|

Macroeconomics

ECO 403

VU

LESSON

31

AGGREGATE

DEMAND IN THE OPEN

ECONOMY(Continued...)

Equilibrium

in the Mundell-Fleming

model

Y

= C

(Y

- T

) +

I

(r

*) +

G

+ NX

(e

)

M

P = L

(r

*,Y

)

LM*

e

equilibrium

exchange

rate

IS*

equilibrium

Y

level

of

income

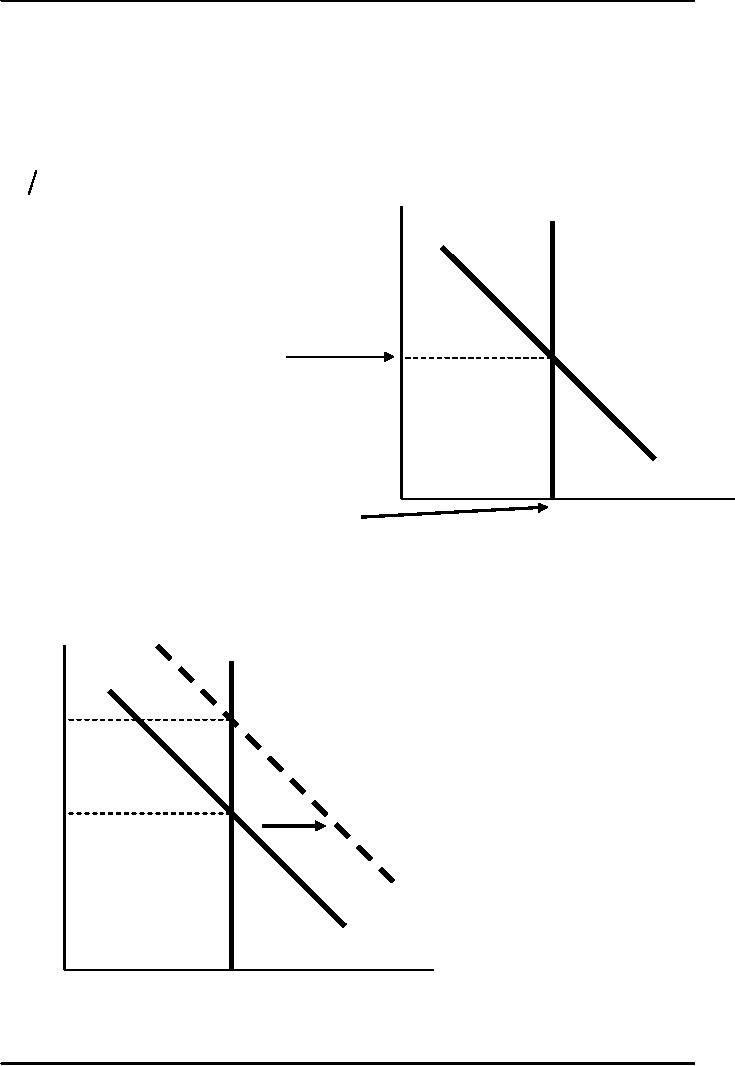

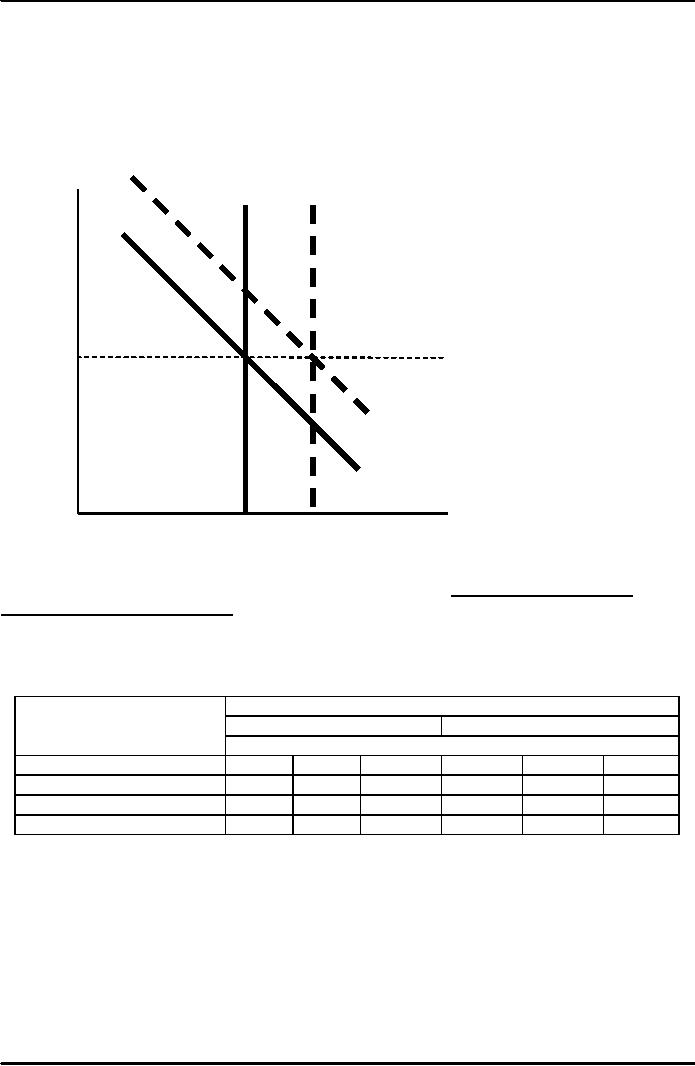

Fiscal

policy under floating

exchange rates

At

any given value of e, a

fiscal expansion increases Y,

shifting IS* to the right.

Results: Δe >

