|

DECISION MAKING:Avoidable Costs, Non-Relevant Variable Costs, Absorbed Overhead |

| << DECISION MAKING:Size of fund, Income statement |

| DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS >> |

Cost

& Management Accounting

(MGT-402)

VU

LESSON

# 43

DECISION

MAKING

Relevant

Costs

Relevant

costs are future cash

flows arising as a direct consequence of

a decision.

�

Relevant

costs are future

costs

�

Relevant

costs are cash

flows

�

Relevant

costs are incremental

costs

Decision

making should be based on relevant

costs.

a.

Relevant Costs are future

costs. A decision is about

the future and it cannot

alter what has

been

done already. Costs that

have been incurred in the

past are totally irrelevant

to any

decision

that is being made `now'.

Such costs are past

costs or sunk costs. Costs

that have

been

incurred include not only

costs that have already

been paid, but also

costs that have

been

committed. A committed cost is a

future cash flow that

will be incurred

anyway,

regardless

of the decision taken

now.

b.

Relevant costs are cash

flows. Only cash flow

information is required. This means

that

costs

or charges which do not

reflect additional cash spending (such as

deprecation and

national

costs) should be ignored for

the purpose of decision making.

c.

Relevant costs are incremental

costs. For example, if an

employee is expected to have

no

other

work to do during the next

week, but will be paid his

basic wage (of, say,

Rs. 100 per

week)(

for attending work and

doing nothing, his manager

might decide to give him a

job

which

earns the organization Rs.

40. The net gain is

Rs. 40 and the Rs.

100 is irrelevant to

the

decision because although it is a

future cash flow, it will be

incurred anyway whether

the

employee is given work or

not.

Avoidable

Costs

One

of the situations in which it is

necessary to identify the

avoidable costs is in

deciding

whether

or not to discontinue a product.

The only costs which

would be saved are

the

avoidable

costs which are usually

the variable costs and

sometimes some specific

costs. Costs

which

would be incurred whether or

not he product is discontinued

are known as

unavoidable

costs.

Differential

Costs and Opportunity

Costs

Relevant

costs are also differential

costs and opportunity

costs.

�

Differential

cost is the difference in

total cost between

alternatives.

�

An

opportunity cost is the value of

the benefit sacrificed when

one course of action

is

chosen in preference to an

alternative.

For

example, if decision option A

costs Rs. 300 and

decision option B costs Rs.

360, the

differential

costs is Rs. 60.

Example:

Differential Costs and

Opportunity Costs

Suppose

for example that there

are three options, A, B and

C, only one of which can

be

chosen.

The net profit from

each would be Rs. 80,

Rs. 100 and Rs. 70

respectively.

Since

only one option can be

selected option B would be

chosen because it offers the

biggest

benefit.

234

Cost

& Management Accounting

(MGT-402)

VU

Rs.

Profit

from option B

100

Less

opportunity cost (i.e. the

benefit from the most

profitable alternative, A)

80

Differential

benefit of option B

20

The

decision to choose option B

would not be taken simply

because it offers a profit of

Rs.

100,

but because it offers a

differential profit of Rs. 20 in

excess of the next best

alternative.

Controllable

and Uncontrollable

Costs

We

came across the term

controllable costs at the beginning of

this study text.

Controllable

costs

are items of expenditure

which can be directly

influenced by a given manger within

a

given

time span.

As

a general rule, committed

fixed costs such as those costs

arising form the possession

of

plant,

equipment and buildings

(giving rise to deprecation

and rent) are largely

uncontrollable

in

the short term because

they have been committed by

longer-term decisions.

Discretionary

fixed costs, for example,

advertising and research and

development costs can

be

thought of as being controllable

because they are incurred as

a result of decision made

by

management

and can be raised or lowered at

fairly short notice.

Sunk

Costs

A

sunk cost is a past cost

which is not directly

relevant in decision making. The

principle

underlying

decision accounting is the

management decisions can

only affect the future.

In

decision

making, managers therefore required

information about future

cots and revenues

which

would be affected by the decision

under review. They must

not be misled by

events,

costs

and revenues in the past,

about which they can do

nothing.

Sunk

costs, which have been

charged already as a cost of

sales in a previous

accounting

period

or will be charged in a future

accounting period although the

expenditure had

already

been

incurred, are irrelevant to

decision making.

Example:

Sunk Costs

An

example of a sunk cost is

development costs which have

already been incurred.

Suppose

that

a company has spent Rs.

250,000 in developing a new service

for customers, but

the

marketing

department's most recent findings are

that the service might

not gain customer

acceptance

and could be a commercial failure.

