|

Rules of Debit and Credit |

| << Dual Aspect of Transactions |

| Steps in Accounting Cycle >> |

Financial

Statement Analysis-FIN621

VU

Lesson-3

ACCOUNTING

CYCLE/PROCESS

(Continued)

*Rules

of Debit and

Credit

From

our discussion up to this

point, we have established following rules

for Debit and Credit:

Any

account that obtains a

benefit is Debit.

OR

Anything

that will provide benefit to

the business is Debit.

Both

these statements may look

different but in fact if we consider

that whenever an account

benefits as

a

result of a transaction, it will have to

return that benefit to the

business then both the

statements will

look

like different sides of the

same picture.

For

credit,

Any

account that provides a

benefit is Credit.

OR

Anything

to which the business has a

responsibility to return a benefit in

future is Credit.

As

explained in the case of Debit,

whenever an account provides

benefit to the business the

business

will

have a responsibility to return that

benefit at some time in

future and so it is Credit.

*Rules

of Debit and Credit for

Assets

Similarly

we have established that whenever a

business transfers a value /

benefit to an account and as

a

result

creates some thing that

will provide future benefit;

the `thing' is termed as Asset. By

combining

both

these rules we can devise following rules

of Debit and Credit for

Assets:

o When

an asset is created or purchased,

value / benefit is transferred to that

account, so it

is

Debited

I.

Increase

in Asset is Debit

Reversing

the above situation if the asset is sold,

which is termed as disposing off,

for

o

say

cash, the asset account

provides benefit to the cash account.

Therefore, the asset

account

is Credited

II.

Decrease in Asset is

Credit

*Rules

of Debit and Credit for

Liabilities

Anything

that transfers value to the

business, and in turn

creates a responsibility on part of the

business

to

return a benefit, is a Liability.

Therefore, liabilities are the exact

opposite of the assets.

When

a liability is created the benefit is

provided to business by that

account so it is

o

Credited

III.

Increase in Liability is

Credit

When

the business returns the benefit or

repays the liability, the liability

account

o

benefits

from the business. So it is

Debited

10

Financial

Statement Analysis-FIN621

VU

IV.

Decrease in Liability is

Debit

*Rules

of Debit and Credit for

Expenses

Just

like assets, we have to pay

for expenses. From assets,

we draw benefit for a long

time whereas the

benefit

from expenses is for a short

run. Therefore, Expenditure is

just like Asset but for a

short run.

Using

our rule for Debit and

Credit, when we pay cash

for any expense that

expense account

benefits

from

cash, therefore, it is

debited.

Now

we can lay down our

rule for Expenditure:

o

V.

Increase in Expenditure is

Debit

Reversing

the above situation, if we return any

item that we had purchased,

we will

o

receive

cash in return. Cash account

will receive benefit from

that Expenditure account.

Therefore,

Expenditure account will be

credited

VI.

Decrease in Expenditure is

Credit

*Rules

of Debit and Credit for

Income

Income

accounts are exactly

opposite to expense accounts

just as liabilities are

opposite to that of

assets.

Therefore,

using the same principle we

can draw our rules of Debit

and Credit for Income

VII.

Increase

in Income is Credit

VIII.

