

Measure

of

ON

A STRAIGHT LINE

Company

-

AND

TOTAL RISK =

rA* - rRF

Specific

Risk

MARKET

RISK ONLY

Error

=

of

Stock A

Measure

of

Company

-

Specific

Risk

of

Stock A

rM* - rRF

Expected

Return on KSE

100 Market Index (Historical)

%

Variance

Risks Example:

If

the Market Risk = 20% and

Stock A's Beta = 1.5 then

what is the Relevant Market

Risk

Component

of Stock A?

Stock

A's Market Variance = Beta

A2 x

Market Variance = 1.52 x

(20%) 2 = 2.25 x 400%

=

900%

(Variance)

So

the Stock A's Market Risk

(in Standard Deviation terms) =

Square Root of Variance =

30%

=

Beta A σ

M

Note

that Total Risk of Stock A

can be calculated directly by calculating

the Standard Deviation of

the

Possible Future Returns. That

was the first Risk Formula

we studied in Risk

Theory.

Suppose

Total Risk = 35%. Then

Company Specific or Diversifiable or

Random Risk of Stock A =

Total

Risk - Market Risk = 35% -

30% = 5%.

So

86% (= 30/35 x 100) of Stock

A's Total Risk is Market

Risk - quite likely that

Stock A is Part of

a

well Diversified Portfolio or

Mutual Fund.

Security

Market Line (SML)

:

Straight

Line Model is for Beta Risk

and Required Return. Similar to the

Relationship for the 2-

Stock

Portfolio with Ro>0 Beta

Risk is Directly Proportional to

Required Return. The

Investors require

an

extra Return which exactly

compensates them for the extra

Risk of the Stock relative to the

Market.

SML

Linear Equation for the

Required Return of any Stock

A:

rA =

rRF + (rM

- rRF )

β A

In

the above formula

rA

=

Return that Investors

Require from Investment in

Stock A.

rRF

=

Risk Free Rate of Return

(i.e. T-Bill ROR).

rM

=

Return that Investors

Require from Investment in an

Average Stock (or the

Market

Portfolio

of All Stocks where β

M = +

1.0 always).

β

A =

Beta for Stock A. (rM

- rRF

) β

A =

Risk Premium or Additional Return

Required in

Excess

of Risk Free ROR to compensate the

Investor for the Additional

Market Risk of the

Stock

Required

Rate of Return,

Risk

Premium & Market

Risk:

SML

Model for Efficient Markets

establishes a Straight Line

relationship (or Direct

Proportionality)

between

a Stock's Required ROR and its

Risk Premium.

rA

= rRF

+ (rM

- rRF

)

A

A

Stock's Risk Premium depends on

its Market Risk Portion (and

not the Total Risk)

110

Financial

Management MGT201

VU

In

Efficient Markets, Market Price of a

Stock is based on Required

Return which depends

on

Risk

Premium which depends on Stock's

Market Risk Component (and

not the Total Risk).

Stock

Prices in Efficient

Markets:

A

Single Stock Investor who

owns No Stocks and wants to buy a

Share A will have to

face

more

Risk (Market Risk + Specific

Risk) than a Rational Fully

Diversified Investor. The

Single

Stock

Investor will want to buy

the Stock at a lower price to

compensate him for the

higher risk.

However,

Efficient Markets do not

price stocks based on Single

Stock Investors who

want

compensation

for taking on Unnecessary

Company-Specific Risk which

they should have

diversified

away.

Efficient

Markets price the Stocks

based on their Market Risk

Component only. So,

Efficient Stock

Prices

are based on Rational

Investors holding Diversified

Portfolios of many

stocks.

SML

- Numerical Example:

Calculate

the Required Rate of Return

for Stock A given the

following data:

β

A =

2.0 (i.e. Stock A is Twice

as Risky as the Market)

rM

= 20%

pa (i.e. Market ROR or ROR on a Portfolio

consisting of All Stocks or ROR on

the

"Average Stock")

rRF

= 10%

pa (i.e. T-Bill ROR)

SML

Equation (assumes Efficient

Stock Pricing, Risk, and

Return)

rA =

rRF + (rM

- rRF )

β

A

.

=

10% +

(20% - 10%) (2.0) =

30%

Interpretation

of Result:

Investors

require a 30% pa Return from

Investment in Stock A. This is

higher than the

Market

ROR because the Stock (Beta =

2.0) is Riskier than the

Market (Beta = 1.0

always).

