|

Cost

& Management Accounting

(MGT-402)

VU

LESSON#

19

PROCESS

COSTING SYSTEM

(An

introduction)

Definition

Process

costing system applies when

standardised goods are produced

tom a series of

inter-

connected

operations.

In

some industries, the output produced

emerges from a continuous

process. An example might

be

an

oil refinery; Oil in a raw

state is input and subjected

to a process of purification. Refined

oil

emerges

at the end of the

process.

Problems

that arise in such situations include

the attribution of materials

costs and conversion

costs

to units of finished output

and the occurrence of losses

during the process (spoilt

or lost

production).

The

characteristics and application of

process costing

Continuous

production

In

the job order costing, costs

were directly allocated to a

particular job. When

standardised goods

or

services result from a

sequence of repetitive and continuous

operations, it is useful to work

out

the

cost of each operation. Then

because every unit produced may be

assumed to have

involved

the

same amount of work, costs

for a period are charged to

processes or operations, and unit

costs

are

ascertained by dividing process

costs by the quantity of

output units produced This is

know n

as

process costing.

Series

of interconnected operations

Process

costing applies when standardised

goods are produced from a

series of interconnected

operations.

Process costing system is employed by industries

possessing following

characteristics:

1.

There is mass production of a

single product or two or

more products in successive

runs

of

scheduled duration e.g.,

vegetable canning or fruit juice

bottling.

2.

All units of output are

exactly similar and are produced by the

same manufacturing

process.

3.

Entire manufacturing process is divided

into departments or processes, each

performing a

specific

set of operations.

4.

Completed output of each department,

except the last one, is the

raw materials for the

next

department.

5.

Manufacturing operations may result in

production of joint products or by

products.

6.

Production is not in response to

customers' orders but in anticipation of

demand.

Examples

of industries using

Process Costing include:

Bottling,

Pharmaceuticals, Cement, Paint, Coal, Distilleries

Electricity, Ice, Soap,

Sugar, Canning,

Chemicals,

Cooking oil, Electric

appliances, Flour, Natural

gas, Petroleum Products, Rubber,

Steel,

Textile.

Under process costing, for

the purpose of cost control,

each department involved

in

manufacturing

process is regarded as a cost centre

and product costs are

accumulated separately

for

each department. Cost

Centre means a

division or segment for which an

individual is made responsible

.for

the incurrence of cost

Departmental

costs are passed through

department work in process accounts

and not through a

single

work in process control

account as in job costing. As all

units are produced from the

same

raw

materials and by same

manufacturing operations, therefore, it is

assumed that same cost

is

chargeable

to each unit. Instead of accumulating

cost of individual units, an

average unit cost is

computed

by dividing total cost by

total output of the period.

Cost is associated only

with

departments

and not with jobs. It

reduces clerical efforts for

accumulation and analysis of

cost. In

this

way process costing is less

expensive, as

compared with job

costing.

133

Cost

& Management Accounting

(MGT-402)

VU

The

Process Cost Sheet also

called Cost

of Production Report is the

basic document in process

costing.

This document is prepared

for each department and

shows the quantities processed,

total

and

unit cost, and cost of

work transferred out, and

still in process. .