0,

ΔY

= 0

LM*1

e

e2

e1

IS*2

IS*1

Y

Y1

Results: Δe >

0, ΔY =

0

145

Macroeconomics

ECO 403

VU

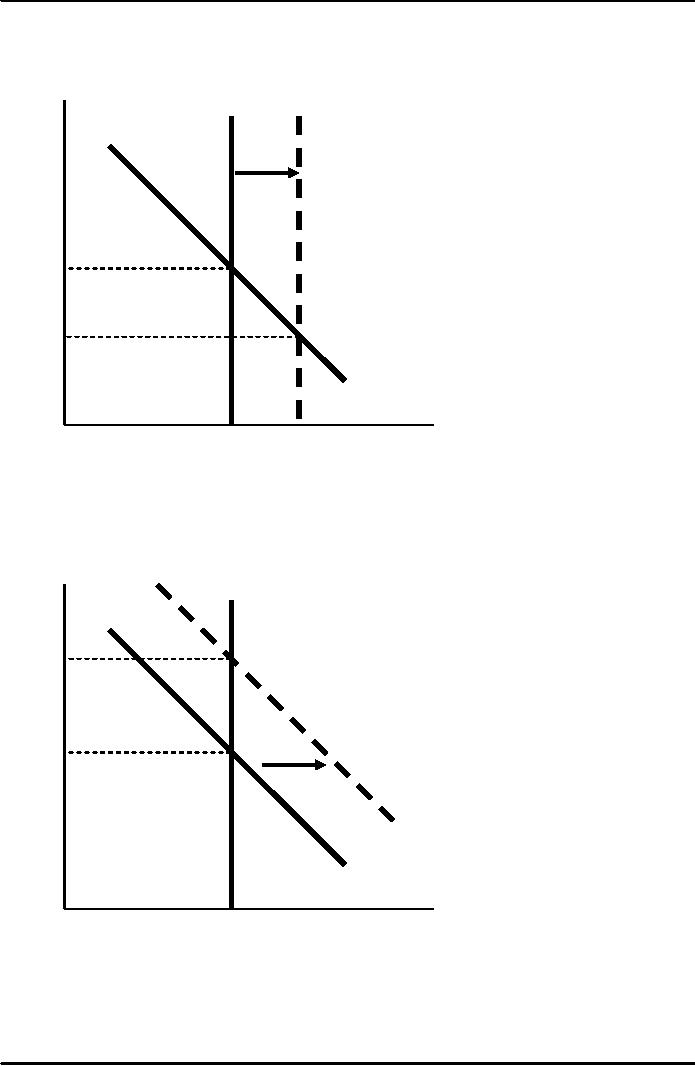

Monetary

policy under floating

exchange rates

An

increase in M shifts LM*

right because Y must rise to

restore equilibrium in the

money

market.

e

LM*1

LM*2

e1

e2

IS*1

Y

Y1

Y2

Results:

Δe <

0, ΔY >

0

Trade

policy under floating

exchange rates

At

any given value of e, a

tariff or quota reduces

imports, increases NX, and

shifts IS* to the

right.