The decision whether or not

to abandon the

development

of the new service would

have to be taken, but the

Rs. 250,000 spent so

far

should

be ignored by the decision makers

because it is a sunk

cost.

Fixed

and Variable

Costs

Unless

you are given an indication to

the contrary, you should

assume the following:

�

Variable

costs will be relevant

costs.

�

Fixed

costs are irrelevant to a

decision.

This

need not be the case,

however, and you should

analyze variable and fixed

cost data

carefully.

Do not forget that `fixed'

costs may only be fixed in

the short term.

Non-Relevant

Variable Costs

There

might be occasions when a

variable cost is in fact a

sunk cost (and therefore a

non-

relevant

variable cost). For example,

suppose that a company has

some units of raw

material

235

Cost

& Management Accounting

(MGT-402)

VU

in

stock. They have been paid

for already, and originally

cost Rs. 2,000. They

are now

obsolete

and are no longer used in

regular production, and they

have no scrap value.

However,

they could be used in a

special job which the

company is trying to decide

whether

to

undertake. The special job is a

`non-off' customer order, and

would use up all

these

materials

in stock.

a.

In deciding whether the job

should be undertaken, the

relevant cost of the

materials

to

the special job is nil.

Their original cost of Rs.

2,000 is a sunk cost, and

should be

ignored

in the decision.

b.

However, if the materials did

have scrap value of, say,

Rs. 300, then their

relevant

cost

to the job would be the

opportunity cost of being unable to

sell them for

scrap,

i.e.

Rs. 300.

Attributable

Fixed Costs

There

might be occasions when a

fixed cost is a relevant

cost, and you must be

aware of the

distinction

`specific' or `directly attributable'

fixed costs, and general

fixed overheads.

Directly

attributable fixed costs are

those costs which, although

fixed within a relevant

range

of

activity level are relevant

to a decision for either of

the following

reasons.

a.

They could increase if certain extra

activities were undertaken. For

example, it may be

necessary

to employ an extra supervisor if a particular

order is accepted. The extra

salary

would

be an attributable fixed

cost.

b.

They would decrease or be eliminated

entirely if a decision were taken

either to reduce

the

scale of operations or shut down

entirely.

General

fixed overheads are those

fixed overheads which will

be unaffected by decisions to

increase

or decreased the scale of operations,

perhaps because they are an

apportioned share

of

the fixed costs of items

which would be completely

unaffected by the decision.

General

fixed

overheads are not relevant

in decision making.

Absorbed

Overhead

Absorbed

overhead is a national accounting

cost and hence should be

ignored for decision

making

purposes. It is overhead incurred

which may be relevant to a

decision.

The

Relevant Cost of Materials

The

relevant cost of raw

materials is generally their current

replacement cost, unless

the

materials

have already been purchased

and would not be replaced

once used. In this case

the

relevant

cost of using them is the

higher of the

following:

�

Their

current resale value

�

The

value they would obtain if

they were put to an alternative

use.

If

the materials have no resale

value and no other possible

use, then the relevant

cost of

using

them for the opportunity

under consideration would be

nil.

236

Cost

& Management Accounting

(MGT-402)

VU

Question

Majeed

Ltd. has been approached by

customer who would like a special

job to be done for

him,

and

who is willing to pay Rs.

22,000 for it. The

job would require the

following materials:

Total

units Units

Book

value

Realizable

Replacement

Material

required

already

in

of units in

value

cost

stock

stock

Rs./unit

Rs./unit

Rs./unit

A

1,000

0

-

-

6

B

1,000

600

2

2.50

5

C

1,000

700

3

2.50

4

D

200

200

4

6.00

9

Material

B is used regularly by Majeed

Ltd, and if units of B are

required for this job, they

would

need

to be replaced to meet other

production demand.

Materials

C and D are in stock as the

result of previous over-buying,

and they have a restricted

use.

No

other use could be found

for material C, but the

units of material D could be used in

another

job

as substitute for 300 units

of material E, which currently costs

Rs. 5 per unit (of

which the

company

has no units in stock at the

moment).

Required:

Calculate

the relevant costs of material

for deciding whether or not

to accept the

contract.

Answer

a.

Material A is not yet owned. It

would have to be bought in

full at the replacement cost

of

Rs.

6 per unit.

b.

Material B is used regularly by the

company. There are existing

stocks (600 units) but

if

these

are used on the contract

under review a further 600

units would be bought

to

replace

them. Relevant costs are

therefore 1,000 units at the

replacement cost of Rs.

5

per

unit.

c.