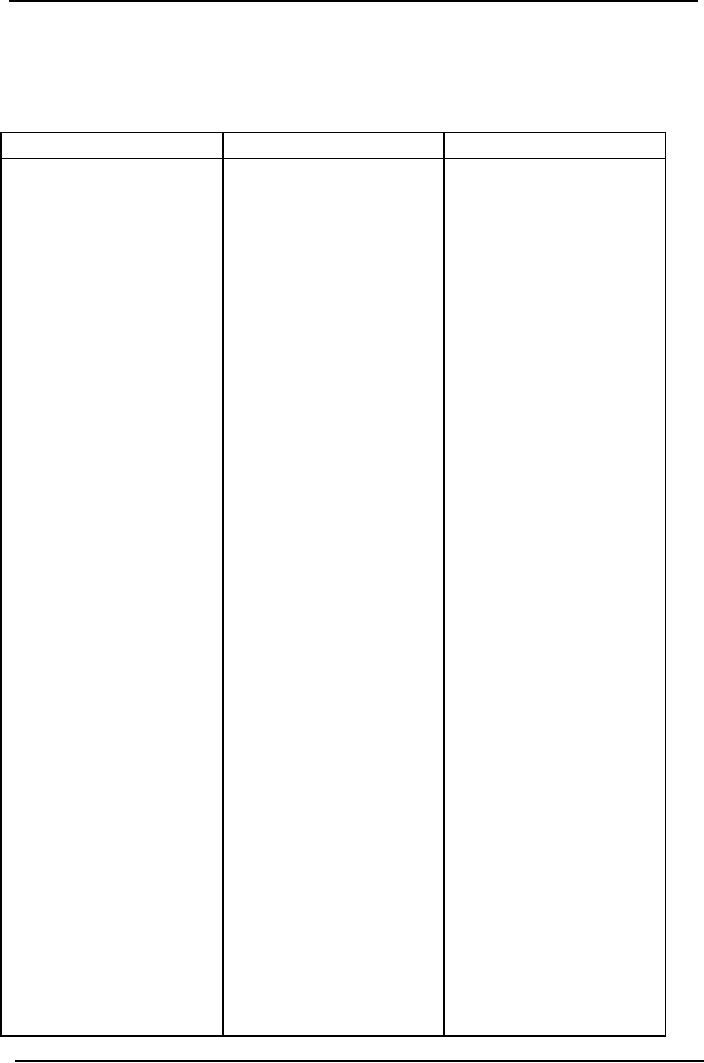

Following

table is meant to make the

difference between the two

costing systems more

clear.

Job

order costing system

Process

costing system

Where

different products

Application

Where

single standard

having

peculiar

product

is produced or

specifications

are produced

two

or more standard

against

customers' orders

products

are produced in

successive

runs.

Production

is for stock

and

in anticipation of

demand.

In

order to determine cost

Accumulation

of Cost

of

each job, costs

are

Costs

are associated

only

compiled

job wise. At the

same

time, to evaluate

with

departments

efficiency

of departmental

management

cost are also

compiled

department wise

Unit

cost is computed on

completion

of job. The job

may

itself be a single

cost

Cost

per unit

unit

e.g. a machine or it may

An

average unit cost is

be

a multi unit

computed

at the end of

costing

period by dividing

total

cost by units of

output

Only

one work in process

of

the period.

control

account is

maintained

A

separate work in process

control

account

is

More

clerical efforts are

Work

in process a/c

maintained

for

each

needed

to accumulate costs

producing

department

by

jobs and by departments,-

therefore,

the system is more

Cost

accumulation is simple

expensive

as

costs are accumulated

only

Cost

of operating the system

by

departments; therefore,

the

system is comparatively

less

expensive.

134

Cost

& Management Accounting

(MGT-402)

VU

Process

costing procedures

In

process costing industries standard

products are produced in accordance

with production

budget.

Therefore, it becomes unnecessary to

issue a production order.

Production Planning

and

Control

Department communicates production

targets to departmental heads by means of

written

letters.

Data of quantities produced by each department are

collected and compared with

budgeted

quantities

for control purposes. These

information are collected by departmental

supervisors or

quality

inspectors may recording these

data. Each producing department is a

cost centre because

for

the purpose of cost control

management is interested in ascertaining

departmental costs.

In

process costing, generally, a separate

work in process account is maintained

for each producing

department.

Data

Collection

Collection

of departmental cost figures of direct materials,

direct labor and factory

overhead is

based

on similar procedure as for, job order

costing. However, the source

documents used for

the

data

collection are comparatively simple.

These documents identify

costs only with

departments

and

not with jobs as

well.

Direct

Materials:

Production

people secure materials by

issuing properly authorised Materials

Requisitions. At the

end

of each month, these requisitions

are sorted and a Materials Requisition

Summary indicating

cost

of direct and indirect materials

issued to each department is

prepared. Monthly totals

of

direct

and indirect materials

issued are debited to departmental

work in process control

accounts

and

factory overhead control

account respectively and credited to

materials control

account.

Direct

Labor:

Instead

of using Job Time Tickets,

labor cost data are

accumulated on Clock Cards and

Daily

Time

Sheets. These documents show

labor time utilized by each

department and classification of

labor

cost as direct and indirect. At

the end of each month,

labor cost data accumulated on

these

source

documents are summarised in

Labor Cost Analysis Sheet indicating

direct and indirect

labor

cost for each department.