LM*1

e

e2

e1

IS*2

IS*1

Y

Y1

Lessons

about trade

policy

·

Import

restrictions cannot reduce a

trade deficit.

·

Even

though NX is unchanged, there is

less trade:

146

Macroeconomics

ECO 403

VU

The trade

restriction reduces

imports

Exchange

rate appreciation reduces

exports

Less

trade means fewer `gains

from trade.'

·

Import

restrictions on specific products

save jobs in the domestic

industries that

produce

those

products, but destroy jobs

in export-producing sectors.

Hence,

import restrictions fail to

increase total

employment.

Worse

yet, import restrictions

create "sectoral shifts,"

which cause

frictional

unemployment.

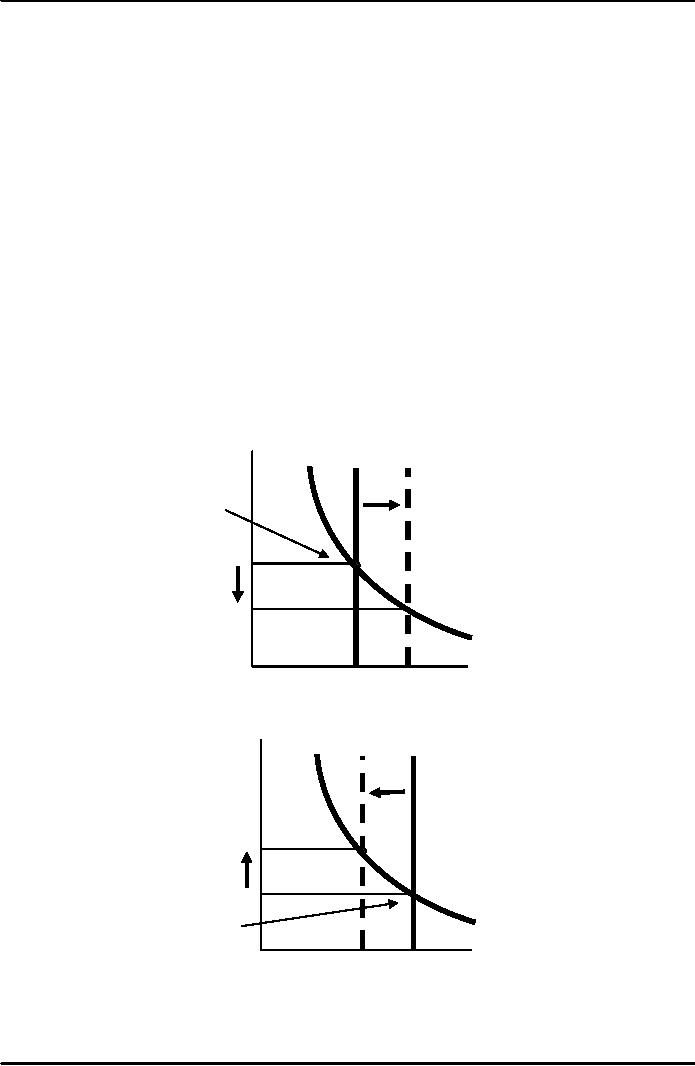

Fixed

exchange rates

·

Under

a system of fixed exchange

rates, the country's central

bank stands ready to buy

or

sell

the domestic currency for

foreign currency at a predetermined

rate.

·

In

the context of the

Mundell-Fleming model, the

central bank shifts the LM*

curve as

required

to keep e at its pre-announced

rate.

·

This

system fixes the nominal

exchange rate.

In

the long run, when

prices are flexible, the

real exchange rate can

move even if the

nominal

rate is fixed.

a.