Decrease

in Income is Debit

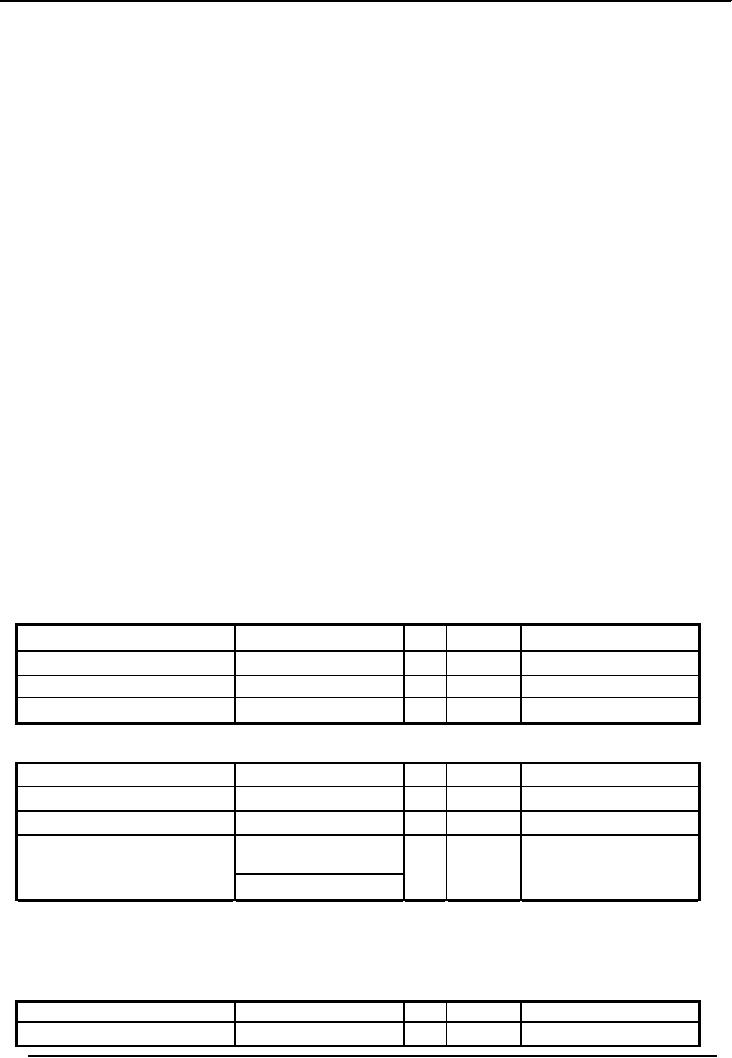

Khizr introduced a

capital of Rs.180,000 in his business

Date

Explanation

Ref

Dr.

Cr.

2006

1-Jul

Cash

Account

1

180,000

Khizr,

Capital

1

180,000

Purchased land for

cash for Rs.141,000

Date

Explanation

Ref

Dr.

Cr.

3-Jul

Land

Account

141,000

Cash

Account

141,000

Purchased

Land for

Rs.

141,000

Purchase of

building partly on cash (Rs.15,000) and partly

on credit

(Rs.21,000)

Date

Explanation

Ref

Dr.

Cr.