Monthly totals of direct labor

are debited to departmental work

in

process

accounts and indirect labor is

debited to factory overhead

control account.

Factory

Overhead:

Factory

overhead costs, other than

indirect materials and

indirect labor discussed earlier,

are

accumulated

in Voucher Register and in General

Journal by means of adjusting entries

for

depreciation,

expired insurance etc, Monthly

total, are debited to

factory overhead

control

account.

Factory

overhead is charged to production

through predetermined departmental factory

overhead

applied

rates. Some industries using process

costing charge actual factory

overhead to

departments.

This method gives satisfactory results if

production is stable from

month to month,

But

if there are fluctuations in

production volume, charge of

actual factory overhead

is

unsatisfactory

especially when considerable

portion of factory overhead is a

fixed cost,

Cost

of Completed Output:

Cost

of completed output of each production

department is calculated in Cost of

Production

Report.

Cost of units completed and

transferred out is credited to

work in process control

account

of

the respective department

and debited to work in

process control account of

the department

receiving

the units. Cost transferred

out by the last department

is, however, debited to

finished

goods

control account

135

Cost

& Management Accounting

(MGT-402)

VU

Cost

of Production Report

In

process costing Cost of Production

Report also called Process

Cost Sheet is the

key

document.

At the end of costing period, generally a

month, a Cost of Production

Report is

prepared.

It summarizes the data of

quantity produced and cost

incurred by each

producing

department.

It also serves as a source

document for passing

accounting entries at the

end of

costing

period.

Cost

of production report is divided into

five

sections.

Each section is meant to provide

specific

information.

A brief description of these sections is

presented below:

1.

Quantity

schedule.

2.

Cost

accumulated in the department/process.

3.

Calculation

of equivalent units produced.

4.

Calculation

of cost per unit.

5.

Accounting

treatment / apportionment of the accumulated

cost

Quantity

Schedule:

The

first section Quantity

Schedule contains input and

output data in terms of quantities.

The

information

is presented in the following

order.

(i)

Units

in process at the beginning of costing

period.

(ii)

Units

started in process or received

from preceding department

during the period.

(Total

of (i) and (ii) constitutes

total units to be accounted

for)

(iii)

Units

completed and transferred to next

department or to finished

goods.

(iv)

Units

completed but still in the

department.

(v)

Units

in process at the end of the

period and their degree of

completion.

(vi)

Units

lost in process during the

period indicating whether normal loss or

abnormal loss.

The

stage of completion at which

the loss occurs is also

specified.

(Total

of (iii) , (iv) , (v) and

(vi) is again the total

units to be accounted for)

The

quantity schedule assists

management to look at a glance

production performance of

departments

as well as it provides necessary data

for preparing remaining sections of the

report.

Cost

accumulated in the department/process.

The

second section Cost

Accumulated to Departments shows

total cost for which

the

departments

are accountable. Total costs

include cost of beginning work in

process inventory,

cost

transferred in from the

preceding department and

cost of direct materials, direct labor

and

factory

overhead added by the

department. If there is normal

loss of units, unit cost

received

from

preceding department requires

adjustment. This adjustment

for lost units is also

shown in

this

section. This section provides

data for debiting work in

process control accounts of

the

departments.

Calculation

of equivalent units produced.

In

order to arrive at cost per

unit of output, total of

each cost element is divided by the

number of

units

produced, For this purpose, where at the

end of costing period, there are

some partially

completed

units in process, these

units must be stated in terms of

equivalent completed units,

For

example,

if 4,000 units. are in

process at the end of month

estimated as 50% complete, these

will

be

equivalent to 2,000 completed units.

These equivalent units are

added to units completed by

the

department to arrive at equivalent

production. Then total cost

is divided by this equivalent

production

figure to calculate unit

cost.

136

Cost

& Management Accounting

(MGT-402)

VU

Calculation

of cost per unit

In

process costing, costs are

averaged over the units

produced. The costs accumulated to a

process

for

a period are collected and divided by the

number of units equally produced during

the period.

Accounting

treatment / apportionment of the

accumulated cost

The

last section presents a

summary to the explaining

the accounting treatments of the

costs

incurred

in the department. This includes

(i)

Adjustment

for lost units for

normal loss, if any.