The Equilibrium exchange

rate is Greater than the

fixed exchange rate

LM1 LM2

e

Equilibrium

exchange

rate

>

>

>

Fixed

exchange rate

IS*

Income,

Output, Y

b.

The Equilibrium exchange

rate is less than the

fixed exchange rate

LM2 LM1

e

Fixed

exchange rate

>

>>

IS*

Equilibrium

exchange rate

Income,

Output, Y

147

Macroeconomics

ECO 403

VU

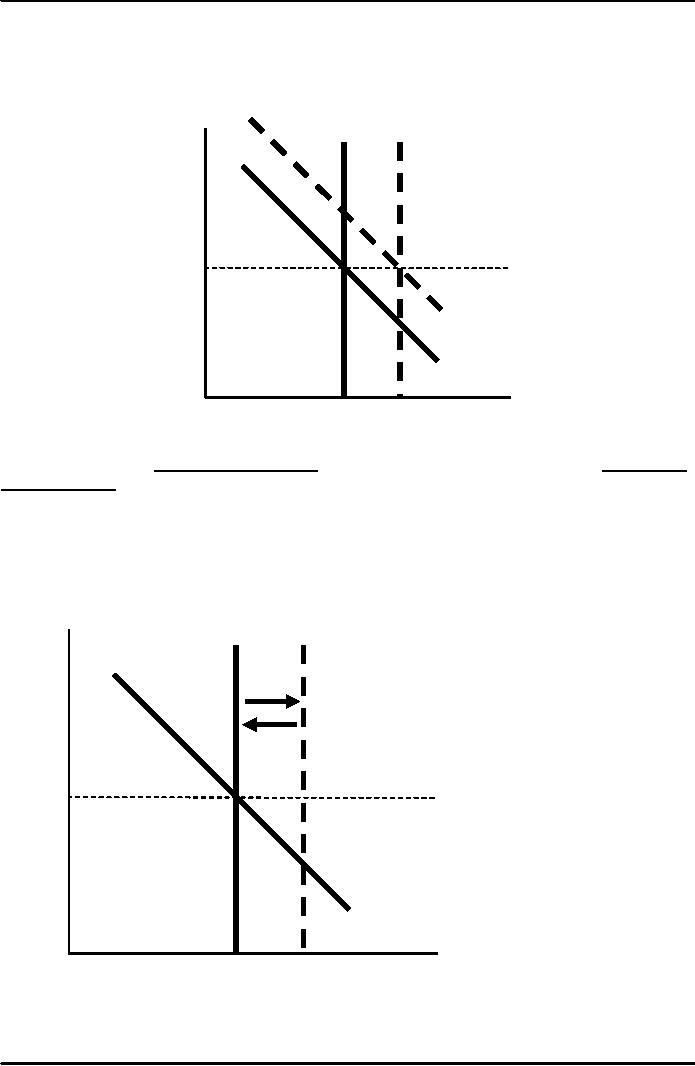

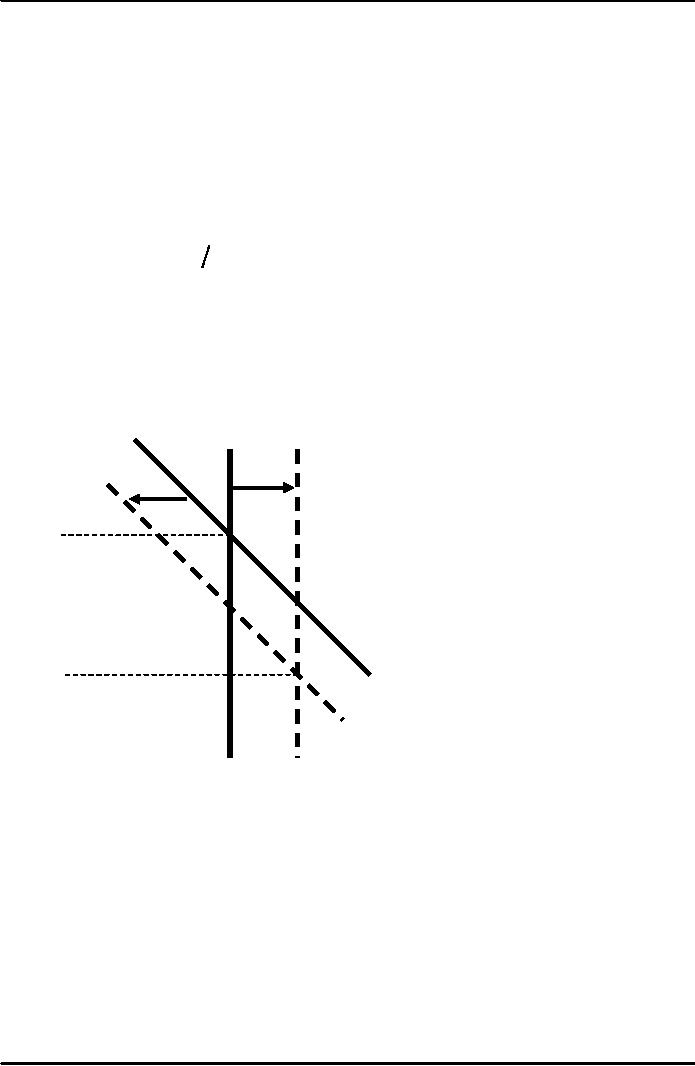

Fiscal

policy under fixed exchange

rates

Under

fixed exchange rates, a

fiscal expansion would raise

e. To keep e from

rising,

the

central bank must sell

domestic currency, which

increases M and shifts LM*

right.

LM*1

LM*2

e

e1

IS*2

IS*1

Y

Y1

Y2

Results:

Δe =

0, ΔY >

0

Under

floating rates, fiscal

policy ineffective at changing

output. Under fixed rates,

fiscal policy

is

very effective at changing

output. LM

shifts out!

Monetary

policy under fixed exchange

rates

An

increase in M would shift LM*

right and reduce e. To

prevent the fall in e, the

central bank

must

buy domestic currency, which

reduces M and shifts LM*

back left.

LM*1

LM*2

e

e1

IS*1

Y

Y1

Y2

Results:

Δe =

0, ΔY =

0

148

Macroeconomics

ECO 403

VU

Under

floating rates, monetary

policy is very effective at

changing output. Under fixed

rates,

monetary

policy cannot be used to

affect output.

Trade

policy under fixed exchange

rates

A

restriction on imports puts

upward pressure on e.

To keep e

from

rising, the central

bank

must

sell domestic currency,