5-Jul

Building

Account

36,000

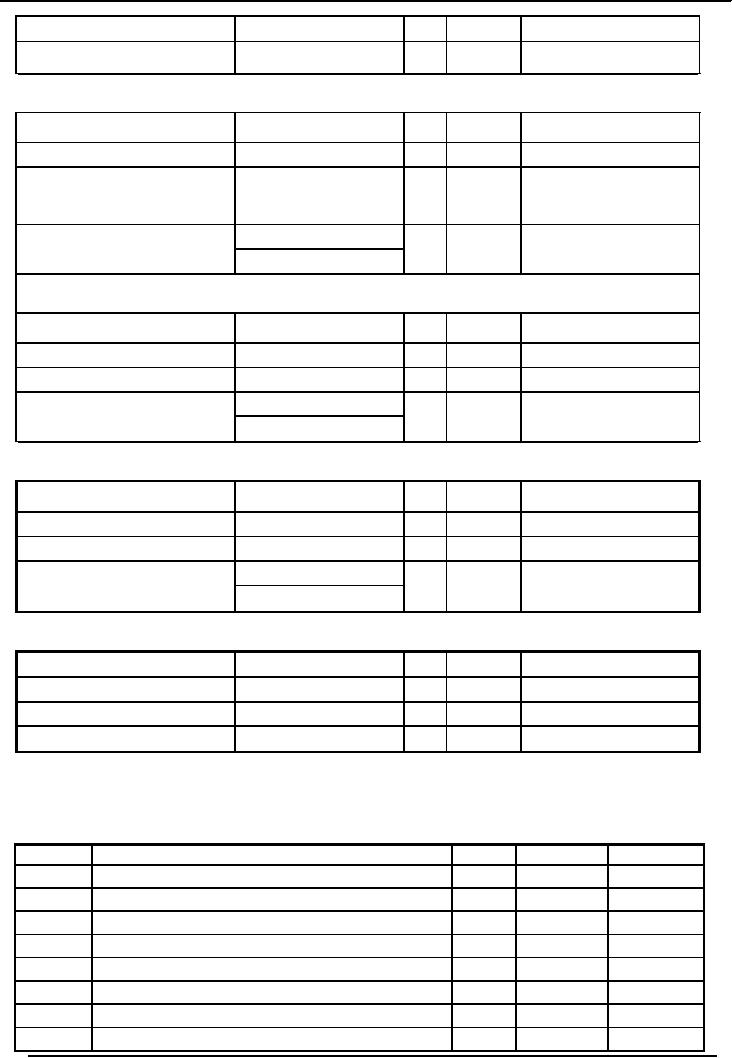

11

Financial

Statement Analysis-FIN621

VU

Cash

Account

15,000

Accounts

Payables

21,000

Sale of part of

land on credit for Rs.11,000

Date

Explanation

Ref

Dr.

Cr.

10-Jul

Accounts

receivables

11,000

11,000

Land

Account

Sold

a portion of land

for

Rs. 11,000.

Purchase of Office

Equipment for Rs.5400 on credit

Date

Explanation

Ref

Dr.

Cr.

14-Jul

Office

equipment

5,400

Accounts

Payables

5,400

Purchased

Equipment

on

credit

Partial collection

of Accounts Rs.1500

Date

Explanation

Ref

Dr.

Cr.

20-Jul

Cash

account

1,500

Accounts

receivables

1,500

Collection

of accounts

receivables

Payment of

liability (A/C Payable)

Rs.3, 000.

Date

Explanation

Ref

Dr.

Cr.