(ii)

Cost

transferred out.

(iii)

Cost

of abnormal loss, if

any.

(iv)

Cost

of work in process ending inventory

and

(v)

Any

other accounting adjustment, if

necessary to present.

Cost

of production report is generally

presented to management with

supplementary reports of

usage

of materials, labor and

factory overhead.

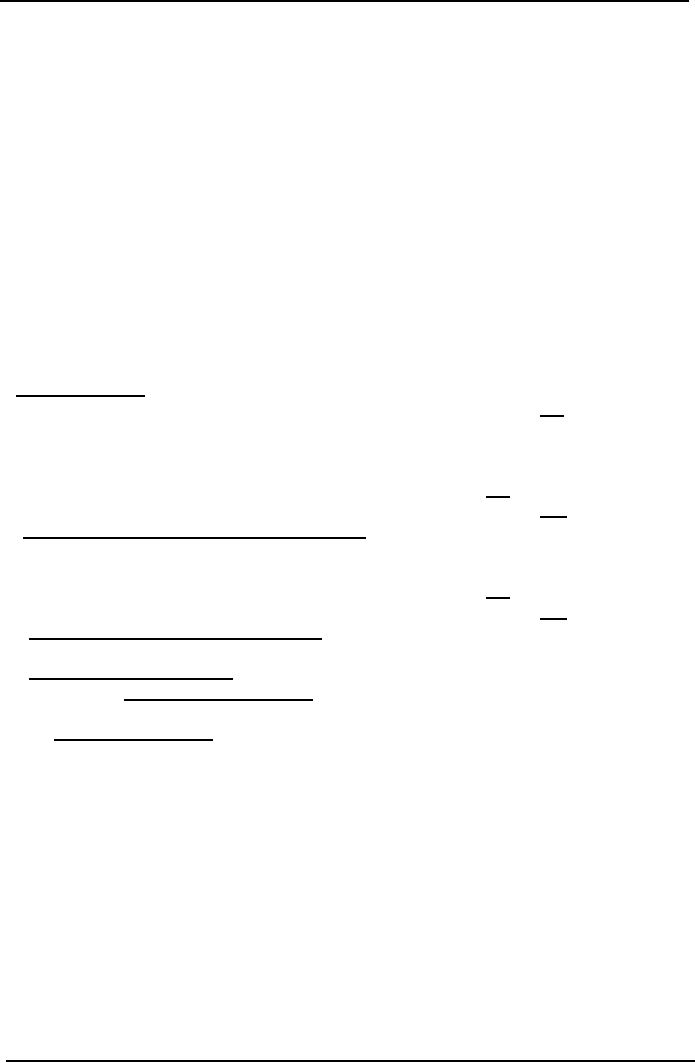

Standard

format of a simple

Cost

of Production Report

I-

Quantity Schedule:

Units

put into the

process

***

Units

completed in this process &

transferred

to

next department.

***

Units

not yet completed at the end

of the

Period.

***

***

II-

Cost Accumulated In The

Department / Process:

Direct

Material Cost

***

Direct

Labor

***

Factory

Overhead (Applied)

***

***

III-

Calculation of Equivalent Units

Produced

100%

of completed units + % completed of the in

process units

IV-

Calculation Of Per Unit

Cost

=

Total

Cost

.

Equivalent

Units Produced

V-

Accounting

Treatment

1-

Finished goods

2-

Closing Work in process

137

Cost

& Management Accounting

(MGT-402)

VU

Problem

Questions

Q.

1

Heera

Manufacturing Company manufactures a

product. Production made and

manufacturing

costs

incurred in the first

department during the month

of October .are given

below:

10,000

units were started in

process out of which 9,400

units were transferred to

next department

and

remaining 600 units were 1/2

complete as to materials, labor and

overhead. Direct

materials

Rs.

19,400, direct labor Rs.

24,250 and factory overhead

Rs. 14,550 was charged to

production.

Required: Cost

of production report for the

month.

Q.

2

Production

and cost data of first

production department of Excellent

Manufacturing Company

for

the

month of March 2006 are as

follow:

Units

started in process were

5,000. Units completed and

transferred to second department

were

4,500.

Remaining units were in process

estimated to be 50%, 40%,

60% completed as to materials,

labor

and factory overhead respectively.