1,000 units of material C are

needed and 700 are

already in stock. If used for

the contract,

a

further 300 units must be

bought at Rs. 4 each. The

existing stocks of 700 will

not be

replaced.

If they are used for

the contract, they could

not be sold at Rs. 2.50

each. The

realizable

value of these 700 units is an

opportunity cost of sales revenue

forgone.

d.

The required units of material D are

already in stock and will

not be replaced. There is

an

opportunity

cost of using D in the contract

because there are alternative

opportunities

either

to sell the existing stocks

for Rs. 6 per unit

(Rs. 1,200 in total) or avoid

other

purchases

(of material E), which would

cost 300 x Rs. 5 = Rs.

1,500. Since

substitution

for

E is more beneficial, Rs. 1,500 is

the opportunity cost.

e.

Summary of relevant costs:

Rs.

Material

A (1,000 x Rs. 6)

6,000

Material

B (1,000 x Rs. 5)

5,000

Material

C (300 x Rs. 4) plus (700 x

Rs. 2.50)

2,950

Material

D

1,500

Total

15,450

The

Relevant Cost of Labor

The

relevant cost of labor, in

different situation, is best

explained by an example:

237

Cost

& Management Accounting

(MGT-402)

VU

Example:

Relevant Cost of Labor

LW

plc is currently deciding

whether to undertake a new contract. 15

hours of labor will

be

required

for the contract. LW plc

currently products product L,

the standard cost details of

which

are

shown below.

STANDARD

COST CARD

PRODUCT

L

Rs./Unit

Direct

Materials (10kg @ Rs. 2)

20

Direct

Labor (5 hrs @ Rs. 6)

30

50

Selling

price

72

Contribution

22

c.

What

is the relevant cost of

labor if the labor must be

hired form outside

the

organization?

d.

What

is the relevant cost of

labor if LW plc expects to

have 5 hours spare

capacity?

e.

What

is the relevant cost of

labor if labor is in short

supply?

Solution

a.

Where

labor must be hired from

outside the organization, the

relevant cost of labor

will

be

the variable costs

incurred.

Relevant

cost of labor on new

contract = 15 hours @ Rs. 6 =

Rs. 90.

b.

It

is assumed that the 5 hours

spare capacity will be paid

anyway, and so if these 5

hours

are

used on another contract,

there is no additional cost to LW

plc.

Rs.

Direct

labor (10 hours @ Rs.

6)

60

Spare

capacity (5 hours @ Rs.

0)

0

60

c.

Contribution

earned per unit of Product L

produced = Rs. 22

If

it requires 5 hours of labor to

make one unit of product L,

the contribution earned per

labor

hour

= Rs. 22/5 = Rs.

4.40.

Rs.

Direct

labor (15 hours @ Rs.

6)

90

Contribution

lost by not making product L

(Rs. 4.40 x 15 hours)

66

156

It

is important that you should

be able to identify the

relevant cost which are

appropriate to a

decision.

In many cases, this is a

fairly straightforward problem,

but there are cases where

great

care

should be taken. Attempt the

following question:

Question:

A

company has been making a machine to

order for a customer, but

the customer has since

gone

into

liquidation, and there is no prospect

that nay money will be obtained

from the winding up

of

the

company. Costs incurred to

date in manufacturing the machine

are Rs. 50,000 and

progress

payments

of Rs. 15,000 had been

received from the customer

prior to the

liquidation.

The

sales department has found

another company willing to

buy the machine for Rs.

34,000 once

it

has been completed.

To

complete the work, the

following costs would be

incurred.

a.

Materials:

These have been bought at a

cost of Rs. 6,000. They

have no other use, and

if

the

machine is not finished, they

would be sold for scrape for

Rs. 2,000.

238

Cost

& Management Accounting

(MGT-402)

VU

b.

Further

labor costs would be Rs.

8,000. Labor is in short

supply, and if the machine

is

not

finished, the work force

would be switched to another job,

which would earn Rs.

30,000 in

revenue,

and incur direct costs of

Rs. 12,000 and absorbed

(fixed) overhead of Rs.

8,000.

c.

Consultancy

fees Rs. 4,000. If the

work is not completed, the

consultant's contract

would

be

cancelled at a cost at Rs.

1,500.

d.

General

overheads of Rs. 8,000 would

be added to the cost of the

additional work.

Required:

Assess

whether the new customer's

offer should be

accepted.

Answer:

a.

Costs

incurred in the past, or revenue

received in the past are

not relevant because

they

cannot

affect a decision about what

is best for the future.