If

Required Return (30%) is

higher than Expected Return

(20%) it means that Stock A

is

Unlikely

to Achieve the Investors' Requirement and

Investors will NOT invest in

Stock A.

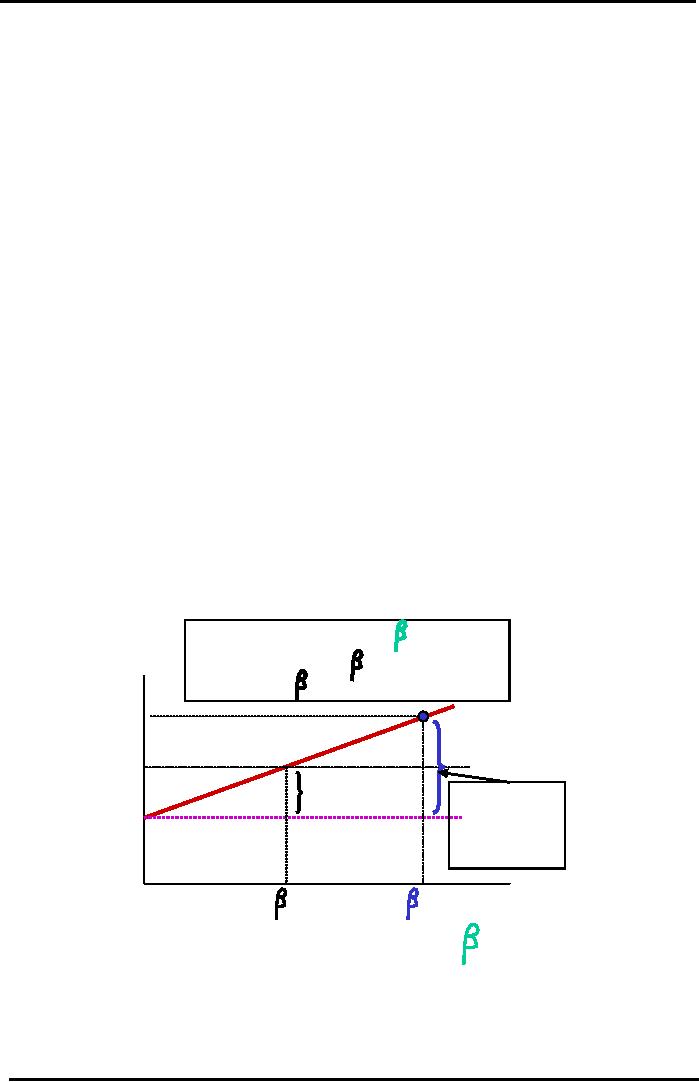

Security

Market Line (SML)

For

Market of Efficient

Stocks

rA = rRF +

(rM -

rRF )

x

A

Required

y

= c + mx where x = and m = Slope

=

(rM -

rRF) / ( M

- 0) =

(rM -

rRF) /1

Return

(r*)

rA= 30%

Security

Market Line

rM=

20%

Market

Risk

Premium

for

Risky

Stock A's

Avg

Stock =

rRF= 10%

Total

Risk

10%

Premium

=

30-10

= 20%

A

=+ 2.0

M

=+ 1.0

Beta

Risk (

)

111

Table of Contents:

- INTRODUCTION TO FINANCIAL MANAGEMENT:Corporate Financing & Capital Structure,

- OBJECTIVES OF FINANCIAL MANAGEMENT, FINANCIAL ASSETS AND FINANCIAL MARKETS:Real Assets, Bond

- ANALYSIS OF FINANCIAL STATEMENTS:Basic Financial Statements, Profit & Loss account or Income Statement

- TIME VALUE OF MONEY:Discounting & Net Present Value (NPV), Interest Theory

- FINANCIAL FORECASTING AND FINANCIAL PLANNING:Planning Documents, Drawback of Percent of Sales Method

- PRESENT VALUE AND DISCOUNTING:Interest Rates for Discounting Calculations

- DISCOUNTING CASH FLOW ANALYSIS, ANNUITIES AND PERPETUITIES:Multiple Compounding

- CAPITAL BUDGETING AND CAPITAL BUDGETING TECHNIQUES:Techniques of capital budgeting, Pay back period

- NET PRESENT VALUE (NPV) AND INTERNAL RATE OF RETURN (IRR):RANKING TWO DIFFERENT INVESTMENTS

- PROJECT CASH FLOWS, PROJECT TIMING, COMPARING PROJECTS, AND MODIFIED INTERNAL RATE OF RETURN (MIRR)