which increases M

and

shifts LM*

right.

LM*1

LM*2

e

e1

IS*2

IS*1

Y

Y1

Y2

Results:

Δe =

0, ΔY >

0

Under

floating rates, import

restrictions do not affect Y or NX.

Under fixed rates,

import

restrictions

increase Y and NX. But,

these gains come at the

expense of other countries,

as

the

policy merely shifts demand

from foreign to domestic

goods

M-F:

summary of policy

effects

Type

of Exchange Rate

Regime

Floating

Fixed

Impact

on

Policy

Y

e

NX

Y

e

NX

Fiscal

Expansion

0

0

0

Monetary

Expansion

0

0

0

Import

Restriction

0

0

0

Interest-rate

differentials

Two

reasons why r may differ

from r*

·

Country

risk:

The

risk that the country's

borrowers will default on

their loan repayments

because of

political

or economic turmoil. Lenders

require a higher interest

rate to compensate

them

for this risk.

149

Macroeconomics

ECO 403

VU

·

Expected

exchange rate

changes:

If

a country's exchange rate is

expected to fall, then its

borrowers must pay a

higher

interest

rate to compensate lenders

for the expected currency

depreciation.

Differentials

in the M-F model

r

= r

*+ θ

Where

θ

is a

risk premium.

Substitute

the expression for r into

the IS* and LM*

equations:

Y

= C

(Y

- T

) +

I

(r

* + θ )

+

G

+ NX

(e

)

M

P = L

(r

* + θ ,Y

)

The

effects of an increase in θ

IS*

shifts left, because ↑

θ ⇒ ↑r

⇒

↓I

LM*

shifts

right, because ↑

θ ⇒

↑r

⇒

↓(M/P) d,

So

Y must rise to restore money

market equilibrium.