Costs of materials, labor

and overhead were Rs.

50,000,

Rs.

60,000 and Rs. 40,000

respectively.

Required:

Cost

of production report.

138

Table of Contents:

- COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION:COST CLASSIFICATION,

- IMPORTANT TERMINOLOGIES:Cost Center, Profit Centre, Differential Cost or Incremental cost

- FINANCIAL STATEMENTS:Inventory, Direct Material Consumed, Total Factory Cost

- FINANCIAL STATEMENTS:Adjustment in the Entire Production, Adjustment in the Income Statement

- PROBLEMS IN PREPARATION OF FINANCIAL STATEMENTS:Gross Profit Margin Rate, Net Profit Ratio

- MORE ABOUT PREPARATION OF FINANCIAL STATEMENTS:Conversion Cost

- MATERIAL:Inventory, Perpetual Inventory System, Weighted Average Method (W.Avg)

- CONTROL OVER MATERIAL:Order Level, Maximum Stock Level, Danger Level

- ECONOMIC ORDERING QUANTITY:EOQ Graph, PROBLEMS

- ACCOUNTING FOR LOSSES:Spoiled output, Accounting treatment, Inventory Turnover Ratio

- LABOR:Direct Labor Cost, Mechanical Methods, MAKING PAYMENTS TO EMPLOYEES

- PAYROLL AND INCENTIVES:Systems of Wages, Premium Plans

- PIECE RATE BASE PREMIUM PLANS:Suitability of Piece Rate System, GROUP BONUS SYSTEMS

- LABOR TURNOVER AND LABOR EFFICIENCY RATIOS & FACTORY OVERHEAD COST

- ALLOCATION AND APPORTIONMENT OF FOH COST

- FACTORY OVERHEAD COST:Marketing, Research and development

- FACTORY OVERHEAD COST:Spending Variance, Capacity/Volume Variance

- JOB ORDER COSTING SYSTEM:Direct Materials, Direct Labor, Factory Overhead

- PROCESS COSTING SYSTEM:Data Collection, Cost of Completed Output

- PROCESS COSTING SYSTEM:Cost of Production Report, Quantity Schedule

- PROCESS COSTING SYSTEM:Normal Loss at the End of Process

- PROCESS COSTING SYSTEM:PRACTICE QUESTION

- PROCESS COSTING SYSTEM:Partially-processed units, Equivalent units

- PROCESS COSTING SYSTEM:Weighted average method, Cost of Production Report

- COSTING/VALUATION OF JOINT AND BY PRODUCTS:Accounting for joint products

- COSTING/VALUATION OF JOINT AND BY PRODUCTS:Problems of common costs

- MARGINAL AND ABSORPTION COSTING:Contribution Margin, Marginal cost per unit

- MARGINAL AND ABSORPTION COSTING:Contribution and profit

- COST – VOLUME – PROFIT ANALYSIS:Contribution Margin Approach & CVP Analysis

- COST – VOLUME – PROFIT ANALYSIS:Target Contribution Margin

- BREAK EVEN ANALYSIS – MARGIN OF SAFETY:Margin of Safety (MOS), Using Budget profit

- BREAKEVEN ANALYSIS – CHARTS AND GRAPHS:Usefulness of charts

- WHAT IS A BUDGET?:Budgetary control, Making a Forecast, Preparing budgets

- Production & Sales Budget:Rolling budget, Sales budget

- Production & Sales Budget:Illustration 1, Production budget

- FLEXIBLE BUDGET:Capacity and volume, Theoretical Capacity

- FLEXIBLE BUDGET:ANALYSIS OF COST BEHAVIOR, Fixed Expenses

- TYPES OF BUDGET:Format of Cash Budget,

- Complex Cash Budget & Flexible Budget:Comparing actual with original budget

- FLEXIBLE & ZERO BASE BUDGETING:Efficiency Ratio, Performance budgeting

- DECISION MAKING IN MANAGEMENT ACCOUNTING:Spare capacity costs, Sunk cost

- DECISION MAKING:Size of fund, Income statement

- DECISION MAKING:Avoidable Costs, Non-Relevant Variable Costs, Absorbed Overhead

- DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS

- DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS:MAKE OR BUY DECISIONS