Costs incurred to date of

Rs. 50,000 and

revenue

received of Rs. 15,000 are

`water under the bridge' and

should be ignored.

b.

Similarly,

the price paid in the

past for the materials is

irrelevant. The only

relevant cost

of

materials affecting the

decision is the opportunity

cost of the revenue from

scrap which would

be

forgone Rs.

2,000.

c.

Labor

costs Rs Labor costs required to complete

work 8,000 opportunity

costs:

Contribution

forgone by losing other work

Rs. (30,000

12,000)

18,000

Relevant

cot of labor

26,000

d.

The

incremental cost of consultancy

from completing the work is

Rs. 2,500.

Rs.

Cost

of completing work

4,000

Cost

of canceling contract

1,500

Incremental

cost of completing

work

2,500

e.

Absorbed

overhead is a national accounting

cost and should be ignored.

Actual overhead

incurred

is the only overhead cost to

consider. General overhead costs (and the

absorbed overhead

of

the alternative work for

the labor force) should be

ignored.

f.

Relevant

costs may be summarized as

follows:

Rs.

Rs.

Revenue

from completing work

34,000

Relevant

Costs:

Materials:

Opportunity

cost

2,000

Labor:

Basic

pay

8,000

Opportunity

Cost

18,000

Incremental

cost of consultant

2,500

30,500

Extra

profit to be earned by accepting

the order

3,500

The

Deprival Value of an

Asset

The

deprival value of an asset represents the

amount of money that a

company would have to

receive

if it were deprived of an asset in order

to be no worse off than it

already is.

The

deprival value of an asset is best demonstrated by

means of an example.

239

Cost

& Management Accounting

(MGT-402)

VU

Example:

Deprival Value of an

Asset

A

machine cost Rs. 14,000 ten

years ago. It is expected

that the machine will

generate future

revenues

of Rs. 10,000. Alternatively,

the machine could be scrapped

for Rs. 8,000. An

equivalent

machine

in the same condition would

cost Rs. 9,000 to buy

now. What is the deprival value of

the

machine?

Solution

Firstly,

let us think about the

relevance of the costs given to us in

the question.

Cost

of machine = Rs. 14,000 = past/sunk

cost

Future

revenues = Rs. 10,000 = revenue

expected to be generated

Net

realizable value = Rs. 8,000 =

scrap proceeds

Replacement

cost = Rs. 9,000

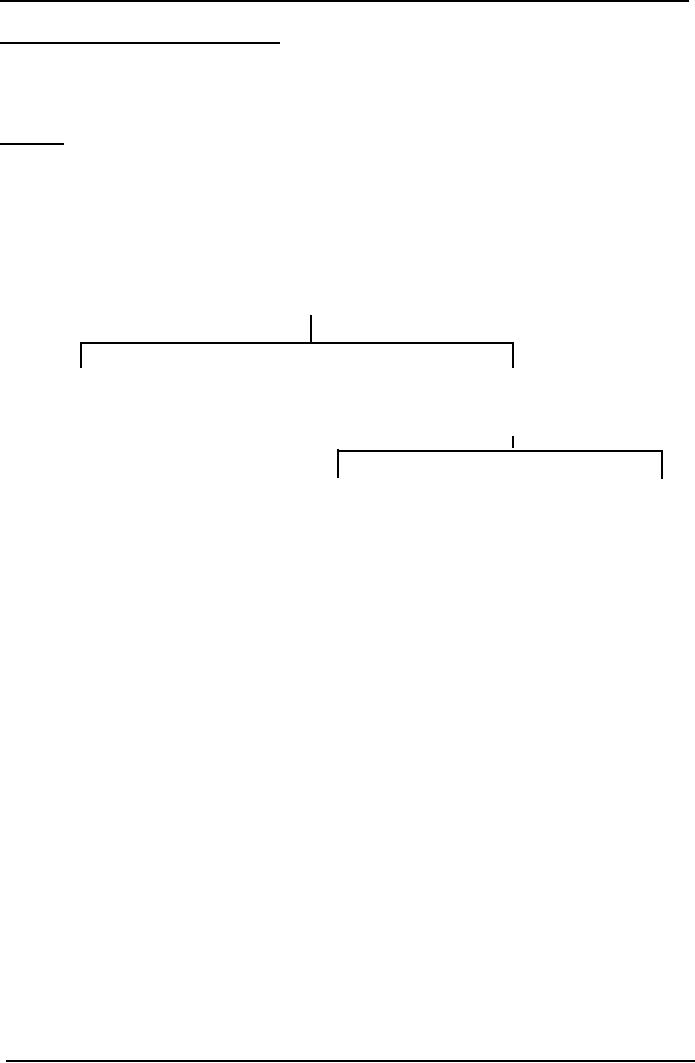

When

calculating the deprival value of an

asset, use the following

diagram.