- SOME SPECIAL AREAS OF CAPITAL BUDGETING:SOME SPECIAL AREAS OF CAPITAL BUDGETING, SOME SPECIAL AREAS OF CAPITAL BUDGETING

- CAPITAL RATIONING AND INTERPRETATION OF IRR AND NPV WITH LIMITED CAPITAL.:Types of Problems in Capital Rationing

- BONDS AND CLASSIFICATION OF BONDS:Textile Weaving Factory Case Study, Characteristics of bonds, Convertible Bonds

- BONDS’ VALUATION:Long Bond - Risk Theory, Bond Portfolio Theory, Interest Rate Tradeoff

- BONDS VALUATION AND YIELD ON BONDS:Present Value formula for the bond

- INTRODUCTION TO STOCKS AND STOCK VALUATION:Share Concept, Finite Investment

- COMMON STOCK PRICING AND DIVIDEND GROWTH MODELS:Preferred Stock, Perpetual Investment

- COMMON STOCKS – RATE OF RETURN AND EPS PRICING MODEL:Earnings per Share (EPS) Pricing Model

- INTRODUCTION TO RISK, RISK AND RETURN FOR A SINGLE STOCK INVESTMENT:Diversifiable Risk, Diversification

- RISK FOR A SINGLE STOCK INVESTMENT, PROBABILITY GRAPHS AND COEFFICIENT OF VARIATION

- 2- STOCK PORTFOLIO THEORY, RISK AND EXPECTED RETURN:Diversification, Definition of Terms

- PORTFOLIO RISK ANALYSIS AND EFFICIENT PORTFOLIO MAPS

- EFFICIENT PORTFOLIOS, MARKET RISK AND CAPITAL MARKET LINE (CML):Market Risk & Portfolio Theory

- STOCK BETA, PORTFOLIO BETA AND INTRODUCTION TO SECURITY MARKET LINE:MARKET, Calculating Portfolio Beta

- STOCK BETAS &RISK, SML& RETURN AND STOCK PRICES IN EFFICIENT MARKS:Interpretation of Result

- SML GRAPH AND CAPITAL ASSET PRICING MODEL:NPV Calculations & Capital Budgeting

- RISK AND PORTFOLIO THEORY, CAPM, CRITICISM OF CAPM AND APPLICATION OF RISK THEORY:Think Out of the Box

- INTRODUCTION TO DEBT, EFFICIENT MARKETS AND COST OF CAPITAL:Real Assets Markets, Debt vs. Equity

- WEIGHTED AVERAGE COST OF CAPITAL (WACC):Summary of Formulas

- BUSINESS RISK FACED BY FIRM, OPERATING LEVERAGE, BREAK EVEN POINT& RETURN ON EQUITY

- OPERATING LEVERAGE, FINANCIAL LEVERAGE, ROE, BREAK EVEN POINT AND BUSINESS RISK

- FINANCIAL LEVERAGE AND CAPITAL STRUCTURE:Capital Structure Theory

- MODIFICATIONS IN MILLAR MODIGLIANI CAPITAL STRUCTURE THEORY:Modified MM - With Bankruptcy Cost

- APPLICATION OF MILLER MODIGLIANI AND OTHER CAPITAL STRUCTURE THEORIES:Problem of the theory

- NET INCOME AND TAX SHIELD APPROACHES TO WACC:Traditionalists -Real Markets Example

- MANAGEMENT OF CAPITAL STRUCTURE:Practical Capital Structure Management

- DIVIDEND PAYOUT:Other Factors Affecting Dividend Policy, Residual Dividend Model

- APPLICATION OF RESIDUAL DIVIDEND MODEL:Dividend Payout Procedure, Dividend Schemes for Optimizing Share Price

- WORKING CAPITAL MANAGEMENT:Impact of working capital on Firm Value, Monthly Cash Budget

- CASH MANAGEMENT AND WORKING CAPITAL FINANCING:Inventory Management, Accounts Receivables Management:

- SHORT TERM FINANCING, LONG TERM FINANCING AND LEASE FINANCING:

- LEASE FINANCING AND TYPES OF LEASE FINANCING:Sale & Lease-Back, Lease Analyses & Calculations

- MERGERS AND ACQUISITIONS:Leveraged Buy-Outs (LBO’s), Mergers - Good or Bad?

- INTERNATIONAL FINANCE (MULTINATIONAL FINANCE):Major Issues Faced by Multinationals

- FINAL REVIEW OF ENTIRE COURSE ON FINANCIAL MANAGEMENT:Financial Statements and Ratios