31-Jul

Accounts

payables

3,000

Cash

account

3,000

Payment of

liability

Khizr

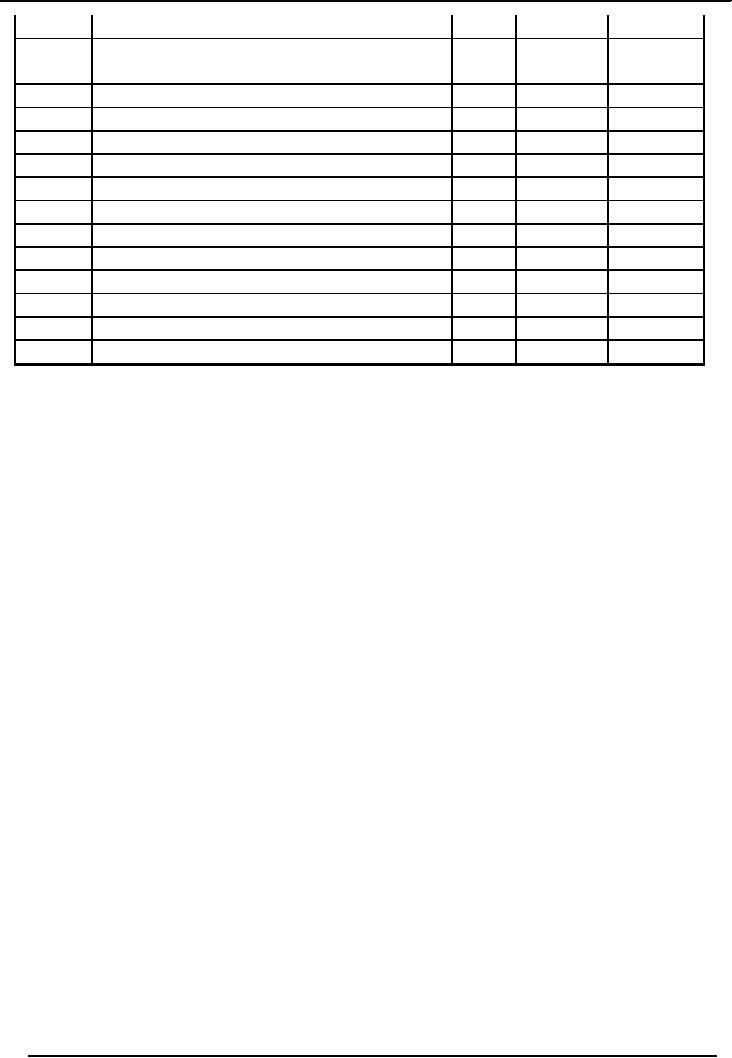

Limited

General

Journal

For the month of

July 2006

Date

Description

L/F

Dr.

Cr.

1-Jul

Cash

Account

180,000

Khizr,

Capital

180,000

Capital

Invested by owner

3-Jul

Land

Account

141,000

Cash

Account

141,000

Purchased

Land for Rs.

141,000

5-Jul

Building

Account

36,000

Cash

Account

15,000

12

Financial

Statement Analysis-FIN621

VU

Accounts

Payables

21,000

Purchased

Building partly for cash and

partly on

credit

10-Jul

Accounts

receivables

11,000

Land

Account

11,000

Sold

a portion of land for Rs.

11,000.

14-Jul

Office

equipment

5,400

Accounts

Payables

5,400

Purchased

Equipment on credit

20-Jul

Cash

account

1,500

Accounts

receivables

1,500

Collection

of accounts receivables

31-Jul

Accounts

payables

3,000

Cash

account

3,000

Payment of

liability

13

Table of Contents:

- ACCOUNTING & ACCOUNTING PRINCIPLES

- Dual Aspect of Transactions

- Rules of Debit and Credit

- Steps in Accounting Cycle

- Preparing Balance Sheet from Trial Balance

- Business transactions

- Adjusting Entry to record Expenses on Fixed Assets

- Preparing Financial Statements

- Closing entries in Accounting Cycle

- Income Statement

- Balance Sheet

- Cash Flow Statement

- Preparing Cash Flows

- Additional Information (AI)

- Cash flow from Operating Activities

- Operating Activities’ portion of cash flow statement

- Cash flow from financing Activities

- Notes to Financial Statements

- Charging Costs of Inventory to Income Statement

- First-in-First - out (FIFO), Last-in-First-Out (LIFO)

- Depreciation Accounting Policies

- Accelerated-Depreciation method

- Auditor’s Report, Opinion, Certificate

- Management Discussion & Analyses (MD&A)

- TYPES OF BUSINESS ORGANIZATIONS

- Incorporation of business

- Authorized Share Capital, Issued Share Capital

- Book Values of equity, share

- SUMMARY

- SUMMARY

- Analysis of income statement and balance sheet:

- COMMON –SIZE AND INDEX ANALYSIS

- ANALYSIS BY RATIOS

- ACTIVITY RATIOS

- Liquidity of Receivables

- LEVERAGE, DEBT RATIOS

- PROFITABILITY RATIOS

- Analysis by Preferred Stockholders

- Efficiency of operating cycle, process

- STOCKHOLDERS’ EQUITY SECTION OF THE BALANCE SHEET 1

- STOCKHOLDERS’ EQUITY SECTION OF THE BALANCE SHEET 2

- BALANCE SHEET AND INCOME STATEMENT RATIOS

- Financial Consultation Case Study

- ANALYSIS OF BALANCE SHEET & INCOME STATEMENT

- SUMMARY OF FINDGINS