Lower

of

Replacement

Revenue

Cost

Expected

(Rs.

9,000)

(Rs.

10,000)

Higher

of

NRV

(Rs.

10,000)

(Rs.

8,000)

Therefore,

the deprival value of the machine is the

lower of the replacement

cost and Rs.

10,000.

The

deprival value is therefore Rs.

9,000.

240

Table of Contents:

- COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION:COST CLASSIFICATION,

- IMPORTANT TERMINOLOGIES:Cost Center, Profit Centre, Differential Cost or Incremental cost

- FINANCIAL STATEMENTS:Inventory, Direct Material Consumed, Total Factory Cost

- FINANCIAL STATEMENTS:Adjustment in the Entire Production, Adjustment in the Income Statement

- PROBLEMS IN PREPARATION OF FINANCIAL STATEMENTS:Gross Profit Margin Rate, Net Profit Ratio

- MORE ABOUT PREPARATION OF FINANCIAL STATEMENTS:Conversion Cost

- MATERIAL:Inventory, Perpetual Inventory System, Weighted Average Method (W.Avg)

- CONTROL OVER MATERIAL:Order Level, Maximum Stock Level, Danger Level

- ECONOMIC ORDERING QUANTITY:EOQ Graph, PROBLEMS

- ACCOUNTING FOR LOSSES:Spoiled output, Accounting treatment, Inventory Turnover Ratio

- LABOR:Direct Labor Cost, Mechanical Methods, MAKING PAYMENTS TO EMPLOYEES

- PAYROLL AND INCENTIVES:Systems of Wages, Premium Plans

- PIECE RATE BASE PREMIUM PLANS:Suitability of Piece Rate System, GROUP BONUS SYSTEMS

- LABOR TURNOVER AND LABOR EFFICIENCY RATIOS & FACTORY OVERHEAD COST

- ALLOCATION AND APPORTIONMENT OF FOH COST

- FACTORY OVERHEAD COST:Marketing, Research and development

- FACTORY OVERHEAD COST:Spending Variance, Capacity/Volume Variance

- JOB ORDER COSTING SYSTEM:Direct Materials, Direct Labor, Factory Overhead

- PROCESS COSTING SYSTEM:Data Collection, Cost of Completed Output

- PROCESS COSTING SYSTEM:Cost of Production Report, Quantity Schedule

- PROCESS COSTING SYSTEM:Normal Loss at the End of Process

- PROCESS COSTING SYSTEM:PRACTICE QUESTION

- PROCESS COSTING SYSTEM:Partially-processed units, Equivalent units

- PROCESS COSTING SYSTEM:Weighted average method, Cost of Production Report

- COSTING/VALUATION OF JOINT AND BY PRODUCTS:Accounting for joint products

- COSTING/VALUATION OF JOINT AND BY PRODUCTS:Problems of common costs

- MARGINAL AND ABSORPTION COSTING:Contribution Margin, Marginal cost per unit

- MARGINAL AND ABSORPTION COSTING:Contribution and profit

- COST – VOLUME – PROFIT ANALYSIS:Contribution Margin Approach & CVP Analysis

- COST – VOLUME – PROFIT ANALYSIS:Target Contribution Margin

- BREAK EVEN ANALYSIS – MARGIN OF SAFETY:Margin of Safety (MOS), Using Budget profit

- BREAKEVEN ANALYSIS – CHARTS AND GRAPHS:Usefulness of charts

- WHAT IS A BUDGET?:Budgetary control, Making a Forecast, Preparing budgets

- Production & Sales Budget:Rolling budget, Sales budget

- Production & Sales Budget:Illustration 1, Production budget

- FLEXIBLE BUDGET:Capacity and volume, Theoretical Capacity

- FLEXIBLE BUDGET:ANALYSIS OF COST BEHAVIOR, Fixed Expenses

- TYPES OF BUDGET:Format of Cash Budget,

- Complex Cash Budget & Flexible Budget:Comparing actual with original budget

- FLEXIBLE & ZERO BASE BUDGETING:Efficiency Ratio, Performance budgeting

- DECISION MAKING IN MANAGEMENT ACCOUNTING:Spare capacity costs, Sunk cost

- DECISION MAKING:Size of fund, Income statement

- DECISION MAKING:Avoidable Costs, Non-Relevant Variable Costs, Absorbed Overhead

- DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS

- DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS:MAKE OR BUY DECISIONS