LM*1

LM*2

e1

e2

IS*1

IS*2

Y1

Y2

The

effects of an increase in θ

·

The

fall in e is intuitive:

An

increase in country risk or an

expected depreciation makes

holding the country's

currency

less attractive.

Note:

an expected depreciation is a

self-fulfilling prophecy.

·

The

increase in Y occurs because

the boost in NX (from the

depreciation) is even

greater

than

the fall in I (from the

rise in r).

150

Table of Contents:

- INTRODUCTION:COURSE DESCRIPTION, TEN PRINCIPLES OF ECONOMICS

- PRINCIPLE OF MACROECONOMICS:People Face Tradeoffs

- IMPORTANCE OF MACROECONOMICS:Interest rates and rental payments

- THE DATA OF MACROECONOMICS:Rules for computing GDP

- THE DATA OF MACROECONOMICS (Continued ):Components of Expenditures

- THE DATA OF MACROECONOMICS (Continued ):How to construct the CPI

- NATIONAL INCOME: WHERE IT COMES FROM AND WHERE IT GOES

- NATIONAL INCOME: WHERE IT COMES FROM AND WHERE IT GOES (Continued )

- NATIONAL INCOME: WHERE IT COMES FROM AND WHERE IT GOES (Continued )

- NATIONAL INCOME: WHERE IT COMES FROM AND WHERE IT GOES (Continued )

- MONEY AND INFLATION:The Quantity Equation, Inflation and interest rates

- MONEY AND INFLATION (Continued ):Money demand and the nominal interest rate

- MONEY AND INFLATION (Continued ):Costs of expected inflation:

- MONEY AND INFLATION (Continued ):The Classical Dichotomy

- OPEN ECONOMY:Three experiments, The nominal exchange rate

- OPEN ECONOMY (Continued ):The Determinants of the Nominal Exchange Rate

- OPEN ECONOMY (Continued ):A first model of the natural rate

- ISSUES IN UNEMPLOYMENT:Public Policy and Job Search

- ECONOMIC GROWTH:THE SOLOW MODEL, Saving and investment

- ECONOMIC GROWTH (Continued ):The Steady State

- ECONOMIC GROWTH (Continued ):The Golden Rule Capital Stock

- ECONOMIC GROWTH (Continued ):The Golden Rule, Policies to promote growth

- ECONOMIC GROWTH (Continued ):Possible problems with industrial policy

- AGGREGATE DEMAND AND AGGREGATE SUPPLY:When prices are sticky

- AGGREGATE DEMAND AND AGGREGATE SUPPLY (Continued ):

- AGGREGATE DEMAND AND AGGREGATE SUPPLY (Continued ):

- AGGREGATE DEMAND AND AGGREGATE SUPPLY (Continued )

- AGGREGATE DEMAND AND AGGREGATE SUPPLY (Continued )

- AGGREGATE DEMAND AND AGGREGATE SUPPLY (Continued )

- AGGREGATE DEMAND IN THE OPEN ECONOMY:Lessons about fiscal policy

- AGGREGATE DEMAND IN THE OPEN ECONOMY(Continued ):Fixed exchange rates

- AGGREGATE DEMAND IN THE OPEN ECONOMY (Continued ):Why income might not rise

- AGGREGATE SUPPLY:The sticky-price model

- AGGREGATE SUPPLY (Continued ):Deriving the Phillips Curve from SRAS

- GOVERNMENT DEBT:Permanent Debt, Floating Debt, Unfunded Debts

- GOVERNMENT DEBT (Continued ):Starting with too little capital,

- CONSUMPTION:Secular Stagnation and Simon Kuznets

- CONSUMPTION (Continued ):Consumer Preferences, Constraints on Borrowings

- CONSUMPTION (Continued ):The Life-cycle Consumption Function

- INVESTMENT:The Rental Price of Capital, The Cost of Capital

- INVESTMENT (Continued ):The Determinants of Investment

- INVESTMENT (Continued ):Financing Constraints, Residential Investment

- INVESTMENT (Continued ):Inventories and the Real Interest Rate

- MONEY:Money Supply, Fractional Reserve Banking,

- MONEY (Continued ):Three Instruments of Money Supply, Money Demand